Author

By all accounts, much of the current turmoil in financial markets originated in the housing market. Following years of booming home sales, facilitated by looser credit and alternative financing for riskier borrowers, the housing market started to cool. Prices declined; then a lot of mortgage debt began to go bad.

The subsequent fallout in the broader economy has been the subject of considerable attention and debate. But it's also worth circling back to see if credit conditions have changed in the business sector where this all got started.

The sheer drop of homes bought and sold might imply a horrific credit crunch in home mortgages. That's not the case: Mortgage credit is still available, and at mortgage interest rates that remain cheap by historical comparison (see chart).

But the housing tumult has convinced the mortgage industry to adopt new, and typically more stringent, credit standards. According to the Federal Reserve Board's October survey of senior loan officers, 85 percent of banks reported tightening standards for conventional mortgages and 100 percent are tightening subprime standards.

Traditional mortgages are still available to borrowers with good credit if they're willing to jump through more hoops. But investors that undergird the home-loan market have stopped buying up exotic and riskier mortgages, and those mortgage products are either going up in price or going away altogether. Other sectors like second mortgages and home equity loans have also been affected, but sources say that even those loans are still available from some lenders, for the time being. And as certain portions of the home-loan market fall away, other smaller lending sources are finding room to grow.

Financial crash course

At first glance, a mortgage seems like any other loan; banks lend money from bank deposits to borrowers looking to buy a house. But that only describes a small—and until recently, shrinking—segment of the market.

There are thousands of mortgage lenders nationwide. But most of the funds being borrowed ultimately come from a handful of very large investors—like Citibank, GMAC and Wells Fargo—that ultimately determine the mortgage terms and credit standards that borrowers must meet.

Banks also used to keep home loans on their books, but that's less common today. Instead, they typically sell mortgages (usually pooled as mortgage-backed securities) in the secondary markets. This replenishes lendable funds and maintains liquidity for the next person looking for a mortgage.

The secondary market is dominated by Fannie Mae and Freddie Mac, which are so-called government-sponsored enterprises (GSEs) and whose standards for buying loans influence overall mortgage lending conditions. But the housing slump also sent Fannie and Freddie into government conservatorship after both nearly collapsed.

Tight fit

The broader point here: Primary and secondary financial markets that fund most mortgages have been in turmoil, and as these credit markets change, so do retail mortgage products.

Take conventional loans, for example. They are still widely available, but the standards to qualify for one have risen. For example, both Fannie Mae and Freddie Mac have tightened requirements and now want larger down payments. And the degree of price discrimination has become finer; two high-quality borrowers with slightly different credit scores might now pay quite different rates on identical mortgages, where before they might have been in the same pricing category. These changes are called loan-level price adjustments.

The shift in mortgage products is much more obvious among nonconventional mortgages—particularly subprime, Alt-A (which has risk between prime and subprime) and jumbo mortgages (which finance more expensive homes). In 2006, subprime and Alt-A mortgages made up 33 percent of new mortgage loans, according to an October 2008 report by Freddie Mac. But skyrocketing loan defaults have been a death-knell for these mortgage niches. Through the first half of 2008, the share of these nonconventional loans plunged to just 3 percent, and most anecdotal evidence suggests the market continues to throw dirt on most nonconventional mortgage products.

"The Alt-A, subprime, stated income—all those markets completely went away," said Paul Schuster, a mortgage lender in Edina, Minn.

The reason is simple: Realizing they had badly mispriced the underlying risk of these borrowers, financial markets became unwilling to finance these mortgages any longer. Annual issuance of subprime and Alt-A mortgage-backed securities—which provide liquidity in these markets—went from close to $800 billion in 2006 to effectively zero through the first six months of 2008, according to the Freddie Mac report.

The disappearance of these alternative mortgages hasn't bothered many real estate agents and lenders in Montana and the Dakotas, where such products were not very prevalent. Housing markets in cities like Fargo, N.D., and Billings, Mont., have slowed, but not much in comparison with major markets nationwide. Many attribute that stability both to the absence of earlier housing bubbles and to conservatism on the part of lenders and borrowers.

"We're pretty old-school here, and there wasn't a lot of demand for anything outside the 30-year fixed mortgage," said Steve Tucker, a mortgage broker in Billings.

Jumbo mortgages are also in a tough spot because GSEs cannot buy jumbo loans, or those valued at over $417,000. Their market share has fallen as well, from 16 percent in 2006 to 6 percent in 2008, as financing in the secondary market dried up. However, Congress passed emergency legislation last February that temporarily raised the loan limit to $730,000 in high-cost regions of the country, before lowering it to $625,500 for 2009 mortgages.

When the new limits went into effect, "rates for jumbo borrowers in high cost areas plunged" by more than one percentage point, according to a press release from FreddieMac. However, don't bother looking for those higher jumbo limits around here; all high-cost designations lie outside the Ninth District. And because those loans are typically for prime borrowers, the jumbo mortgage market reflects more signs of a classic credit contraction, because "investors (have) dried up, as opposed to the demand," said Schuster.

Credit conditions are also tightening for second mortgages and home equity loans. These loans, which allow homeowners to borrow against their home equity, were widely credited for fueling strong consumer spending for a decade leading up to the housing collapse.

But now it's not as easy to get those loans. Though many banks still offer such products, anecdotal evidence and recent surveys by the Minneapolis Fed (see cover story) suggest they've been scaled back. In the Federal Reserve System's two most recent quarterly surveys (July and October 2008) of senior loan officers, three-quarters of the nation's banks reported tightened lending standards for revolving home equity lines of credit. Slightly more than one-quarter of domestic banks reported weaker demand for this type of credit in October, more than double the fraction in the July survey.

The victors

Tighter lending conditions have provided an unexpected boost to some players in the mortgage market. Home sales might be down, but they haven't vanished altogether.

Credit unions and community banks have been beneficiaries of the shift. Since these firms primarily keep their loans in-house, they aren't as affected by conditions in the secondary market. "The credit union industry as a whole has not felt anywhere near the crunch that the commercial banking industry has," said Paul Scherman at WESTconsin Credit Union in Menomonie, Wis. WESTconsin makes more conventional loans that can still be sold to Fannie and Freddie, but also offers adjustable-rate mortgages and equity loans that cannot.

The data show that rather than running away from the housing market, credit unions have been running toward it. From September 2007 to September 2008, the amount of real estate loans outstanding with the nation's 7,900 federally insured credit unions grew 15 percent, according to data from the National Credit Union Administration, the federal agency that charters and supervises federal credit unions. At $300 billion in mortgages (third-quarter annualized rate), credit unions expanded in all areas over this period. Fixed-rate mortgages saw particularly strong growth (20 percent), but balloon/hybrid and adjustable-rate mortgages were also higher over this period, as were home equity lines of credit.

Home Federal, a community bank in Sioux Falls, S.D., has started making in-house jumbo loans because the secondary market prices them prohibitively high. "We decided to go out and set aside a few bucks so that we could handle some of these jumbo products and offer the people a competitive rate," said Gary Weckwerth, vice president for mortgage banking at Home Federal.

Loans backed by the Federal Housing Administration have also spiked in response to market developments. The FHA is an insurance fund run by the U.S. Department of Housing and Urban Development. HUD works with a network of mortgage lenders that it certifies. Those lenders can make 30-year fixed-rate loans to qualified borrowers that are then insured by the FHA. Insurance premiums are part of the mortgage payment.

FHA-insured loans are low risk and have traditionally been an inroad for first-time buyers and others for whom homeownership might not otherwise have been an option. But FHA lending started to decline with the rise of subprime and Alt-A loans, which provided even greater access to financing at a lower cost for the same type of borrowers.

"We weren't getting borrowers into FHA loans, and borrowers that had FHA loans were refinancing in a mass exodus," said Anita Olson, an official at HUD's Minneapolis office.

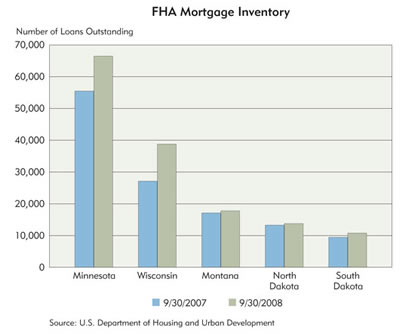

The number of FHA loans in Minnesota declined from 221,000 in 1995 to 55,000 in 2007. But now that those alternatives aren't as readily available, FHA loans have increased in district states (see chart). Nationally, FHA loans have increased from 3 percent of mortgages to 17 percent.

For mortgage lenders that are FHA-certified, this business has become bread-and-butter; those who aren't certified are forced out of this market niche. "We kind of took [subprime] out of the marketplace," said Ron Jordan at State Bank and Trust in Fargo, which does mostly FHA and conventional 30-year fixed-rate mortgages. "We're up about 20 percent over last year."

Where credit is due

Like credit markets nationwide, mortgage credit might best be described as a qualified seek-and-ye-shall-find market—if you shop around, and if you have good credit. If you don't, your options appear more limited than they once were because markets have been forced to recalibrate how they price borrower risk.

Despite the housing slump, the Mortgage Bankers Association acknowledged on its Web site that "the marketplace is working. The volume of many nontraditional products is down because investors, rating agencies and lenders have tightened underwriting standards."

As such, borrowers, lenders and the many interrelated parties involved in the mortgage industry are adjusting to tighter credit standards, and no one knows for sure whether they are temporary, wait-and-see temporary or permanent.

The outlook for the housing market brightened in late November when the Federal Reserve announced a program to increase liquidity in the mortgage finance industry by purchasing $100 billion in GSE debt and up to $500 billion in mortgage-backed securities issued by Fannie Mae, Freddie Mac and Ginnie Mae. The impact was immediately favorable, as interest rates on 30-year fixed-rate mortgages dropped more than a full percentage point.

Whether lower mortgage rates hold and what effect they might have on the housing market is hard to predict, and many in the industry are wary of trying to anymore.

Jordan, from Fargo, expressed optimism for the Fargo region, but he was less bold in assessing how the market might perform going forward. "I'd say I can't imagine it getting worse, but a year ago I'd have said I couldn't imagine a lot of what's going on now."

Joe Mahon is a Minneapolis Fed regional outreach director. Joe’s primary responsibilities involve tracking several sectors of the Ninth District economy, including agriculture, manufacturing, energy, and mining.

{kind=link}

{kind=link}