Author

Article Highlights

- After period of rapid growth, mobile homes surpassed one-third of new single-family homes in early 1970s

- Ostracism and state regulation paradoxically facilitated mobile home boom, unleashing productivity gains and true affordability

- Schmitz: “Stick-built” pressure and federal regulation subsequently relegated manufactured housing to small market share

Just over the city line from Minneapolis, Tim Schroeder has some affordable housing to show off—market-rate, no subsidy required. He leads the way into a new, 1,200-square-foot manufactured home. The closing is scheduled for the next day.

“You could imagine kids doing their homework at the counter,” said Schroeder, gesturing to the large kitchen island across from a farmhouse-style sink. “The parents’ suite is in the back.” Schroeder is president of Performance Realty Inc., the California-based owner of Urban Grove in St. Anthony, Minnesota. The realty firm acquired the 100-lot community in 2023 after a controversial prior sale nearly led to redevelopment.

Jeff Horwich/Minneapolis Fed

Schroeder says this three-bedroom, two-bath home will close for around $130,000—less than half the median home price in Minneapolis. In contrast to the tight market for conventional homes in the Twin Cities, Urban Grove still has plenty of capacity. “Here you’ve got a brand-new home with 2-by-6 construction, high-efficiency furnace, no neighbor up top,” Schroeder said, gesturing toward a condo building across the road. After a 5 percent down payment, Schroeder says the combined lot rent and loan payment will be $1,800 to $2,000 a month, a bit below the cost of an average three-bedroom rental in the city.

New homes for Urban Grove roll out of the cavernous hangar of MidCountry Homes in Dorchester, Wisconsin. Videos show workers maneuvering giant sections along an assembly line, each workstation staffed by a specialist. Each order is customized for the homeowner, but within a standardized process that allows a house ordered for Urban Grove to arrive on-site in as little as eight weeks. Others head to stand-alone plots around the Midwest, where they look much like any single-family home.

To Minneapolis Fed Senior Research Economist James Schmitz Jr., this is where every realistic conversation about affordable housing should lead. “We will never, ever have affordable housing unless we have factory production,” Schmitz said, “and at a big level.” Manufactured homes might not be for everybody. But they could be the answer for millions more households than they now serve, Schmitz contends—if not for lingering stigma, hostile zoning, and a regulatory legacy that raises costs for manufactured homes and preserves the power of traditional “stick-built” home construction.

Banishment, and a boom

Policy experts generally agree that improving housing affordability cannot happen without a surge in supply. One obvious option—making houses in factories—lingers near historic lows, with a single-digit share of new single-family homes. In a recent Minneapolis Fed staff report, Schmitz, Elena Falcettoni of the Federal Reserve Board of Governors, and Mark Wright of the St. Louis Fed look to the relative heyday of mobile homes—from the 1950s to the early 1970s—for lessons that might serve us today.1 “Not only was this episode the first successful U.S. experiment in mass producing homes,” they write, “it remains the only one.”

After World War II, U.S. manufactured home sales accelerated, peaking at more than one-third of single-family production for a period around 1970 (Figure 1).

Although the market had partial rebounds amid the 1980s recession and an ill-fated surge of no-document lending in the 1990s (which led later to a rash of repossessions), manufactured housing fell below 10 percent of single-family production by the 2000s.

The national average masks a wide variation from state to state. The boom culminating in the early 1970s was especially strong in the South and parts of the Mountain West, where mobile homes comprised more than half of all new single-family housing. In parts of the Northeast, mobile homes never broke above a single-digit share (Figure 2).

Schmitz and his co-authors describe how, from the 1940s into the 1970s, the mobile home industry grew in spite of—or, paradoxically, because of—the efforts of many communities to restrict or prohibit them. They recount how localities used existing Depression-era bans on “trailers” or crafted new zoning rules to push mobile homes to industrial areas or unincorporated land. (It is no coincidence that Urban Grove lies just feet outside of Minneapolis or that two of Minnesota’s smallest full-fledged cities—Hilltop and Landfall—began as mobile home communities that later incorporated.)

One result of this exclusion: Where mobile homes were allowed to take root, they did not need to comply with myriad local residential building codes and minimum square-footage requirements. “These localities had banned Mobile Homes from residential areas for not being homes,” the economists write, “which left them in no position to now claim they were homes” and try to regulate them.

In communities that did not have outright bans, mobile homes were often still restricted to designated parks. This led to the typical financing model of many mobile homes: With the land underneath them owned by someone else, lenders generally refused to finance mobile homes with mortgages. Instead, most owners took out personal property (“chattel”) loans, with shorter terms and higher rates—the financing approach that still prevails today.

Building the boom: “We want the state to regulate us”

Amid the wild west of manufacturing standards, an industry trade group saw an opportunity. Through the Mobile Home Manufacturers Association (MHMA), U.S. builders agreed on voluntary standards for plumbing, electrical, and heating systems—and then worked through the 1960s to make them mandatory at the state level. “Coming in and taking the approach of, ‘We want the state to regulate us’—that was the start,” Schmitz said.

The MHMA worked methodically to assemble endorsements from groups like the National Fire Protection Association. The MHMA then successfully shopped its self-adopted code to state legislatures. By 1973, 44 states had enacted codes.

The standards raised home quality, Schmitz said, reassuring potential consumers. Crucially, the economists also highlight how new regulations—rather than stifling growth and innovation—unleashed the economic forces that helped the industry achieve large-scale production and falling costs. Manufacturers producing to a consistent code could scale up production and open factories in different parts of the country using standardized technology. Common standards also increased the incentive for outside vendors to innovate, pitching the mobile home industry on new products and processes in hopes of landing large contracts (“directed technological change,” in the language of economics).

Growing scale supported ancillary research, such as lender surveys to understand financing barriers and new guidance on developing and managing successful parks. Given the prevalence of mobile homes in rural areas, state agricultural extension services emerged as a research resource. This “information infrastructure” fostered further expansion, in a virtuous cycle.

Shipments of mobile homes rose from 60,000 in 1947 to nearly 600,000 by 1973. As scale increased, the prices of mobile homes fell dramatically, from roughly $18 per square foot in 1960 to $6 in 1973 (both numbers in 1960 dollars). Without similar productivity improvements, the square-foot price of comparable stick-built homes rose slightly over this period, becoming almost twice as expensive as mobile homes by 1973 (Figure 3).

“It was a period when we really were making affordable homes,” Schmitz said. “A lot of people could buy them.” A typical 700 square-foot mobile home in 1973 might seem small by today’s standards. But at a cost of about $6,500—less than $46,000 in current dollars—it was a feasible option for low-income households.

Schmitz contrasts this with the contemporary, income-based definition of affordable housing, which is often possible only with low-income housing tax credits and other public subsidies. “Today the term ‘affordable housing’ means the price of a home where expenses would be about one-third of family income,” he said. “It has nothing to do with whether a home can actually be produced at that price.”

Schmitz points to recent examples of “affordable” rental apartments in Chicago, constructed for $800,000 or more per unit—with a lot of public help. “In the early 1970s, mobile homes were being manufactured that builders would build and that families could afford, without any subsidies,” Schmitz said.

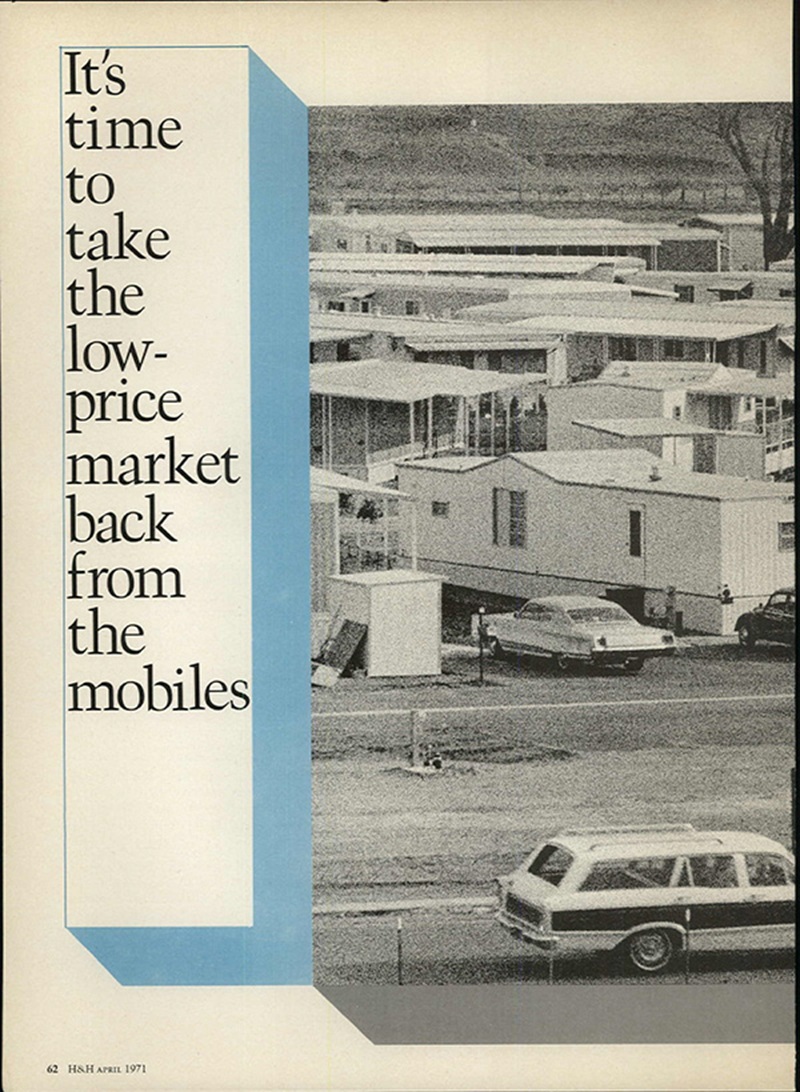

And that market was strong. In the late 1960s, HUD rolled out new federal subsidies to support low-income buyers of stick-built homes. Even so, the economists write, nonsubsidized mobile homes “continued their capture of the lowest end of the housing market.” The headline from a 1971 article in House & Home magazine captures the alarm in the stick-built sector at the time: “It’s time to take the low-price market back from the mobiles.”

Federal code, the “permanent chassis,” and the end of the boom

“That Mobile Homes succeeded despite very significant barriers to them is a testament to the great power of mass production,” write Schmitz and his co-authors. But the mobile home industry was rolling toward a cliff.

Washington State Department of Archaeology and Historic Preservation

In 1974, Congress passed the National Manufactured Housing Construction and Safety Standards Act. By 1976, the new “HUD code” drafted by the U.S. Department of Housing and Urban Development superseded the state codes. In the HUD telling, the federal code helped “ease the administrative burden on manufacturers while establishing consumer protections, allowing manufacturers to build to a single construction standard.” The code reduced the enforcement burden on states with limited resources and “decreased manufacturing costs while ensuring a minimum level of safety.”

Schmitz believes the subsequent path of the industry—rising prices and falling market share—points to a different conclusion: “The whole HUD code was set up for the industry to fail.” Schmitz argues the lobbying power of traditional stick-builders shaped a future in which factory-made housing remained a niche market.2

While the industry-drafted state codes led to falling costs and rising productivity, Schmitz believes the federal code simultaneously increased costs and decreased the appeal. This included fire and energy codes that exceeded what some experts believed were necessary.

Another prime exhibit for Schmitz is front-and-center in the HUD code’s new definition of a manufactured home: “Built on a permanent chassis and designed to be used as a dwelling with or without a permanent foundation.” Previously, the economists write in their staff report, it was common for buyers to remove the frame, axles, and wheels used to transport the home to its site. The home was then placed on a permanent foundation, often with a full basement. But after 1974, they write, “doing this would incur additional, significant costs, as the home had a chassis attached to it. Foundations and basements would have to be dug deeper to accommodate the chassis. Even then the chassis would be lying exposed,” unless a false ceiling was installed at additional expense.

In a recent op-ed in the Washington Post, Schmitz and UCLA economist Lee Ohanian argued that the permanent chassis requirement leaves manufactured homes more vulnerable to severe weather by inhibiting the use of foundations. “Homes on chassis are also far less aesthetically pleasing,” they write, “and they conjure up long-standing prejudice against ‘mobile homes’ in ‘trailer parks.’”

A big future for factory-built homes?

There is recognition at HUD and beyond that addressing the critical shortage of market-rate, nonsubsidized affordable homes includes more manufactured housing. “Factory-built housing offers many benefits, including lower production costs, and holds tremendous promise for increasing the availability of affordable rental and owner-occupied housing,” states a 2020 article in HUD’s Evidence Matters magazine. “Modern factory-built housing can be indistinguishable in appearance and quality from similar site-built housing and incorporates the latest innovations in energy efficiency and disaster resilience.”

Yet the 100,000 new manufactured homes that shipped in 2024 are a virtual speck beside the millions more homes that some estimate the country needs to meet current demand. And it’s just a fraction of the mobile home industry at its peak.

Jeff Horwich/Minneapolis Fed

Even as he sees a “strong upside” for the industry, Urban Grove’s Tim Schroeder can tick through the challenges. Without federally backed mortgage insurance for chattel loans, “the cost of money is higher,” he said. As of late 2024, Schroeder said a buyer with good credit was still facing an interest rate of at least 9 percent today. Despite the clear need in the region for homes well below the median price, “we still have a hurdle in terms of getting people in the door and understanding what they can [afford].” And there is the persistent stigma, something Urban Grove works to counter with landscaped wastewater management ponds, community raised garden beds, and other investments in curb appeal.

In some places, long-held approaches to zoning have been shifting. Minneapolis’ recent single-family zoning reform, considered among the most progressive in the country, includes the goal to “support community driven innovative housing solutions, such as prefabricated and manufactured housing, 3-D printed housing, and tiny houses.” Nonetheless, the city itself contains no designed parks, and it is too early to know how the most affordable factory-built homes will mesh with the city’s zoning code.

Nationally, the prospects for manufactured homes in urban and suburban areas are still shaped by 100-year-old notions of Dust Bowl families hauling trailers, and what is and is not a house. “I think it’s still very difficult to develop a new mobile home community in terms of approval in a lot of cities around the country,” Schroeder said.

To Minneapolis Fed economist James Schmitz, allowing owners to remove their chassis would be one practical and symbolic step toward shedding the neighborhood, civic, regulatory, and economic forces stacked against factory-built homes—and lower-income housing in general. It would be a step toward a future where manufactured houses (and prefabricated multifamily buildings) are rolling off the assembly line not by the thousands, but by the millions.

“Our analysis strongly supports those who have argued since the 1930s (at least) that the only chance of building homes that are ‘affordable’ is in a factory,” write Schmitz and his co-authors.3 “Our analysis shows that there is not only a chance, but that it’s possible. It’s been done.”

Endnotes

1 “Manufactured housing” replaced the term “mobile home” in official government business in 1980. As in the research summarized in this article, “mobile home” is used here in a historical context and to distinguish these homes from other forms of prefabricated housing (such as modular and panelized homes) that were not fully assembled before delivery and did not achieve the same scale or production efficiencies.

2 In separate work, Schmitz has written extensively on his finding that although many firms operate in the traditional homebuilding industry, the industry functions as a monopoly that inhibits innovation and competition—especially from factory construction. He sees troubling monopolistic behavior in parts of the modern manufactured housing industry as well, such as vertical integration in which the same corporate entity owns the manufacturer, lender, and park.

3 Schmitz highlights the views of a “stick-builder” who was deeply familiar with the challenge of mass-producing homes for middle- and lower-income markets: Levitt & Sons, famous for constructing entire suburban communities in the northeast U.S. after World War II. Levitt & Sons Vice President Charles Biederman, in a statement to the U.S. Senate in 1969: “Factory-built housing must succeed, or we will never be able to produce the homes and apartments needed to house our expanding population and our underprivileged citizens in a comfortable, dignified, decent way.”

Jeff Horwich is the senior economics writer for the Minneapolis Fed. He has been an economic journalist with public radio, commissioned examiner for the Consumer Financial Protection Bureau, and director of policy and communications for the Minneapolis Public Housing Authority. He received his master’s degree in applied economics from the University of Minnesota.