Author

This article—part 1 of 2—summarizes the state of agricultural borrowers over the past five years and examines the stresses on agriculturally concentrated banks in the Ninth District. As the agricultural sector continues to be exposed to weak global commodity prices, banks in the district face a more difficult lending environment. We report that farm incomes and balance sheets have deteriorated, but the impacts on Ninth District banks have been minimal to date.

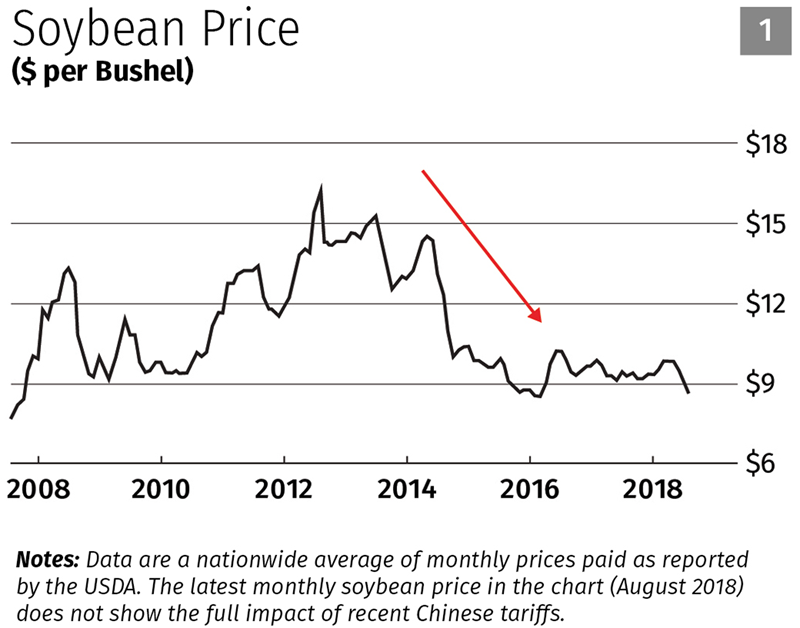

Agriculture in the Ninth District is driven by commodity crop production and, to a lesser extent, by ranching and dairy operations. Commodity crop prices peaked at very high levels in 2012 and stayed elevated through 2013, raising net incomes and reducing the leverage of farmers. Since that time, prices have declined due to slowing Chinese demand, bumper crops in South America, and tariffs on soybean sales

to China.

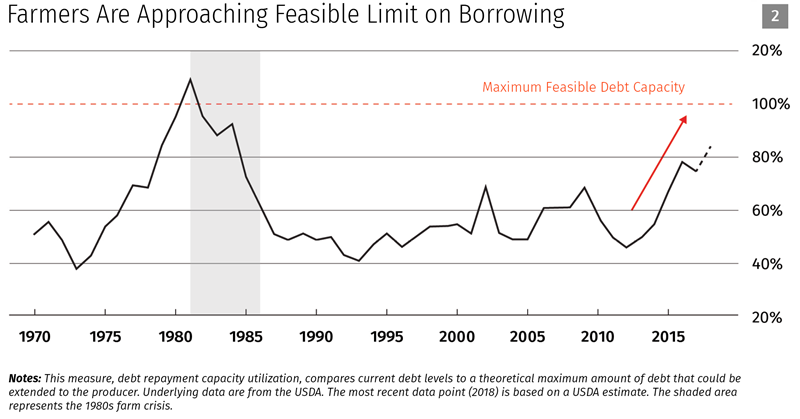

Commodity price weakness (Figure 1) has contributed to lower farm earnings. The U.S. Department of Agriculture forecasts that farm net income will decline in 2018, marking the period from 2016 to 2018 as one of the worst for farm income since the 1980s farm crisis. As Figure 2 shows, lower incomes are adversely impacting the ability of farm households to take on more debt.

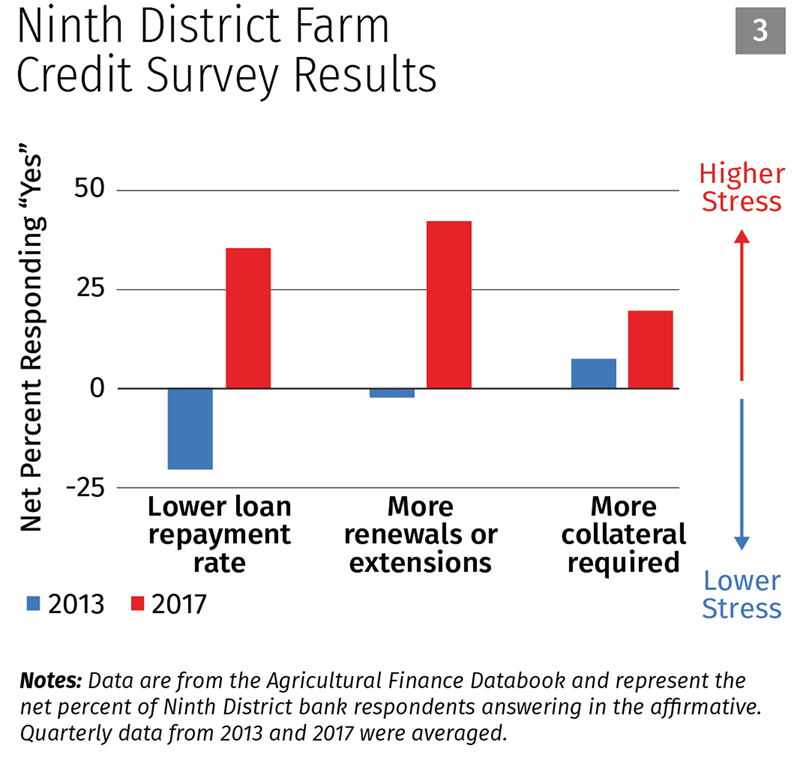

Consistent with these difficult conditions, recent Federal Reserve survey data suggest that banks see declines in customer land values (Agricultural Finance Databook, 2018). They are also experiencing lower farm loan repayment rates and greater demand for loan renewals and extensions. Finally, lower land values are leading banks to ask for additional collateral for outstanding loans (Figure 3).

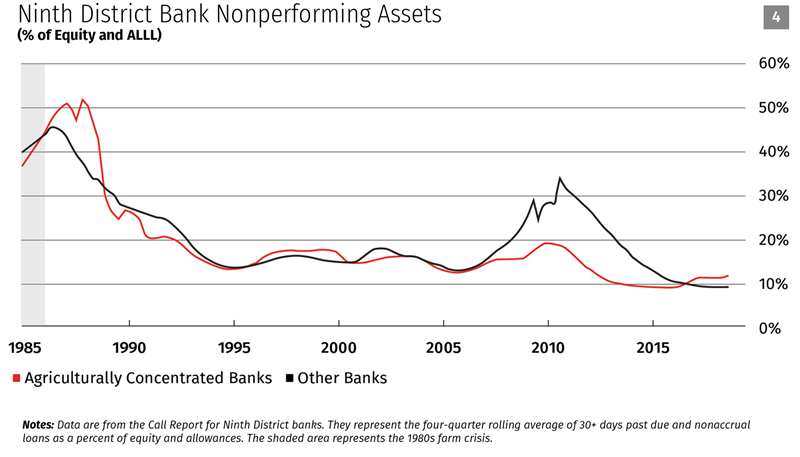

The challenges farmers are facing in the global commodity markets could ultimately impact Ninth District banks. Recent soybean tariffs have added to these difficulties. Despite headwinds, borrowers continue to make their payments on time. This is due to many factors. Off-farm income from working spouses plays a much larger role than it did in the early 1980s, augmenting low farm income. Increased borrowing capacity is also a factor. Farmers are able to tap much more equity than in the past, and banks are willing to roll over large volumes of existing debt. As a result, total nonperforming assets remain at levels well below the post–farm crisis period (Figure 4).

Equity and allowances are a bank’s protection against losses. Decisions about the level of earnings to retain for building equity capital or allowances help determine the bank’s capital resiliency. In part 2 of this article (coming in the first-quarter 2019 issue of Banking in the Ninth), we will explore the capital planning decisions made by Ninth District institutions in the face of mounting pressures in the agricultural sector.