Author

Sarah Dewees

First Nations Development Institute

Financial empowerment is an important step towards personal empowerment and self-determination. Financial knowledge and financial capability are important building blocks for homeownership. The National Native Homeownership Coalition (NNHC) recently invited one of its members, Sarah Dewees of First Nations Development Institute, to present via webinar a report she co-authored on the topic of Native financial capability. Sarah also recently served on the Center for Indian Country Development’s Leadership Council, an advisory group of experts on Indian Country economic development issues.

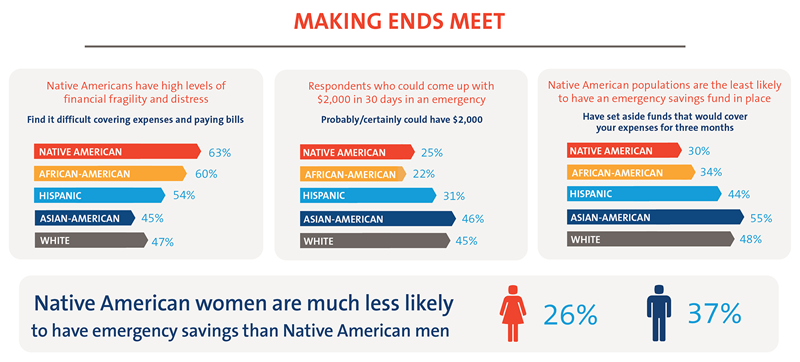

According to the report, titled Race and Financial Capability in America: Understanding the Native American Experience, American Indian and Alaska Natives (AIAN) face difficult financial circumstances and experience high levels of financial fragility, even relative to other minority groups. First Nations Development Institute (First Nations) and the FINRA Investor Education Foundation (FINRA Foundation) published the report which provides new information about the financial knowledge, behavior, and opportunities of American Indians and Alaska Natives. This report drew upon the FINRA Foundation’s National Financial Capability Study (NFCS), one of the largest financial capability studies in the U.S. The most recent National Financial Capability Study included nearly 600 people who self-identified as American Indian or Alaska Native. This is one of the largest samples of Native American respondents in any survey addressing financial behavior.

The report highlights some striking insights about American Indian and Alaskan Native’s challenges with accessing and managing financial products 1) Why do AIANs have a relatively high usage of payday loans and pawn shops? 2) How well can AIANs mobilize in a financial emergency? 3) What is the relationship of AIANs to conventional products like a checking or savings account? Beyond addressing these questions, the findings show promise in Native communities. The gap starts to disappear as household income increases. For example, 63% of AIANs with $50,000 or less in household income are considered financially fragile versus only 25% with household incomes over $50,000. Based on evidence in this report, as economic growth and per capita incomes continues to be on the rise in Native communities, the gap in financial capability can be expected to shrink.

The Center for Indian Country Development recently had a chance to chat with report co-author Sarah Dewees from First Nations Development Institute:

CICD: What are your main takeaways from this work, in relation to supporting homeownership?

Dewees: The findings in this report have several implications for homeownership programs. First, it is clear there is still a need for financial education in many communities. This can be an ongoing effort. In addition, there is a need for safe, affordable financial services such as checking and savings accounts and mortgages. But poverty and low incomes remain a challenge. Homeownership programs can provide financial education and also help individuals find a down payment for home purchase. This combination, along with ongoing support, is a winning formula for supporting homeownership.

CICD: Getting nearly 600 Native American people to respond to a survey about financial issues is impressive. Can you tell us more about your sample?

Dewees: The National Financial Capability Study is one of the largest financial capability studies in the U.S., with over 25,000 respondents. National and state-level findings are based on the 2015 State-by-State Surveys. We had good participation in Alaska and Oklahoma, where 8 and 11 percent of our respondents, respectively, came from. In addition, another 20 percent of respondents came from states with high Native American populations, such as New Mexico and Arizona, so we feel the survey captured a good cross-section of Indian Country. The FINRA Foundation made an effort to include as many Native Americans as possible, and met with staff at the National Congress of American Indians and others to also include questions that would be useful for Native American researchers. Guided by the U.S. Census’ approach to self- identification, the survey allowed people to identify with one or more racial or ethnic group. Nearly 600 people who participated in the survey stated that they identified as American Indian or Alaska Native alone or in combination with some other race. Survey respondents answered detailed questions about their financial knowledge, behavior, use of financial services, and levels of financial distress. This is one of the largest samples of Native American respondents in any survey addressing financial behavior.

CICD: What do you hope people will get out of this work?

Dewees: I think it is important to shine a light on the financial struggles in American Indian and Alaska Native communities. I hope this work highlights the need for ongoing financial education and asset building programs. Because, on average, only 64% of American Indians and Alaska Natives have a savings account may mean that extra work will be needed to help these homeowners come up with a down payment. But some of the findings in this report are hopeful – we found that among those respondents with higher incomes, there was higher financial knowledge, less use of payday loans, and more savings for the future. As tribal economies improve, financial capability may follow.

To download a copy of the report, visit the First Nations Development Institute Knowledge Center or the FINRA Investor Education website.