Author

Jennifer Weil is a person with a lot on her plate.

A first-year graduate student at Minnesota State University-Moorhead, she’s studying counseling and student affairs. She’s also state chair of the Minnesota State University Student Association, and she works in the academic affairs office as a graduate assistant.

Immediately out of high school she attended the state university in St. Cloud, Minn., but left after one year after getting married and then starting a family. She returned to college several years later in the belief that having a degree would better provide for her two boys. That decision was a prescient one after her marriage ended in divorce. A mother with two small boys, Weil fits in motherhood, classes and an estimated 40 hours of work per week.

If that feels like a heavy load for one person, she’s got a financial burden to match, coming out of her undergraduate studies with $42,000 in debt—about twice the level of the average four-year graduate; much of the debt difference for Weil came from private student loans to pay for day care while tending to class and work.

So you might say that Weil has a unique perspective on the college experience—and particularly its costs—having firsthand experience and as the voice of students statewide.

“It’s ridiculously expensive,” said Weil. Among her peers, Weil said her level of debt “is fairly common.”

For Weil, her debt means different choices, both now and in the future. She has always worked at least part-time to help pay for school—from being a Mary Kay beauty consultant to various gigs in student government and now the Student Association. But working during college is a fact of life for many students.

“Almost everybody I know has at least one job. Students have to work significantly more hours a week just to pay for tuition.” And despite all that work while in school, Weil understands it will take still more work after graduation to pay off her debt, requiring further sacrifices. For example, she said, “because of the number of years it’ll take to pay that [debt] off, I’ll have to wait to purchase a house. It’s very difficult.”

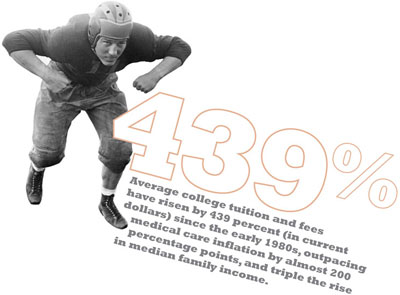

Weil might not exactly be the poster student for college today, but she represents part of the growing angst over the rising cost of higher education. According to the annual Measuring Up report by the National Center for Public Policy and Higher Education, average college tuition and fees have risen by 439 percent (in current dollars) since the early 1980s, outpacing medical care inflation by almost 200 percentage points, and triple the rise in median family income.

Families are worried about the cost of college. Weil said she helped at a booth at the Minnesota State Fair sponsored by the Minnesota System of Colleges and Universities (MnSCU) in late August. Cost, she said, “was a huge topic for families” because parents have been laid off and investment portfolios have shrunk. “The money that was set aside or planned for [for college] is gone now. People feel the crunch of the economy,” Weil said.

College has never been cheap, exactly; but its cost used to be heavily subsidized for students. Over time, costs have risen steadily, and a larger portion of that growing bill has been laid on students and families. For the first time in history, tuition this year at the University of Minnesota is expected to contribute more revenue to the operating budget than state funding. South Dakota State University crossed that threshold two years ago.

This trend didn’t come quickly or by surprise. It’s the result of many colliding factors, from fickle state support to rising enrollments to escalating higher education expenditures—each of which is similarly driven by a variety of factors.

Over time, a mentality has evolved that college is too expensive. For the better part of two decades, university officials, policy wonks, students and their families have criticized the slow evolution of a higher-tuition, higher-aid model as unsustainable.

But its dogged survival has demonstrated the opposite, as students streamed through college doors because they saw a favorable value proposition: Go to school, maybe have to take out a few loans, but graduate and get a much better job earning a lot more money than without a degree. Tuition’s also not as expensive as it often looks, thanks to a lot of grant aid in myriad forms. (For an analysis of the value proposition of college education, see Is College Unaffordable? in the December 2005 Region.)

Enter the recession. While recessions are nothing new, and college enrollment typically grows during such events, the scale of this recession has sent a shock through consumers and intensified much of the existing cost tensions between higher education systems and their customers.

As in other areas of consumer spending, this recession will likely test the implicit assumption that (net) tuition and student debt can rise with little consequence to enrollment or higher education generally. Already, even amid growing enrollments, there are signs of subtle shifts in choice. What remains unknown is whether college preferences will reset along traditional lines once the recession is over and job growth resumes, or if the higher education model is in for a more fundamental shake-up.

The good old days

You have to go back a few decades to see how higher education got to this position. In virtually every way, higher education was a smaller, simpler endeavor. A narrower slice of (only) young people attended college, and the cost of attendance was kept artificially low through state appropriations to colleges. Slowly but steadily, the system evolved: More students started going to college, and state and higher education budgets both got swamped by additional spending priorities. The cost to go to college rose progressively higher as a result, and an increasing share was passed on to students.

As costs climbed, students sought more financial aid to fill the gap between the expense of college and their savings and work income. And many were successful in finding grant money to help buy down the cost of tuition. An array of grant programs has meant that net tuition (after grants are subtracted) has gone up less steeply; in fact, according to the College Board figures, net tuition has gone down at two-year colleges this decade. But it’s risen by 32 percent at four-year public universities.

Comparable net tuition and fee figures over time were not available among all district states, and they likely vary widely because published tuition and grant levels, and their change over time, differ significantly across states and institution types. For example, published tuition rates at two-year schools run 20 percent to 90 percent higher in district states compared with the national average. In much of the district, net tuition and fees are higher: For the 2007 school year, net tuition and fees at Minnesota’s public two-year colleges were 194 percent higher than the national average, and they were 85 percent higher at the state’s four-year universities, according to information from the Minnesota Office of Higher Education.

At the same time, many students are either not eligible for or cannot find grant aid, and in general, the supply of grant money has not kept pace with the rise in tuition. So students have increasingly sought loans to finance college, and average debt of graduates has risen substantially. (For a detailed discussion of these historical trends in the Ninth District, see College finance 101: A history lesson.)

Fast forward to today. Even in recession, higher education institutions have had difficulty reining in tuition. At the University of Minnesota and MnSCU schools (the latter comprised of seven universities and 25 two-year colleges), tuition for the current school year was upped by 7.5 percent and 5 percent, respectively. Thanks to federal stimulus funds, those rates were subsidized down to 3 percent and 2.8 percent. (See Chart 1 for changes in tuition this decade.)

Among Wisconsin’s technical colleges, “realistic” growth of FTEs this year is 10 percent, according to Morna Foy, vice president with the Wisconsin Technical College System. She added that growth “could be much higher,” given that half of the state’s 16 technical colleges are expecting increases of at least 15 percent this fall. Last year saw an FTE rise of 5 percent.

Four-year universities do not expect to match that growth, but many are expecting higher-than-average enrollment this year. Brad Eldredge, director of institutional research for the Montana University System (MUS), said via e-mail that it was too early to confirm this fall’s enrollment, but added that “our sense from preliminary numbers is that enrollment growth will be strong.” Preliminary figures from the University of Montana-Missoula estimated a 5 percent increase over last year’s enrollment—which was itself a record.

Credit for the enrollment surge, according to Foy, Eldredge and other higher education officials across the district, is given almost universally to the recession. As one source put it, “It’s a socially acceptable form of unemployment” as young adults and unemployed workers seek better skills in hopes of becoming more marketable in the future job market. It’s even attractive to employed workers interested in greater job security or flexibility, knowing that they could be next in the unemployment line.

Of course, the recession comes with an ugly side for students and higher education institutions alike. For example, parents still fund a significant portion of college costs, and when one or both lose a job, it strains their ability to afford tuition out of savings or income. The same goes for students; over the past decade and a half, and particularly in this recession, teenagers and other young adults have had a rough go of it in the job market, which means they also do not have much savings or regular income to pay for college. Such circumstances imply that student debt is likely to continue climbing, possibly steeply.

Adding salt to this wound is the fact that, even before the recession, incomes had not kept pace with college costs, and prices for other basic student needs also have outpaced inflation by a large margin. According to the College Board, average room and board costs have increased by 23 percent above inflation during the past decade. From fiscal year 2004 to 2008, tuition and fees at the University of Wisconsin-La Crosse rose by 17 percent, housing costs rose by 12 percent, and the most popular meal plan rose by more than 7 percent, according to this year’s UW System Fact Book. (All figures are adjusted for inflation.)

A helping hand (into debt)

For existing and prospective students, the challenge for many is finding the necessary means to pay for college. Getting a firm handle on the extent of financial need in the district today is tricky for two reasons. First, state-specific data on financial need—the number of aid applications, amounts requested and approved, and the financial gap between approved aid and demonstrated need—typically lags at least a year.

Second, compounding the matter is the fact that financial aid packages are based on the previous year’s income. So even last year, some sources said, financial aid trends didn’t appear dramatically different because aid packages were based on student and family income from 2007, when the economy was still upright.

“If there was an acceleration (of financial need) in 2008–09, we didn’t see it very clearly,” said Greg Stringer, a senior vice president at Great Lakes Educational Loan Services, a federally designated guarantor for student loans in Minnesota, South Dakota and Wisconsin. Headquartered in Madison, Wis., the company services loans for more than 2 million borrowers and holds loan guarantees on nearly $51 billion under the Federal Family Education Loan Program, one of the major federal student loan programs.

Stringer and other sources said they are seeing more signs of financial need today. He ticked off a number of reasons—higher joblessness, tighter credit standards from banks for credit cards and home equity loans, and higher tuition and other costs—that were are all leaving their mark. “Put it all into the mix, and it seems intuitive that demand would be up.”

Lois Larson, director or financial aid at Century College, a two-year community college in White Bear Lake, Minn., said the school had as many applications for aid on file this past August as “we had all of last year for three terms—fall, spring and summer.”

Eldredge said that MUS was also seeing an increase in requests for financial aid; the number at the state’s flagship University of Montana “is up significantly,” and students were demonstrating greater need. Those local events mirror national trends: According to a September survey of 500 financial aid offices by the National Association of Student Financial Aid Administrators, 61 percent reported that financial aid applications were up 10 percent or more.

Financial aid flavor: Rocky road

Though financial aid takes on different forms and comes from a variety of sources, it all boils down to a fairly simple template: grants and loans. The federal government is the single largest provider of both, particularly loans. But states, institutions and private interests also provide a lot of financial aid—in fact, much more grant aid on a cumulative basis than the federal government.

But not all aid is equally palatable, Stringer pointed out. “There is a free-money flavor and a debt flavor, and one of those flavors doesn’t taste very good.”

As is always the case, there is never enough free money to go around, and rising demand for financial aid means even more competition for finite grant resources. A total of 35,000 students in Wisconsin’s 16 technical colleges received need-based grants from the Wisconsin Higher Education Grant program, but more than 15,000 got shut out when funding ran out. That’s more than double last year’s number of unserved applicants, according to Foy.

Still, students manage to find the financial resources necessary to enroll, as evidenced by enrollment growth. Eldredge, from MUS, said students are able to find aid, “but often that aid is in the form of student loans. … [That’s] the only aid that doesn’t run out.” He added that early projections showed student loan volume this year was up between 5 percent and 10 percent.

A September report by the U.S. Department of Education estimated that the total value of federal student loans grew by 13 percent last year and will do so by another 6 percent this year, to almost $92 billion. However, it offered no geographic breakdown on loan demand.

Higher enrollments are driving some of that federal loan growth. But the recession has also shut down other credit sources. For example, the recession and the concomitant slump in housing have cut deeply into home equity, which had been a small but growing source of financing for college. And the shake-up in financial markets also has banks and other for-profit lenders beating a hasty retreat from the private student loan market, which had been the fastest growing segment of student aid.

Bring your checkbook, or else?

While many complain about the rising use of student loans—whatever their source—the alternative might be worse. Without debt financing, millions of students simply wouldn’t be able to afford college.

But higher costs and the growing use of debt financing have also heightened anxiety over college access for low- and modest-income households. High tuition and fees are “more and more of a challenge for those households with limited income,” said David Chicoine, president of South Dakota State University in Brookings. “If we were all rich, there’s not a problem.”

But the current focus on low-income access might not be as intuitive as you think.

According to the National Center for Education Statistics, the gap between students from low-income families (those in the bottom 20 percent of family income) and their higher-income peers narrowed from 1972 to 2006, but differences remain. Still, the rate at which low-income high school graduates enroll in two- or four-year colleges by the following October has risen steadily, even this decade (see Chart 3). In fact, it’s the middle- and high-income high school graduates who have seen their college matriculation rate plateau.

One likely reason for improvement among low-income students is the continued availability of aid—grants and subsidized loans—for those who can demonstrate need (see College finance 101: A history lesson for more discussion). Chicoine said that access for low-income students “might be better than those that are just above that (need) line” who must finance their college attendance via student loans. “If the student has the ability and preparation to get to college, we can put together a package” to get him or her in the doors, he said.

A potentially larger obstacle for many is not their respective wealth (or lack thereof), but their willingness to take on debt to get an education. That’s because debt is often “something (students) have worked to avoid,” said Chicoine, even if that means eschewing low-cost federal loans and ultimately “choosing not to go to school based on debt.”

That’s particularly the case for first-generation college students, who often get their views on debt from their more conservative parents. The matter is exacerbated when parents and students look at sticker prices for tuition—a price that few students pay because of widespread tuition discounting and scholarships. “What needs to be discussed is not gross cost but the net cost” after various sources of financial aid are applied, said Stringer, from Great Lakes. “A lot of people see the gross price, and they are horrified.”

That’s particularly the case for first-generation college students, who often get their views on debt from their more conservative parents. The matter is exacerbated when parents and students look at sticker prices for tuition—a price that few students pay because of widespread tuition discounting and scholarships. “What needs to be discussed is not gross cost but the net cost” after various sources of financial aid are applied, said Stringer, from Great Lakes. “A lot of people see the gross price, and they are horrified.”

Many students also drop out when they can no longer pay for college out of their own pocket. Some take a semester or two off, hoping to save up enough money to pay for a return down the road. But research shows that many never go back.

While there is some utility—even trendiness—to frugality today, an absolute stance against debt can be counterproductive for a young person. “There are levels of debt that are affordable. If you’re going to be a school teacher, there’s a (total debt) number out there” to help you figure out what program is the best fit, Stringer said.

Tell that to the bill collector

But that view also competes with a rising din of anecdotes from students who didn’t pay much attention to debt levels and their career choices.

Whether student debt is manageable depends on a person’s income after graduation. Despite a plethora of stories about what seems to be excessive student debt, the college wage premium suggests that student loan debt generally must be manageable—if maybe unpalatable—for the majority of borrowers. Were it not, students would most certainly start making different decisions.

At the same time, surprisingly few data are available on the net financial burden of student debt. Figures for average debt are widely accessible, but that likely hides a significant amount of variation—and possibly shifting choices—among career paths.

It’s not that educational institutions are uninterested in such matters. “We definitely try to track it. We’re asking, but the other side is (students) need to respond” to income surveys they receive, said Gavin Leach, vice president of finance administration for Northern Michigan University in Marquette.

Loan defaults can offer some insight on debt management. National default rates on federal student loans, for example, are on the rise, at 6.7 percent for 2007, the most recent figures available from the U.S. Department of Education. That’s up significantly from 4.6 percent in 2005.

But it’s not all bad news. The rate among most district institutions, for example, is considerably lower (though also rising); statewide rates in the district run between a low of 2.3 percent (Montana) and a high of 3.8 percent (South Dakota). Rates nationwide were also much higher two decades ago, peaking at 22 percent in 1990. Those have come down significantly, thanks mostly to changes in federal lending programs that gave borrowers greater repayment flexibility.

Still, more financial trouble appears to be brewing. Stringer, from Great Lakes, said his organization has seen “a sharp increase in the number of delinquencies and defaults this year.” But students also have more leeway in repaying education loans compared with other consumer loans. With student loans, Stringer said, “there are lots of temporary release valves that allow loan payments to be put into suspension while things work themselves out.” A new income-based repayment option was also introduced this summer that caps loan repayments at 15 percent of discretionary income.

What, me worry?

As students and their families scramble to finance college, institutions face their own challenges that will likely add still more pressure to higher education costs.

Higher education institutions generally have high fixed costs, thanks to a huge assortment of programs, mostly tenured faculty and expansive facilities. As a result, they depend on reliable streams of (increasing) revenue. But some of those streams might not run as fast as they have in the past. For example, though state appropriations to higher education this decade have been generally modest, even meager in some places, they will nonetheless be under constant threat for the foreseeable future in many states—including Minnesota and Wisconsin—that are staring at huge structural budget deficits.

Or consider university endowments. Many schools receive significant contributions from them, but the collapse of financial markets last year put a serious dent in many endowments. The district’s largest endowments rest at the University of Minnesota Foundation ($1.4 billion) and the University of Wisconsin Foundation ($2.3 billion). Each grew greatly in recent years, and their universities benefited richly: In 2008, foundation disbursements to the University of Minnesota were almost $100 million, a 21 percent increase over 2007. The Wisconsin Foundation did that one better, distributing $203 million to UW-Madison last year.

Whether or not universities can count on similar contributions is likely being reevaluated in light of a disastrous investment year. The UW Foundation assets dropped by 23 percent in 2008, with losses of almost $600 million. (The U of M Foundation has not reported investment results for the second half of 2008 and early 2009). Such endowment pain is widespread. UW-Superior, with about 2,300 students, reportedly awarded $100,000 less this year in endowed scholarships due to investment losses.

Institutions have also been receiving significantly more revenue from research contracts over time. That funding might hold out; even if it does, however, it’s not likely to relieve student costs because such revenue is typically dedicated to noninstructional types of expenditures, such as research staff, equipment and project administration.

With these revenue challenges, there will be growing pressure to have students fund more of their own instructional costs via tuition and fees, which means colleges and universities will also depend on strong enrollment. This isn’t a problem for the time being—in fact, many institutions are more likely overcrowded—but it might be down the road, because the pull of higher education during recession is expected to wane with economic recovery.

Colleges and universities also are watching two demographic shifts roll through high schools, particularly in slow-growth states like those in the district: First, a steady decline in the number of high school graduates; second, an ethnic shift among those who graduate.

North Dakota has already had a glimpse of the high school future: The number of high school graduates there dropped by almost 10 percent from 2004 to 2008. It’s projected to fall another 15 percent by 2016, the largest drop among district states (see Chart 4). But the trend hits high schools in every district state. That will have a trickle-up effect on all colleges and universities.

“I’ve never seen (a decline), certainly not to this degree,” said David Laird, recently retired, but at the time of the interview, president of Minnesota Private Colleges and Universities. “The decline in Minnesota is almost entirely in white, middle- and upper-class students,”—in other words, the traditional bread and butter of higher education, particularly for private colleges. Most future enrollment growth will come from ethnic populations that are traditionally underrepresented in college and culturally tend to be more debt averse than their white counterparts—a potentially serious obstacle given the role of student loans in financing college today.

And … what?

Students and institutions alike are also staring wide-eyed into the worst job market for graduates in decades. Anecdotes on the matter are rife, but consider a handful of surveys by the National Association of Colleges and Employers, an industry group connecting career service professionals at nearly 2,000 colleges and universities nationwide with thousands of staffing professionals.

Last spring, a NACE survey found that two-thirds of the class of 2009 were worried about their job prospects. It turns out they had good reason: Employers expected to hire 22 percent fewer new grads than from the previous year. Last May, NACE reported that just 20 percent of grads who had applied for jobs had been hired, down from 26 percent and 49 percent the previous two years; the percentage of grads even applying for jobs has also dropped each of the past two years. Then this fall, it reported that graduates who did find jobs saw their starting wages fall by 1.2 percent over the 2008 class. Finally, 55 percent of college career centers reported budget cuts for the coming year, and only 5 percent saw increases despite a potentially huge increase in demand for their services.

In the district, it appears to be much the same. A survey released in September by the St. Cloud State University Career Center found that 16 percent of respondents planned to decrease graduate hiring, up from 7 percent a year earlier. Employment markets are not expected to rebound quickly: The Minneapolis Fed’s July forecast predicts that total nonfarm employment will decline further in 2010 in Minnesota, Wisconsin, South Dakota and the Upper Peninsula of Michigan, while Montana and North Dakota will have below-average (but positive) job growth.

Add up all of these colliding factors—higher costs, higher debts and an unsettling employment outlook for students; higher expenditures, a shifting client base and constrained revenue streams for institutions—and you’ve got the proverbial irresistible force and immovable object. Will students become more price sensitive? Is the current anxiety on both sides short lived, a figment of the economic times?

Time will tell, but chatter over college costs is getting louder. Steven Schuetz, vice president for admission and financial aid at Ripon College, a private school in Ripon, Wis., outlined much of the problem facing higher education, especially on the upper end. “Already, we are finding that all institutions need to justify their increases, and those above inflation are harder and harder to justify to families even though the cost of doing business is going higher. At the higher end of the tuition scale, we will have to eventually ask ourselves, ‘Are we worth $50,000 a year?’”

But students are looking at different options. For example, online enrollments are growing fast. While most colleges and universities offer online courses, there appears to be significant leakage to private online colleges. In 2008, fall head count at Minnesota’s two online universities (Walden and Capella) increased by 17 percent over the previous year, to 60,000 students.

Among traditional institutions, two-year colleges have seen easily the largest enrollment surge. Some of this is likely a function of rising job dislocation and career retraining, which technical and community colleges specialize in. But even before the recession, two-year colleges were out-polling four-year institutions. In Montana, two-year colleges saw enrollment from 1998 to 2008 grow by 25 percent, compared with an increase of just 6 percent for the university system as a whole and 5 percent for the state flagships, Montana State University-Bozeman and the University of Montana-Missoula. This fall, Montana Tech reported an 11 percent increase in its head count.

Larson, from Century College in Minnesota, said the choice of a two-year college makes affordable sense in today’s economic environment. “Think about it for a second. A student loan at this time nicely covers half-time enrollment costs at a two-year college, and then the rest is sent to the student for living expenses. If you are hungry, going back to college can be a short-term fix as well as a long-term goal. I think all [higher ed institutions] will see an increase in applicants. But the increase in enrollment will pass down the food chain to lower-cost colleges, at least for now.”

“My instinct is that yes, families are becoming more cost-conscious, at least on the margins, not wholesale. It’s not dismissing the idea of college but changing what you want to do,” said Stringer, from Great Lakes. That might mean choosing an in-state public university because “they can’t send Johnny or Judy across the country to an Ivy League school anymore.”

Chicoine, from SDSU, believes schools like SDSU might be the destination of prodigal students—those who transfer from expensive out-of-state or private institutions when families can no longer rationalize the expense. Laird, from Minnesota’s private colleges, said more students were looking at premier public universities like UW-Madison as a lower-cost alternative.

New and improved! Great value!

Educational institutions are also taking a fresh look at how to deliver services. For example, the UW System is exploring the possibility of accelerated three-year baccalaureate degrees. In an attempt to tackle skyrocketing textbook prices, half of the system’s four-year campuses have implemented rental programs. The system has also considered additional fees for high-cost fields that also offer higher salaries, like engineering.

In the midst of budget pressures, some institutions are even looking downright businesslike. Facing state appropriation reductions, the University of Minnesota was staring at $90 million in budget reductions and reallocations this year. The Board of Regents took the unprecedented step of cutting more than 1,200 jobs—including 220 faculty positions.

Elsewhere, faculty are having to swallow hard to avoid what’s behind door number two. Earlier this year, the unions representing the MnSCU’s 32 institutions agreed to a two-year salary freeze. At the Montana University System, tuition was kept constant at all campuses for the 2007–2008 biennium. It will remain flat over the coming two years at most campuses, and will rise by 3 percent annually only at MSU-Bozeman and UM-Missoula. Eldredge called this level of tuition stability “unprecedented.”

Opinions varied as to whether actions by students and institutions are the first steps in a new direction for higher education or a necessary reaction for muddling through the recession.

“My sense is that there is going to be a softening [of price sensitivity by students] once the economy recovers,” Chicoine said. He and others pointed out that the world needs more—not less—skilled labor in the future, and that means a university classroom seat will continue to be a finite resource, particularly if state and federal funding remains scarce. Regardless, higher education needs to be seen “as an investment, and not a current expenditure … [because] there is no substitute for human capital” for long-term economic growth, Chicoine said.

That doesn’t necessarily mean that college costs can resume their ascent once the economy recovers. A few sources believed there is an as-yetunknown cost point at which the return on a college degree is no longer obvious and students will start making different choices.

“I don’t know where the [affordability] line is, but it’s out there where families will change their horizons on a more permanent basis,” said Stringer.

College degree: Earning its keep

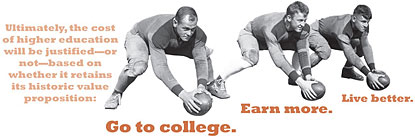

Ultimately, the cost of higher education will be justified—or not—based on whether it retains its historic value proposition: Go to college. Earn more. Live better.

Of course much of that value proposition depends on who’s paying, and that’s not always straightforward because research has shown that both the individual and society as a whole benefit from the human capital growth that occurs through higher education. But there is no clear line demonstrating how much each party needs to pony up for its share of the benefits.

“I don’t know if there is a theoretical balance” between the public and private share of higher education investment, said Chicoine. If that’s true—and there’s virtually no research that even takes a stab at a hypothetical equilibrium—then students and higher education systems will have to continue feeling their way along the cost ladder.

Chicoine pointed out that college students “make decisions all the time” based on their understanding of costs and benefits. Average student debt at the university rose from $14,200 at the start of the decade to $20,800 in the 2008 school year. At the same time, median wages for workers in South Dakota with four or more years of college were about 60 percent higher in 2006 than for those with a high school diploma, according to figures compiled by the Federal Reserve Bank of Minneapolis. So taking on some debt to earn a degree, Chicoine said, “is a good, rational decision. The evidence of the value proposition is pretty robust.”

Some might think that the cost issue is more pressing for private institutions with higher tuition and fee costs. But that depends on how you interpret value. Average debt is higher for graduates of these institutions. But fourand six-year graduation rates from Minnesota’s private four-year schools are significantly higher than those of public universities in the state (including the University of Minnesota), and entry into the workplace a year after graduation is also much higher. That means private college grads start earning their wage premium earlier and begin paying off their debt sooner.

But Laird, representing Minnesota’s private colleges, also acknowledged that all schools are on a slippery cost slope considering the economic conditions today, and have to be part of the solution. “Could institutions behave differently? If they had some necessity or benefit, sure,” said Laird. “These institutions are not incapable of making very dramatic changes when necessary, or when there are incentives to do so.”

Ron Wirtz is a Minneapolis Fed regional outreach director. Ron tracks current business conditions, with a focus on employment and wages, construction, real estate, consumer spending, and tourism. In this role, he networks with businesses in the Bank’s six-state region and gives frequent speeches on economic conditions. Follow him on Twitter @RonWirtz.