Perceptions of increasing risk within and outside the banking sector have contributed to the credit crisis, and these perceptions are reflected in

the wide fluctuations and volatility seen in bank funding markets.

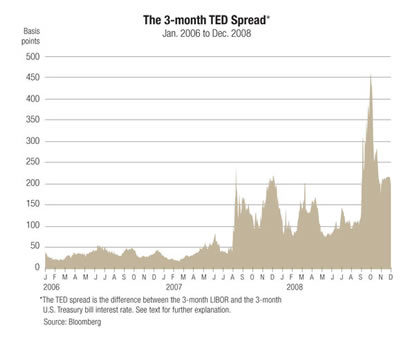

One key measure of perceived risk and volatility in markets is the TED spread.1 The TED spread is the difference between the London Interbank Offered Rate (LIBOR) (the benchmark for the interest rate banks charge one another for loans) and the rate on comparable-term Treasury bills, usually 3 or 6 months. Because a Treasury bill is considered a risk-free security, the difference between it and LIBOR, which is a gauge of banks' confidence in each other, is a good measure of concern in lending markets.

In normal times, the median 3-month TED spread is about 50 basis points (a basis point is 1/100th of a percentage point). Rarely does it rise higher than 100 points. But since August 2007, the TED spread has routinely been above 100, and since early September 2008 has ranged from 200 to over 460, reflecting substantial anxiety about credit risk. On the other hand, the spike seen in early October dropped by early November.

1/ TED is an acronym where T stands for Treasury bill and ED is the ticker symbol for a eurodollar futures contract sold on the Chicago Mercantile Exchange. Eurodollars are U.S. dollars on deposit in commercial banks outside the United States, and prices for CME Eurodollar futures contracts are determined by the market's forecast of the 3-month London Interbank Offered Rate (LIBOR).

Return to: Actions to Restore Financial Stability

{kind=link}