Authors

Toby Madden

Regional Economist

The slow housing sector, tighter credit conditions, and higher energy and food prices have contributed to a soft district economy. According to the Minneapolis Fed's forecasting models, soft economic growth will continue into 2009. On a positive note, growth in manufacturing and natural-resource-based sectors and increases in personal income could keep the economy from slowing further.

Housing continues to hamper economic growth

During the recession of 2001, relative strength in residential investment helped keep the economic contraction relatively mild. In contrast, since the second quarter of 2006, the downturn in residential investment has shaved about 1 percent off the annual rate of U.S. gross domestic product growth each quarter through the first quarter of 2008. While the U.S. economy hasn't dipped into a recession, the housing slump accounts for a good share of the recent slowdown.

At the district level, housing units authorized decreased in all states during 2006 and 2007, with particularly large decreases in Minnesota and Wisconsin (see PDF for charts). Furthermore, languid housing markets have led to declines in home sales and prices. Decreases in sales of existing homes from the first quarter of 2007 to the first quarter of 2008 ranged from -2 percent in South Dakota to -24 percent in Wisconsin. The average home price decreased 10 percent in Minneapolis-St. Paul and 3 percent in Sioux Falls, S.D. The Minneapolis Fed's forecasting models suggest that housing units authorized will begin a recovery in some states during 2008 and 2009. (For a broader discussion of housing trends in the Ninth District since 1999, see "A man's home is his unsold castle.")

Recent strains in financial markets are attributed in part to weakness in the housing sector. Home foreclosures have increased, and mortgage and consumer credit requirements have tightened. Large commercial banks have written off billions of dollars of mortgage loans.

Credit standards for many types of loans have tightened, a potential constraint on consumer spending. Furthermore, cash-out refinancing levels have decreased as assessed home values have declined. During the first quarter of 2008, the value of home equity cashed out through refinancing of loans owned by Freddie Mac was about one-third the amount during the first quarter of 2007.

Despite tightening in credit standards, the amount of consumer credit outstanding increased 5.4 percent at an annual rate in the first quarter of 2008, only slightly lower than the 5.7 percent increase for 2007. Personal income has also continued to climb, a good sign for consumer spending, although growth slowed during the first quarter of 2008. Consumer spending grew 1 percent during the first quarter, compared with 2.3 percent growth during the fourth quarter of 2007. This result mirrors a recent informal survey of district retailers that suggests continued modest growth in consumer spending. However, adjusted for inflation, consumer spending has fallen.

Energy and food prices increase

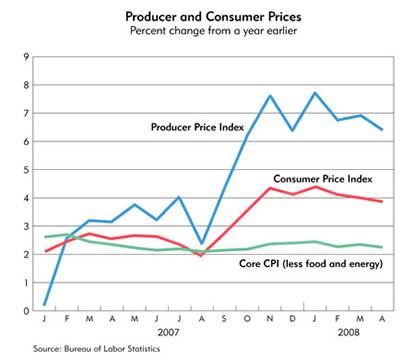

Consumers are facing higher energy and food prices, but the core rate of inflation remains relatively tame. The Consumer Price Index in April 2008 was 3.9 percent higher than in April 2007. Once prices for energy and food are removed, the core CPI in April was 2.3 percent higher than a year ago. Nevertheless, energy and food represent about 20 percent of total personal consumption expenditures, and higher prices mean less spending on other goods and services, particularly for lower-income households.

Consumers are not the only ones facing higher costs—so are producers. The Producer Price Index, which measures inflation at the wholesale level, increased 6.4 percent in April compared with a year ago.

Employment flat; manufacturing aided by exports

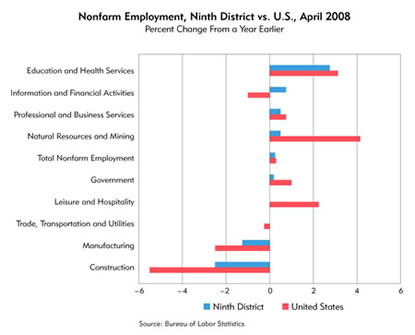

Labor markets have slackened, with virtually no growth and higher unemployment rates. District nonfarm employment grew 0.2 percent in April compared with a year ago. Education and health services showed the strongest gain in employment (2.7 percent), followed by information and financial services (0.8 percent). Meanwhile, employment levels in manufacturing decreased 1.2 percent and construction employment dropped 2.4 percent. The Minneapolis Fed's forecasting models point to stagnant employment growth and higher unemployment rates into 2008 and 2009.

Despite the decrease in employment levels, output in the manufacturing sector has increased in Minnesota and the Dakotas, according to a May survey of purchasing managers by Creighton University (Omaha, Neb.). Manufacturing output has been buoyed by steady growth in exports as the world economy has grown faster than the U.S. economy and the exchange rate of the dollar relative to other currencies has made U.S. goods less expensive abroad. During the first quarter of 2008, growth in manufactured exports from district states ranged from 8 percent in Minnesota to 44 percent in North Dakota.

In addition to a healthy manufacturing sector, the mining and oil drilling sectors in the western part of the district remain active in the context of strong metal and energy prices.

Farmers get a late start on 2008

Large harvests and high prices boosted farm profits in 2007. However, the first half of 2008 has seen higher input costs and delays in planting. Ranchers are getting squeezed with rising feed costs and stable output prices. Ethanol and biodiesel continue to affect district agriculture. Land prices continue to increase, and many are wondering if prices will peak in 2008. (For a detailed discussion of farmland prices and related ag issues, see the cover article in this issue of the fedgazette.)

According to the Minneapolis Fed's first-quarter (April 2008) agricultural credit conditions survey, 2007 was a strong year for agricultural income, with 90 percent of survey respondents reporting increased income. Agricultural lenders are somewhat optimistic for farm profits in the second quarter of 2008, with 61 percent expecting increased income and only 5 percent expecting decreased income.

Farmers are concerned about the start of 2008. Due to foul weather in many parts of the district, planting was delayed and corn and soybean crop progress is slow. This may negatively affect yields at harvest time. The western Dakotas and eastern Montana are in a severe drought, although the heavy mountain snowpack bodes well for reservoirs and irrigation. So far the wheat crop appears in good condition.

For farmers, the outlook for prices is strong. Corn, soybean and wheat prices are all expected to increase from 2007 into 2008 and further increase into 2009. The outlook for revenues is mixed, as higher prices may be somewhat offset by lower yields. Profits may not be as large as in 2007 due to increased input costs, including fuel and fertilizer.

For animal producers, the outlook is not as bright. Profits are squeezed by higher costs and flat selling prices. The increased demand by bioenergy producers has put upward pressure on crop prices. This has driven feed costs up for those cattle ranchers who are not near an ethanol plant. In addition to feed, fuel and other costs have also increased. Cattle, hog and milk prices are expected to stabilize in 2008 from 2007 levels and increase slightly in 2009.

| AVERAGE FARM PRICES | ||||

|---|---|---|---|---|

| 2005/ 2006 |

2006/ 2007 |

Estimated 2007/2008 | Projected 2008/2009 | |

| (Current $ per bushel) | ||||

| Corn | 2.00 |

3.04 |

4.20-4.45 |

5.30-6.30 |

| Soybean | 5.66 |

6.43 |

10.00 |

11.00-12.50 |

| Wheat | 3.42 |

4.26 |

6.50 |

6.75-8.25 |

| 2006 | 2007 | Estimated 2008 | Projected 2009 |

|

| (Current $ per cwt) | ||||

| All Milk | 12.90 |

19.13 |

18.90-19.30 |

18.15-19.15 |

| Choice Steers | 85.91 |

91.82 |

89.00-93.00 |

89.00-97.00 |

| Barrows & Gilts | 47.26 |

47.09 |

46.00-48.00 |

47.00-51.00 |

Source: |

||||