Author

Many people have the notion that hospitals and other health care organizations are high-margin cash cows—I mean, have you seen their prices lately? And how else do you explain all those building cranes?

In fact, many believe the cranes and cash go hand in hand: High prices lead to fat margins; fat margins lead to new buildings; new buildings lead to higher costs; higher costs lead to higher consumer prices, which gets us back to those fat margins.

The health care public, as well as many policymakers, see new buildings as evidence of a medical "arms race" that is unnecessarily and recklessly pushing up costs. Economists, on the other hand, are fond of saying that incentives matter, and if you follow the money, the pattern of capital investment seems to be a rational attempt to attract higher-margin patients as defined by the reimbursement policies of health plan sponsors—employers and government health care programs, mostly.

In other words, some services or procedures are reimbursed at a higher rate than others, and some payers reimburse at higher rates than others for the same service. So when it comes time for capital investment, this tiered reimbursement arrangement influences the decisions of health care providers in predictable ways. Responding to incentives embedded in the payment system, health care organizations often focus their capital investments on high-end procedures and privately insured patients, for the simple reason that they make more money doing so.

Say ahhhhh

To make the connection between reimbursements and capital investment, let's delve into the core of health care finance. Contrary to what many might believe, profit margins at hospitals are low, collectively speaking, fluctuating between about 2 percent and 4.5 percent since 1990, according to the American Hospital Association. But that bottom-line figure obscures a lot of cross-subsidization that goes on for different types of patients.

Margins are low in part because provider costs have been steadily rising. For example, a persistent shortage of doctors and nurses means that staffing costs have been increasing faster than inflation. Hospitals and clinics are also reporting significantly higher costs in recent years for liability insurance, drugs, medical devices and other supplies. They are also seeing more uncompensated care. According to the Wisconsin Hospital Association, for example, the cost of charity care for hospitals in the state rose 20 percent, to $234 million, from 2002 to 2004; bad debt increased even faster, rising from $257 million to $343 million.

The revenue side of the ledger comes largely from third-party payers—government and employers who pay most of the nation's health care costs on behalf of program participants or workers enrolled in a health care plan. Health care providers practice what's called price discrimination, whereby different prices are charged to different parties for the same service. This happens mostly because it can; health care providers serve a multitude of groups insured under different health plans. Depending on its size, each group has a different negotiating leverage, which provides wiggle room in prices and reimbursement rates charged to health plan sponsors.

Government, on the other hand, is the gorilla at the table. For the most part, it can dictate the amount it is willing to pay for a given service or procedure. Hospitals can take it or leave it. Most have to grudgingly accept government reimbursement rates because otherwise they would have to stop serving much of their client base; not only would this have serious organizational ramifications, but it would also violate the missions of most community hospitals, many of which have religious affiliations.

As a result, hospitals and clinics see low and even negative margins for Medicare and Medicaid patients. A survey by the American Hospital Association found that two-thirds of all responding hospitals lost money on Medicare and Medicaid services in 2004. AHA calculated that Medicare and Medicaid underpaid hospital claims by $25 billion on a cost basis in 2005, up dramatically from just $4 billion in 2000.

Both of these entitlement programs represent a unique reimbursement problem for providers. Medicaid, for example, typically represents a small portion of the customer base for most hospitals, though it's often higher for inner city hospitals. More important, Medicaid reimbursements are particularly low; one hospital official in Minnesota said serving Medicaid patients is "community service, really."

In Wisconsin, Medicaid reimbursements to hospitals dropped from slightly above 80 percent of cost in 1997 to 55 percent in 2004, according to the state hospital association. The dropping reimbursement rate is compounded by (as well as the result of) a surge in Medicaid enrollment, up 88 percent from 1998 to 2003. It's like the tongue-in-cheek adage of losing money on every patient, so you try to make it up on volume. The cumulative Medicaid shortfall for Wisconsin hospitals has grown from about $75 million in 1997 to $450 million in 2004.

Medicare reimbursement rates are generally higher, but still below cost, and this population makes up a significant portion of the patient base in virtually every health care facility in the country. A 2006 report by MedPAC, a federal advisory agency for Medicare, found that Medicare margins for hospitals fell from about 5 percent in 2001 to -3 percent in 2004. For rural hospitals, Medicare margins fell from about 0 percent to -4 percent. MedPAC did note, however, that hospitals with consistently negative margins also tended to have a poorer competitive position in their market, with lower occupancy rates and higher costs per discharge.

Still, all of this might seem innocuous enough. After all, government saves billions in taxes by squeezing reimbursements to providers. But health care facilities—even nonprofit ones—won't stay open long if they consistently lose money. So with Medicare and Medicaid patient margins in the red or close to it, health care providers look to privately insured patients (and their plan sponsors) to provide the bulk of their operating margin.

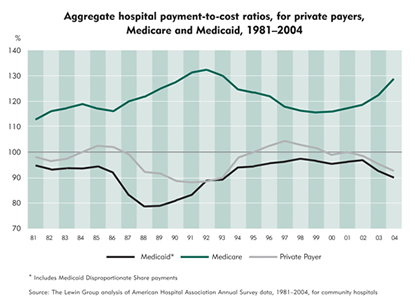

Since 1997, the average margin of private payers has diverged markedly from that earned from Medicare and Medicaid, according to research conducted by the Lewin Group on behalf of the AHA (see chart). In Minnesota, for example, state and federal governments paid hospitals approximately 14 percent below hospital costs—a gap of about $520 million—in 2004, according to the state hospital association. "That means, in effect, the government is shifting the costs of caring for people to commercial insurers," the association noted on its Web site.

Going forward, the matter is likely to worsen. For one, provider costs are expected to continue rising. Even if Medicaid and Medicare reimbursement rates remain stable, employer-sponsored health plans will bear a disproportionate share of the cost increase. But there is ongoing pressure to cut Medicare reimbursement rates in hopes of slowing down overall expenditures by the program, which have climbed steeply because of increased enrollment and higher service utilization by recipients. Current Medicare law even includes a statutory update formula that requires a cut in payment rates for physician-related services when total expenditures exceed a certain amount. This formula was put in place in 2002. Significant rate decreases would have been triggered every year since had Congress not intervened, according to the Centers for Medicare and Medicaid Services.

Not all Medicare reimbursements are created equal, either; rates for some services or procedures are more generous than others. For example, specialized services like heart bypass surgery tend to be reimbursed at higher Medicare rates (in terms of cost) than treatments for more common ailments like pneumonia. A 2005 article in the journal Health Affairs noted, "Although largely unintended, Medicare's payment systems have benefited specialized, procedure-oriented care," such as oncology and cardiac surgery.

This brings us back full circle to the role of reimbursement in health care capital investment: When planning for new facilities and services, organizations will pursue profitable lines of business as a simple matter of survival. Currently, that means sophisticated, intensive kinds of treatment, particularly for individuals with private insurance. That's one reason why, for example, new cancer centers are being developed in both Billings, Mont., and Sioux Falls, S.D., to compete with an existing facility in each city.

Brothers in arms

Many industry sources acknowledged the arms-race controversy; most, but not all, were agnostic about whether it was a problem, and for whom. What a patient (or policymaker) sees as a medical arms race, most health care executives see as a rational pursuit of operating margin in an effort to cross-subsidize many other areas of care that are vital to the mission of any community hospital but money losers in terms of reimbursement.

"I think the discussion follows only the impact on costs" to health plan sponsors, according to George Quinn, from the Wisconsin Hospital Association. Building investments "are meant to serve patients" by offering better treatments, greater comfort and a higher standard of safety. "There isn't enough emphasis on those (traits)."

Jeff Thompson is CEO of Gundersen Lutheran, a health care provider in La Crosse, Wis., serving a 19-county region with annual revenues topping $600 million. He offered a sharp critique of the forces that shape much of the capital investments in health care today.

"I think the battle over who's got the bigger, shinier sword is a problem," Thompson said. To be sure, that shiny sword is nowhere to be found in Thompson's office—a cubicle, really, on the third floor of the hospital located south of downtown La Crosse, and no more glamorous than that of a modestly successful middle manager.

During Thompson's six-year tenure so far, the annual rate of fee increases has declined every year, moving from 9 percent to about 5 percent. But continuing that streak is tough for a number of reasons. One of them is the reimbursement model, which encourages the addition of high-margin specialty services.

In larger markets with more than one provider, duplication can occur as competitors build up the range of services that can be offered within a health care system. About a decade ago, Gundersen and its regional competitor, Franciscan Skemp, tried to forge a partnership that would have tied all of their hospitals and clinics into a single health care unit. The move, taking advantage of each organization's strengths, could have wrung $100 million to $150 million out of the region's health care spending, Thompson said. But the deal ultimately fell apart when Franciscan Skemp joined forces with the Mayo Clinic of Rochester, Minn.

So now the La Crosse region is "imbalanced," in Thompson's view, in terms of the medical capacity necessary to serve the region. For example, both Gundersen and Franciscan have neonatal intensive care units. But facilities are just the tip of the cost iceberg, according to Thompson, who is himself a neonatologist. Once in place, the dual facilities have to be equipped, which means there are two of everything, including "a set of ventilators that mostly sit in the closet." Even more important, "these things have to be staffed," he said, and "the people costs are huge" because of the specialized training required for nurses and physicians.

"It isn't that expensive to build a building," Thompson said. "People focus on the shiny new building. But it's the technology and the people—that's what costs money." For example, the lifespan of technology investments is about one-fifth that of any facility, he pointed out. These and other capital needs "will be relentless even when you're done building."

Though policymakers and others fret over a medical arms race, the focus appears misplaced. Health care providers have little choice but to follow the money. Many in the industry acknowledge that health care dollars could be used to greater effect if spent differently. "I don't think we need a ton more money. I think there's enough there" to maintain a good health care system, said Thompson.

But as the saying goes, you get what you pay for: In this case, reimbursement policies have been a central architect of any medical arms race taking place today, encouraging investment in new, intensive and expensive kinds of treatment.

"You don't see people opening big behavioral centers" that treat for chemical addiction or mental illness, despite their prevalence and cost to society, Thompson said. That's because reimbursements for such treatments are low, and hospitals can lose money on each patient. Instead, units specializing in services such as kidney dialysis or cancer treatment get the lion's share of new spending "because that's what gets reimbursed well above cost."

Ron Wirtz is a Minneapolis Fed regional outreach director. Ron tracks current business conditions, with a focus on employment and wages, construction, real estate, consumer spending, and tourism. In this role, he networks with businesses in the Bank’s six-state region and gives frequent speeches on economic conditions. Follow him on Twitter @RonWirtz.