Authors

Jay Hendrickson

Investing in ethanol and related products has seemed like a risk-free proposition, prompting much expansion and widespread media attention. Developers had about 75 ethanol plants under construction as of this past February. This growth would more than double production capacity and increase the number of plants by nearly 70 percent.

Investing in ethanol and related products has seemed like a risk-free proposition, prompting much expansion and widespread media attention. Developers had about 75 ethanol plants under construction as of this past February. This growth would more than double production capacity and increase the number of plants by nearly 70 percent.

But some agricultural economists warn of a boom mentality in the ethanol industry. Oil prices could fall, or the corn used to make ethanol could increase in price. Either development, depending on the extent of the change, could significantly reduce the returns to ethanol producers.

Given the high profile of ethanol's growth and speculation about its future, it is natural to ask bank supervisors about banking exposure to this industry. This question does not imply that banks should avoid ethanol-related lending. Bank regulators understand that banks provide valuable services by taking on risk; loans related to ethanol, even higher-risk ones, do not mean that banks have excessively risky portfolios of loans.

But banks could end up with excessively concentrated exposure to ethanol because they can lend money to plant developers, to locals who invest in the plants and to the many types of agricultural producers (for example, corn and livestock) who now find their future linked, at least partly, to ethanol production. Unlike most other parties financing ethanol plants, including local farmers, private investors and even stock-market investors, banks receive special government protections, such as deposit insurance, that can shift losses from such concentration to the public.

Observations of and direct conversations with the banks supervised by the Federal Reserve Bank of Minneapolis suggest that they do not have concentrated exposure to ethanol production. These banks also do not seem to have significantly increased their indirect exposure to ethanol through loans to agricultural producers.

But these observations have important caveats. In particular, supervisors face challenges in systematically measuring ethanol exposure, which can change quickly over time.

Direct exposure to ethanol

A look at banks supervised by the Federal Reserve Bank of Minneapolis offers only a partial picture of bank exposure, because many banks are supervised by other regulators. The Office of the Comptroller of the Currency (part of the U.S. Treasury Department) examines banks with a national charter. Banks that choose a state-granted charter receive supervision from a state supervisor and either the Federal Reserve or the Federal Deposit Insurance Corp.

Based on information gathered during examinations and ongoing dialogue with state member banks, it appears that banks supervised by the Federal Reserve Bank of Minneapolis do not have large direct risk exposure to ethanol producers. That is, these banks generally do not have a material amount of credit outstanding to ethanol producers. Producers that have bank loans also appear to make payments in a timely fashion. That experience seems to be generally shared by state supervisors as well, based on conversations with several from district states.

However, banking supervisors conduct their most intensive reviews of banks once a year, or even less frequently for banks in stronger condition, and typically do not otherwise receive notice of underperforming loans. As a result, the current analysis reflects only information about a subset of institutions the Federal Reserve Bank of Minneapolis supervises.

Another fairly direct source of ethanol exposure for banks arises from loans to firms or individuals, particularly farmers, who then use the money to invest in an ethanol plant. Nationwide, farmers owned nearly 40 percent of the ethanol production capacity as of January 2007. Such loans have appeared in reviews of state banks' credit operations, but available evidence suggests that banks supervised by the Federal Reserve Bank of Minneapolis have prudently assessed borrowers' overall financial strength, rather than the stock value of the ethanol plant, in making the loans. More generally, data from the Renewable Fuels Association indicate that farmers own a historically small share, around 10 percent, of the ethanol plant capacity under construction.

Indirect exposure: Grain production

At first blush, the ethanol boom should offer nothing but gain for corn producers and those lending funds to corn producers. Corn utilization by ethanol producers increased nearly 100 percent between the first quarter of 2002 and the fourth quarter of 2005; the U.S. Department of Agriculture expects another utilization increase of 45 percent during 2007. Increased use of corn for ethanol has pushed corn reserves to 11-year lows following a lower-than-expected 2006 harvest of 10.53 billion bushels.

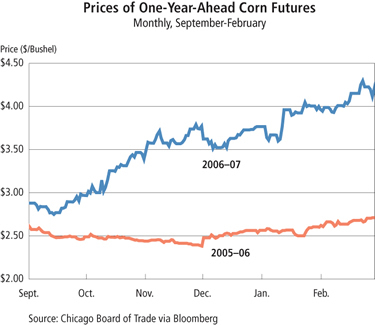

Elevated demand has pushed the price of corn in the current period to a 10-year high. With healthy growth in ethanol production capacity anticipated, the prices of corn futures (hedging contracts that lock in a price for corn delivered in the future) for delivery roughly one year out were running 50 percent to 60 percent higher at the beginning of 2006 than they were in the same period a year earlier (see chart).

But there is a potential downside to banks having excessive concentrations of loans to corn producers: Should ethanol become less profitable in the future, demand for corn could also fall, and if it did, corn prices would likely follow. If farmers make investments to increase corn production (for example, buy more land or equipment), they may find themselves with less cash than anticipated if prices fall or are not as high as expected. Less cash for the expansion-minded producer means an increased chance of not repaying the bank.

Of course, farmers can profit from the boom in corn prices without much additional financing. For example, they are reportedly shifting acreage from wheat, soybeans and other crops to corn production. Although ethanol has been discussed only with a subset of banks and examiners, there doesn't appear to be much new lending that puts the borrower at the mercy of ethanol. Some banks have reported receiving fairly speculative financing proposals, but they are rare and supposedly end up receiving support from nonbanks, according to Federal Reserve Bank of Minneapolis examiners.

In addition to exam-based evidence, the Federal Reserve Bank of Minneapolis also monitors short-term changes in land prices as a possible indicator of increased demand for land—and possibly increased banking exposure—in ethanol-producing areas. Such monitoring by its nature faces challenges because other factors—hunting, recreation, housing and commercial development—influence land pricing beyond ethanol production and corn prices. So-called 1031 exchanges (where a land seller avoids capital gains taxes if the money is used to buy similar property for commercial purposes) and continued low interest rates may also explain higher prices in some areas. (For more discussion of farmland prices in the district, see the September fedgazette.)

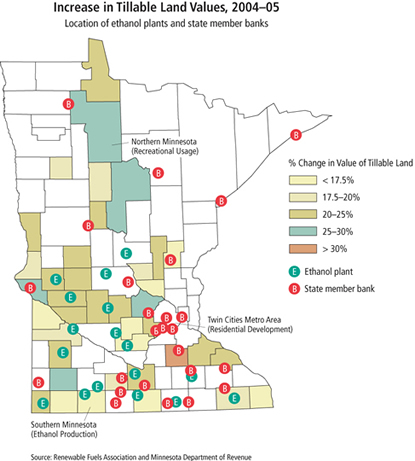

A look at a geographic connection between ethanol refinery locations and banks supervised by the Federal Reserve Bank of Minneapolis provides additional information for bank supervisors. In Minnesota, for example, there appears to be some relationship between land values and ethanol production. But it's hard to tease out ethanol's exact influence. Indeed, for the highest land value increases, proximity to the Twin Cities and recreational demand seem to be, at least superficially, drivers of the increase (see map).

Indirect exposure: Livestock production

Livestock producers rely heavily on corn as an input, which means that ethanol's influence on corn prices could affect the ability of livestock producers to repay their bank loans. Consider cattle ranchers. As corn prices rise, so do feed costs, which cut into margins on every animal. Some feedlot operators near ethanol plants can mitigate the increase in corn prices somewhat by using a portion of the corn byproduct from the ethanol production process. But all else being equal, the feedlot owner facing higher corn prices will want to pay less for feeder cattle. Consistent with that story, average prices for feeder cattle fell 23 percent from January 2006 to January 2007 at public auction yards in Montana. Similar arguments apply to dairy farmers whose cows typically feed on nothing but corn. Agriculture Department data show that monthly feed costs for milk production in Wisconsin rose 35 percent in January from a year earlier.

Supervisors thus need to consider bank exposure to cattle production when considering ethanol-related risks. And some state member banks are located in cattle country. Although significant problems have not yet arisen, Federal Reserve Bank of Minneapolis examiners have found that some state member banks are concerned about the effect of rising prices on rancher-borrowers, some of whom may have significant susceptibility to external pressures, such as rising feed prices.

Hog producers also use corn as an input. But banks supervised by the Minneapolis Fed have less direct exposure to hog production than to cattle production. This outcome reflects a number of factors, but one particularly important development concerns the vertical integration of the hog industry. With such integration, those raising hogs look to large processors—who own hogs throughout the production cycle and provide the key inputs—to help finance their operations. The hog-producing bank customers may engage in that activity under a contract with a large processor that could help protect them from changes in market prices (at least in the short run). Similar developments have also altered the nature of poultry production.

Worrywarts

Only paid worriers could look at the current ethanol boom and express concern. Bank supervisors plead guilty. (For a more complete list of risks associated with ethanol, see Issue 1 of the Kansas City Federal Reserve Bank's 2007 Main Street Economist.) Bank supervisors have a responsibility to assess if bank risk-taking—the raison d'être for banks in the first place—has become too concentrated and excessive because of the unique government guarantees that these financial institutions receive. For the moment, at least, banks supervised by the Federal Reserve Bank of Minneapolis do not appear to have large exposure to a rapidly growing ethanol market, or its offshoot effects. But continued vigilance is needed, given the difficulty in measuring ethanol-related exposures and the speed with which they could change.

Even developments that could take many years to play out can pose some risk. Consider the potential for cellulosic-based ethanol, which uses a wide array of biomass, such as agricultural waste and native prairie grasses, as inputs. Such a shift could undermine the viability of current corn-based ethanol producers and those lending to them, and pull the plug on a considerable amount of demand for corn. Something else for Ninth District bank supervisors to worry about.

Jay Hendrickson is an examiner and Mark Lueck an economist in the Supervision, Regulation and Credit department of the Federal Reserve Bank of Minneapolis. Ron Feldman, vice president; Mark Rauzi, assistant vice president; and Steve Wyard, field supervisory examiner, made significant contributions to this article.