Author

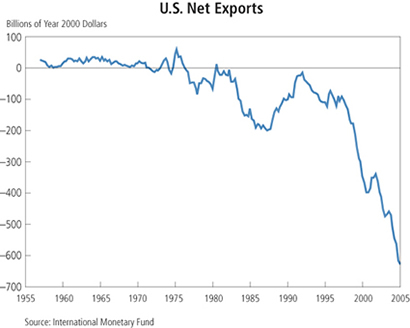

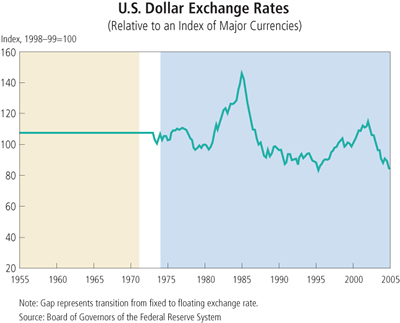

With the U.S. trade deficit large and growing larger, and the dollar losing value relative to other world currencies, it's natural to ask if the two trends are related. It's also worth asking if the trends will continue into the future, or if we should even be worried about them.

These questions have been prominent in media and political debates across the country, and they were the focus of this year's Minneapolis Fed board of directors' retreat, held in mid-August.

The broad media reaction to these trends has been akin to horror, and the halls of Congress have begun to ring with echoes of mercantilism—the discredited 18th century economic doctrine favoring home industries and exports over imports. But at the directors' retreat, economists reviewed theory and practice to share a deeper perspective on the realities of international trade and exchange rates—demonstrating that mercantilism still rings hollow.

Trade and the dollar

"The subject seemed like a natural one last year when we planned this retreat," observed Minneapolis Fed President Gary Stern, in his opening remarks, "and interest in it has been steadily increasing since."

Indeed, media coverage of trade deficits and the weakening dollar has reached saturation levels, and China has often been portrayed as the prime culprit for both because of its policy of pegging the yuan to the dollar. The currency peg, goes the argument, makes Chinese goods artificially cheap and hampers the tendency of the sliding dollar to decrease U.S. imports of Chinese products. Facing international pressure and fearing trade restrictions, the Chinese have made small moves toward a more flexible rate policy in recent months. Even Fed Chairman Alan Greenspan, speaking before Congress, had kind words to say about the change in the yuan peg.

The media story seems to jibe with conventional economics. If Americans are purchasing more foreign goods, thus sending more dollars overseas, the greater supply should decrease the dollar's value relative to other currencies. Less international confidence in the dollar's stability could lead nations to sell off their reserves, exacerbating the dollar's decline. Eventually, foreign goods would become more expensive for Americans and, depending on your perspective, either the trade balance would become more equal or all hell would break loose.

The dismal dollar

But is this picture the correct one? Addressing that question was the subject of the first day's sessions. Directors heard first from Research Officer Warren Weber. While there is nothing intrinsically wrong with the conventional picture, he said, the dollar's value doesn't necessarily fall as the trade deficit grows. "When you think about international trade," said Weber, "think about borrowing and lending. ... Really, it's based on an intertemporal allocation decision, and not so much about which country's goods are cheaper." The key point is that to finance a trade deficit, a nation must borrow from foreign lenders.

Weber began by presenting trade data indicating that indeed the U.S. trade deficit has been rapidly increasing in recent years. But, he argued, this should not alarm us, because trade deficits are not inherently bad. For one thing, economic indicators like gross domestic product (GDP) and employment don't vary much with the trade balance. Both have continued to grow as deficits have gotten larger. "As a matter of fact, if you catch me after a beer or two," he joked, "I might make the argument that maybe we shouldn't be collecting trade data whatsoever, because people tend to think deficits are bad and surpluses are good, and collecting data may cause them to draw erroneous conclusions."

Then Weber returned to the question of whether the dollar must fall because of the trade deficit. His answer: Maybe not. While the trade imbalance can't continue indefinitely, the dollar's decline isn't the only way to eliminate the deficit. Weber suggested two other possibilities.

One is an increase in interest rates. Foreigners will eventually require higher rates before they'll lend more money or roll over existing debt. Higher interest payments by American consumers will mean lower consumption, leading to reduced imports. This could all happen without a slide in the dollar's value. But, Weber noted, "I'm not arguing that these are mutually exclusive."

The other possibility requires no adjustment in interest or exchange rates. Foreign incomes will rise simply because of higher debt payments and greater foreign holdings of American assets. As incomes rise, foreigners will demand more American exports. Also, greater American consumption now means decreased consumption in the future, other things equal—imports can't climb forever.

In sum, Weber observed, while dollar depreciation is one possible consequence of the trade deficit, it need not be the only adjustment mechanism, or even the most important one.

Let's fix it

Directors then heard from the Minneapolis Fed's Vice President and Director of Research Art Rolnick on "The Dollar, the Yuan, and Trade Balances." The talk began with a summary of Rolnick and Weber's work on exchange rate policies. (For more detail, see Arthur J. Rolnick and Warren E. Weber, "The Case for Fixing Exchange Rates," The Region, 1989 Annual Report.) The conventional view, said Rolnick, is that money is a good like any other and that its value should be determined by the market. Since Milton Friedman's influential 1953 essay, "The Case for Flexible Exchange Rates," economists have generally held that floating rates bring international trade into balance. But Rolnick argued that this view is flawed.

The evidence clearly shows that trade balances have become less stable since the world moved toward a floating rate policy in the 1970s, said Rolnick. Exchange rates have been volatile, and this has imposed significant costs on international trade. While the conventional view can't explain this, it is easily understood from an alternative perspective: "Fiat money" is fundamentally different from other commodities.

Economists refer to currencies like the dollar and yuan as "fiat money" because it is by government fiat alone that they acquire value. "These are useless pieces of paper that cost almost nothing to produce, so there is a virtually unlimited supply. That's special," said Rolnick. "Why do people demand fiat money? They don't demand it because it's something useful that has value like gold or silver or tea or tobacco." The demand is a result of political factors and social influences, not regular market forces. "That means markets aren't going to work the way we expect them to," he said.

As evidence, Rolnick pointed to research on the predictability of exchange rates. The data suggest that exchange rates follow a random walk, meaning the day-to-day fluctuations are random and unpredictable, so there is no better predictor of the future value of a currency than its present value. Unlike other goods, fundamentals don't do a good job of explaining the value of money.

"From our perspective, this makes sense. The price of money can and should be set by the government," said Rolnick. The most successful example of such a policy is the Federal Reserve System itself. Each of the Fed banks issues its own currency, but those currencies trade at a fixed rate of one-to-one within the United States. That has made it possible to conduct transactions throughout the country without the risk that a combination of floating currencies would impose. Similar arrangements exist in Germany, since reunification, and in the European Monetary Union. Both are examples of successful fixed exchange rate policies.

While such policies clearly can work, the challenge they face is not economic but political. Nations must be convinced to give up monetary sovereignty, and sometimes redistributive decisions must be made. Within the European Union, for instance, the United Kingdom refuses to give up authority over its pound, and wealthy nations griped when some poorer Eastern European states were admitted to the Union. In a 1992 interview with The Region, Milton Friedman, asked whether a European monetary union would be a good idea, replied that it was a fine idea, but it would never happen.

Rolnick then moved to the issue of the Chinese currency peg. Not only is such a peg not harmful to trade, he argued, it is actually a good policy that can reduce the cost of currency volatility. Given the level of trade between the United States and China, such a cost could be quite high, and reducing it could promote trade. Contrary to the popular belief that the yuan's value would rise if the peg were removed, Rolnick said, the evidence indicates that there is actually no way to predict whether an unpegged yuan would rise or decline relative to the dollar or other currencies. A peg makes sense, Rolnick concluded, and it doesn't even matter exactly where it's set, so long as it's credible.

At that point, Rolnick was challenged by Nobel laureate Ed Prescott, senior monetary adviser to the Minneapolis Fed. Prescott questioned whether, indeed, such a peg could be credible. His was no minor quibble, since Prescott pioneered the analysis of credibility in economic policies. Such a policy must be carried out by government buying up and selling currency, and "there's only so much debt to go around," Prescott said. Rolnick quipped that this was evidence that the economics profession is not near a consensus on the issue.

Barriers to riches

That interaction led into Prescott's much anticipated presentation, "Barriers to Riches." While not directly related to the retreat's main theme, Prescott's talk focused heavily on open trade as an important factor in determining the wealth of nations.

Prescott's theory is that modern economic growth results from increased productivity due to technological advances. Poor nations can achieve growth by opening their doors to technologies developed in rich nations. However, entrenched interests, such as monopolies, often block technologies that would compete with their business and thus create barriers to growth in poor nations. Open trade is therefore essential to economic development. (For more, see Preston J. Miller and James A. Schmitz Jr., "Breaking Down the Barriers to Technological Progress," The Region, 1996 Annual Report Essay, or Prescott's 2000 book, Barriers to Riches, with co-author Stephen Parente.)

Prescott also gave some impressions from his travels around the world since winning the Nobel in October 2004. Chinese Prime Minister Wen Jiabao "seemed sharp," said Prescott, "but has a tough political situation." Wen told Prescott that China was committed to staying open and would not repeat the mistake of the Ming Dynasty by closing off and stagnating. Prescott said he told Wen that China should not subsidize much U.S. debt, "but as an American," he joked, "I didn't mind being subsidized."

The Chinese theme continued that night at dinner. Mike Meyers, national economics correspondent for the Minneapolis StarTribune, gave a talk titled "A Reporter's Observations on China." He recounted his experiences in his three months of traveling in the country last year. The overarching theme of his talk was that Americans need not fear the Chinese economy. The nation is still plagued with inefficiency, so it is not quite the juggernaut it is made out to be.

Two case studies

The next day was dedicated to case studies. Ricardo Lagos, assistant professor of economics at New York University and a research economist at the Minneapolis Fed, presented some recent history from his native Argentina. Once the policy reform poster boy of the International Monetary Fund, Argentina has been in steep economic decline since the late 1990s, said Lagos. After a period of recovery from years of stagnation, real GDP per capita has dropped 19 percent since 1998. "This is a catastrophe," Lagos told the audience.

Argentina's woes are especially relevant to the conference's theme, since Argentina operated on a fixed exchange rate policy with the U.S. dollar until December 2001, when it defaulted on its debt. The policy was initially successful in stabilizing the Argentine economy which, until the 1990s, had been wracked by hyperinflation. Lagos recalled going into a bookstore during that inflationary era and asking the price of a textbook. The clerk told him the price, but said it would be higher once Lagos returned with the cash to buy it.

The fixed exchange rate policy took care of hyperinflation, but ultimately failed due to a combination of bad policies and unfortunate circumstances, thereby providing a lesson on how not to fix rates. Lagos argued that the exchange rate set by Argentina was too high relative to the currencies of some of its nearby trading partners. Rolnick, of course, had earlier argued that the rate didn't matter as long as it was credible. Lagos suggested that, indeed, the policy lost its credibility when the public lost its faith in the currency board.

However, Lagos continued, there were deeper reasons for Argentina's woes. While some observers contend that fiscal discipline reforms weren't sufficiently implemented, Lagos said that was only part of the problem and that some of the data were misleading. He suggested that the collapse was due to a "destructive cocktail" of external shocks like the Mexican, Russian and Brazilian currency devaluations, along with weak fundamentals, such as the government's history of violating property rights in tough financial times.

Ultimately, Lagos said, many questions remain unanswered, and the story of Argentina's economy continues to unfold. University of Minnesota Professor of Economics Tim Kehoe added that it usually takes a nation 10 to 15 years to regain its credit standing after defaulting on debt, so we don't yet know what the future holds for Argentina.

With that comment Kehoe, a Minneapolis Fed research consultant, began his presentation on the European Union. "Art just told you that I'm going to tell you where the European Union is going, and that's not quite true because I don't know where it is going," he said. He did, however, discuss some of the difficulties and uncertainties that Europe now faces.

Kehoe said there is widespread belief among Europeans that the EU is not growing as fast as the United States because the European Central Bank is too focused on controlling inflation. But Kehoe argued that Europe's relative stagnation is due to labor policies, not central bank problems. It is well known, for instance, that Europeans work less and vacation more than Americans; the question is why. Some attribute the difference to cultural factors: Europeans prefer leisure more than Americans do. Others, like Prescott, argue that the explanation is differences in tax policy. (See Douglas Clement, "European Vacation," The Region, December 2003.)

Kehoe attributes some of the difference to governments operating on the "lump of labor fallacy," the idea that there could be too many workers in the market and not enough jobs. This belief led governments to encourage older workers to retire early so the young could have their jobs.

Labor law reform has been controversial in Germany and elsewhere in Europe, and Kehoe said one reason many nations have rejected the EU constitution is a sentiment among Europeans of not wanting to be "like the Americans." The constitution, they fear, would mean having to give up labor practices that they largely favor. Kehoe closed by assuring the audience that while the EU is troubled, the European monetary union is firmly in place and remains a testament to the value of fixing exchange rates.

Stern lecture

Minneapolis Fed President Gary Stern then provided concluding remarks, starting with a synopsis of the retreat. The first day's presentations provided a broad framework for thinking about trade, he said. "That the dollar might fall [in reaction to a trade deficit] is just one of a number of possible adjustment mechanisms," he said, summarizing the day's lessons, "although the press treats it as a fait accompli."

The second day of presentations had covered the application of these principles, said Stern. Lagos had shown that institutions matter. "Erratic policies, including the lack of central bank independence," Stern summarized, "can stifle growth." Kehoe had shown that anxiety about the EU is not really connected to growth, but to other concerns. Commented Stern, "People don't observe growth."

Stern then provided broader comments on the Fed and such issues. "There is a lot of concern, some of it misplaced in my view, on the current account and the exchange rate," he said, reiterating earlier themes. "More consumption now may just mean less in the future." In addition, said Stern, most Fed policymakers are coming to accept that exchange rates are not predictable.

Stern also shed some light on Greenspan's public comments on China's recent exchange rate move. "One of Greenspan's greatest concerns is a renewal of support for protectionism and trade-limiting policies, especially if that were to lead to retaliation or imitation by other countries." Allowing exchange rates to float a little might not be such a bad idea, Stern concluded, if such a move keeps politicians from reverting to protectionism.

Joe Mahon is a Minneapolis Fed regional outreach director. Joe’s primary responsibilities involve tracking several sectors of the Ninth District economy, including agriculture, manufacturing, energy, and mining.