Author

That time of year again. Yep. Farmers across the district are getting ready to do what farmers do. They'll plan for and worry over innumerable scenarios for getting crops planted and nurtured until harvest, making sure machines are well-tuned, seed is high quality and their knees are pain free, because it won't be long before the praying starts.

Farmers in much of the district are facing persistent drought and droughtlike conditions going into the growing season, as well as a host of other threats like pests, disease, floods and frost that can jeopardize crop yields. In that vein, maybe no other item on the checklist is as critical to a farmer's financial interests as crop insurance.

And while direct crop subsidies to farmers have gotten the lion's share of media and policy attention over the last decade, a slow but important transformation has taken place in crop insurance. The good news is that farmers nationwide and in the district are insuring more acres, seeking higher levels of protection and getting better payouts when disaster strikes—as it inevitably does.

The bad news is that regardless of significant federal subsidies that buy down the cost of crop insurance for farmers—at a cost of billions to U.S. taxpayers—crop insurance in its current form is still not sophisticated enough to keep farmers off a slippery financial slope when natural disaster, in its many forms, hits. Nor has crop insurance managed to eliminate federal disaster aid to farmers despite being intended to achieve that seemingly attainable goal.

Policy drought?

With the worry of drought and numerous other perils, one would think district farmers are beating down the doors of local insurance agents. But you won't find strong trends one way or the other when looking at the number of active policies.

Heading into the 2004 crop season, drought has been the "primary motivator" for Montana farmers to purchase crop insurance, according to Doug Hagel, director of the regional Risk Management Agency office in Billings, Mont. The RMA is an arm of the U.S. Department of Agriculture (USDA) and runs the federal crop insurance program.

But if there is a larger trend in crop insurance policies, it's slightly downward. Nationwide, the number of active policies peaked—at least so far—in 2001. The number of policies in Montana has been on a slow increase since 1998, but dropped slightly in 2003. In Minnesota, where almost three of four counties were declared drought disaster areas in November, the number of crop insurance policies in that state is well down since 1998. Policies for the Dakotas and Wisconsin are also down marginally.

While that trend might seem counterintuitive, there are a number of factors that help explain the phenomenon. First, Hagel pointed out, the number of farms continues to fall every year, which reduces the number of needed policies as acreage gets consolidated into fewer farms.

Probably more prevalent, crop insurance has also hit its saturation point in many regions. Farmers today are taking out insurance policies as a matter of good business practice, much like the average person carries car insurance. "We've gotten to the level where we're pretty stable" in terms of policies, Hagel said.

Craig Rice is the director of the regional RMA office in St. Paul that covers Minnesota, Wisconsin and Iowa. "In my three states, everyone who's going to buy it has it," he said. Rice estimated that upward of 90 percent of corn and soybean farmers in Minnesota and Iowa have crop insurance.

The insurance rate among Wisconsin farmers is much lower than the district's average—Rice estimated between 50 percent and 60 percent but said there was some logic behind that trend as well. Wisconsin's major ag industry is dairy, and most dairy farmers grow corn and soybeans to diversify. But if their corn shrivels up because of drought, Rice said, "they'd just cut it and harvest it for silage" for their cows and still get value out of it. Rice also noted that Wisconsin dairy farmers "have not traditionally been helped by government programs," which seems to make them more independent to begin with.

Other sticks measure up

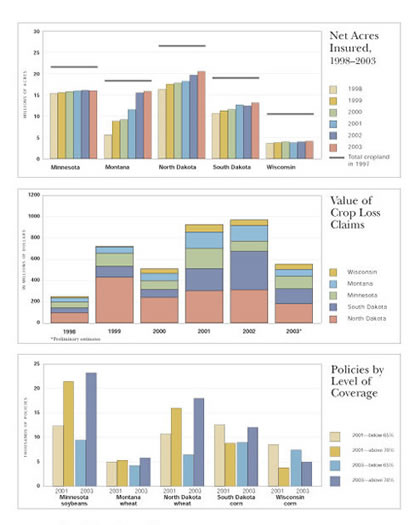

Two other measures—net acres insured and so-called coverage levels—suggest that farmers are indeed embracing crop insurance more tightly than in years past. The number of insured acres went up in every district state from 1998 to 2003, including 18 percent in North Dakota and 22 percent in both Wisconsin and South Dakota, bringing more than 6 million more acres under the insurance umbrella in just those three states (see chart).

Source: Risk Management Agency, U.S. Department of Agriculture

Montana is in a category all by itself. Covered acres rose by 260 percent from 1998 to 2003, adding 10 million acres, according to RMA data. Two factors are involved: the introduction of new policies to insure rangeland—which makes up a significant chunk of farm acreage in Montana—coupled with the drought, which convinced farmers to hedge against poor livestock forage.

District farmers are also increasing their coverage level. (Coverage level is the point at which yield losses trigger insurance claims. For example, if a farmer takes out a policy at a coverage rate of 65 percent, he must incur a yield loss of 35 percent before insurance kicks in.) According to testimony last June by RMA Administrator Ross Davidson Jr., only one acre in 10 had coverage of 70 percent or more of yield in 1998. By 2002, half of all acres had such coverage.

In the district, from 2001 to 2003, virtually all major commodity groups (analyzed by state) showed a decrease in the number of policies with coverage levels under 70 percent, while those same crop groups saw universal increases—often big ones—in policies with coverage over 70 percent (see chart on adjacent page). The increase in acreage and coverage levels pushed up total insured crop liabilities in the district by 17 percent from 2001 to 2003.

That has meant more cash in the pockets of strapped farmers when they see crops wither on the proverbial vine. From 2001 through (preliminary final data for) 2003, annual crop insurance claims by district farmers have averaged about $825 million, led by North Dakota, which has averaged about $275 million annually in indemnities over this period, according to data provided by the RMA.

Nickel slot, pays dimes

Indeed, if farmers simply are patient and diligent about buying insurance, Congress has intentionally structured the program in such a way that buying insurance is profitable for farmers.

How? Unlike most insurance products, crop insurance would likely not exist at or near the current levels were it not for federal crop insurance programs, the first of which was created in the 1930s, according to the RMA. Numerous changes were made to programs over time, mostly to expand the number of covered commodities (now at about 100) and to encourage farmers to protect themselves against crop loss.

Congress first started subsidizing the purchase of crop insurance in 1980, paying for 30 percent of a policy's cost at coverage levels up to 65 percent. Unhappy about participation levels and repeated natural disasters in the late 1980s and early 1990s that required emergency farm aid, Congress passed broader and more generous provisions in 1994. While the number of covered acres expanded dramatically, Congress tinkered yet again, with the Agricultural Risk Protection Act of 2000 (ARPA), which Hagel called "the foremost act as far as crop insurance."

Among numerous objectives—including protecting against fraud and educating farmers about other risk-management tools—ARPA dramatically increased the average subsidy for crop insurance policies, which is paid by the Federal Crop Insurance Corp. For a policy with 50 percent coverage, ARPA authorized the FCIC to subsidize 67 percent of the premium's cost; at 65 percent, the FCIC assumes 59 percent of the premium. For the first time, ARPA created subsidies for policies with coverage levels of 75 percent (with a 55 percent subsidy) and 85 percent (38 percent subsidy).

Rice and Hagel both said that they are required to set policy rates at a level that achieves a loss ratio of 1.07 over time. (Loss ratio is the percentage of total indemnities divided by total premiums, including government subsidies.) In other words, for every dollar paid toward a crop insurance policy—including the federal subsidy averaging about 60 percent of the premium—the RMA expects to pay out $1.07.

"Rates are already set so you're going to make money over time," Rice said. "Farmers say it's pretty expensive, but it's really pretty cheap." The 1.07 loss ratio also does not include the overhead of 18 private insurance companies that do the marketing and selling of the actual insurance policies for the RMA—a cost to the RMA that Rice estimated at about 23 percent.

Just how good a deal is this for farmers? From 2001 through 2003, district farmers paid a total premium of $931 million for all crop policies, according to data provided by the RMA. Meanwhile, the federal government subsidized those policies to the tune of $1.3 billion. In turn, district farmers laid claim to $2.5 billion in indemnities. In other words, during this three-year period, crop insurance netted district farmers an additional $520 million in cash annually over and above their out-of-pocket costs for the insurance. Indeed, drought and other weather events have made the district something of a hot spot for claims (see map).

On the individual farm level, the return on any insurance investments will depend on weather and many other factors. Good weather and good harvests make insurance look like an unnecessary expense. Even when growing conditions are bad, the return on insurance policies varies widely and depends on coverage levels, acreage, crop and severity of loss.

But on the whole, most reports at the farm level support the notion that insurance more than pays for itself over time. Farm Business Management is an educational program for farmers run by Minnesota State Colleges and Universities. It publishes summary financial reports on about 2,300 farms that participate annually in the program. From 1998 to 2002, in all but one year (2000) the average FBM farmer received more in insurance payments than was paid in premiums.

FBM farms with the highest net income were also those that spent the most on insurance and received the greatest return on that insurance investment. In the five years analyzed, the top 20 percent of FBM farms (in net income) never earned less than a 27 percent annual net return on their cost of insurance and had a five-year average net return of better than 40 percent.

In terms of actual cost, crop insurance can appear reasonable, if not downright cheap after factoring in federal subsidies. RMA officials estimated that a farmer's out-of-pocket costs for crop insurance typically run about 4 percent of total expenses. A 2003 crop budget report by Bob Anderson, a University of Minnesota Extension educator, estimated that crop insurance costs per acre for state corn farmers equaled about 3 percent of total expenses (which did not include rental or other land costs) and only about 2 percent of total expected income.

Slippery slope

Most farmers, however, are working with small operating margins, and therein lies a significant problem with current insurance programs.

Hagel said many commodity farmers have profit margins of 5 percent to 7 percent. "That's pretty slim," he said. Insurance costs, while seemingly affordable at face value, nonetheless cut deeply into a farmer's potential profit margin. This is particularly the case if a farmer chooses high coverage levels, which are proportionally more expensive because related liabilities and potential indemnities are also higher. And in the end, that insurance might still not protect him very well in the event of a disaster. If a farmer carries a policy with 75 percent coverage—which is higher than average—he'll end up taking a loss of 18 percent to 20 percent despite being paid a claim, Hagel said. "He's put himself back three or four years."

That slope gets even more slippery for farmers over time, because policies base claim payments on average yield over time, often a decade, which goes down when harvests are low enough for farmers to make an insurance claim.

In testimony last August to a U.S. House committee hearing on farm policy in Ada, Minn., Bruce Freitag, president of the North Dakota Grain Growers Association, told representatives that it takes 90 percent to 95 percent of an average crop to cover costs.

"Coverage levels that are higher than 75 percent are impractical to purchase unless you plan on having a disaster. ... With the most affordable and justifiable coverage levels of the current crop insurance program at the 65 percent to 70 percent level, a substantial shortfall occurs whenever there are crop problems. In other words, a farmer had better plan on having five or six good years before having a bad one in order to stay in business," Freitag said.

Those farmers that choose to forgo insurance or carry low coverage levels do so because "the deductible bugs them. ... They say it doesn't pay off," Rice said. At 65 percent coverage, "they lose a third of their crop and insurance doesn't pay them anything."

But that's also missing the point, Rice said. "You don't collect on your car insurance every year either."

Policy: disaster

Maybe a more serious indictment of the current crop insurance program is its failure to eliminate the economic or political need for emergency aid when disaster says hello—this despite generous incentives for farmers and high participation rates in terms of farmers and acreage. Early last year, for example, Congress passed an emergency aid package of $3.1 billion for farmers, about two-thirds of which went directly to farmers who experienced weather-related crop losses of more than 35 percent in 2001 and 2002.

Although significant insurance improvements were made under ARPA, farmers and policymakers continue to complain about coverage gaps that expose farmers to loss risks. In testimony to the House hearing in Ada, Randy McMillin, a canola farmer and chair of the Minnesota Canola Council, stated that "although the RMA must remain actuarially sound, one thing we must do is strive to make higher levels of crop insurance more affordable. This will not only help to preserve and strengthen the safety net on which producers rely, but it is critical to the economic health of our region in bad years as well."

Economists point out that the elimination of risk basically throws out the rule book for an efficient market economy and virtually guarantees excess production over time. Already, because insurance subsidies divert production risk away from farmers and onto the shoulders of the federal government, crop insurance likely encourages production on marginal land that otherwise probably would not be planted.

An RMA source said that existing programs serve some segments very well and others less so. Farmers in higher-value crops like potatoes, cranberries and other fruits and vegetables see fewer crop losses on average because such crops "are only grown in areas where they [historically] can be grown," the source said. Given that these operations also tend to have higher-than-average equity, farmers often insure against "the one-in-10-year hit." Other crops, particularly major commodities like wheat, corn and soybeans, are often grown on more marginal land and low rainfall areas "where the degree of risk is much higher."

But it looks like more of the same for much of the district in 2004. For example, the USDA projected Minnesota's 2003 crop loss at $1.1 billion, with 62 of the state's 87 counties were declared drought disaster areas. On the heels of that, district congressional representatives are again beating the budget bushes for disaster aid. In October, Minnesota Rep. Collin Peterson introduced the Permanent Emergency Agricultural Assistance Act, which seeks to help crop farmers suffering from crop losses in the last three years and offers a more generous payment formula. The proposal would also establish regular, programmatic disaster aid for farmers going forward, on the condition that only those farmers carrying crop insurance would be eligible.

At the Ada hearing and elsewhere, Congress has been looking for feedback from farmers and others in the industry on a better crop insurance model. Most often, suggestions from farmers and their member associations tend to focus on greater subsidies for higher coverage levels and more generous formulas for average yield (against which losses are tabulated). Such improvements would certainly benefit farmers, but at an additional cost almost wholly assumed by the federal government, and with no guarantee that such changes would eliminate emergency disaster aid.

Said the RMA source, who asked not to be named, "Congress works on an ad hoc basis trying to fill all these holes ... which helps on a short-term basis, but is really not effective from a long-term perspective."

| Ninth District agricultural lenders are optimistic after a strong fourth quarter according to the Fed's agricultural credit survey. See the survey results. |

Ron Wirtz is a Minneapolis Fed regional outreach director. Ron tracks current business conditions, with a focus on employment and wages, construction, real estate, consumer spending, and tourism. In this role, he networks with businesses in the Bank’s six-state region and gives frequent speeches on economic conditions. Follow him on Twitter @RonWirtz.