Author

A good illustration of the changes to district banking structure is its evolution at the county level.

The Minneapolis Fed analyzed banking trends in the 303 counties located in the Ninth District. These counties were grouped into three categories: metropolitan, fringe and rural. Metropolitan counties are those located in metropolitan statistical areas (MSAs). Fringe counties, as defined by the U.S. Department of Agriculture, physically adjoin one or more metropolitan counties and have at least 2 percent of the employed labor force commuting to the central metropolitan counties. Rural counties are those that are nonmetropolitan and nonfringe.

The metropolitan and fringe counties for the district include those in and near the 14 regions in the district defined as MSAs by 1990: Missoula, Great Falls, Billings, Rapid City, Bismarck, Sioux Falls, Grand Forks, Fargo-Moorhead, Minneapolis-St. Paul, St. Cloud, Duluth, Rochester, La Crosse and Eau Claire.

The county analysis revealed that banking trends have plowed through urban, fringe and rural counties with roughly proportional force. For example, rural counties have experienced only slightly more head office loss and slightly less branch formation during the last 14 years.

However, those gains and losses did not occur equally across all counties, or types of counties. Twenty counties experienced a decrease in the total number of bank service points within their borders from 1990-2003, 101 had no change, and 182 saw a gain of at least one service point. (Six of 303 district counties had neither a branch nor head office in 1990 or 2003 and were counted as "no change.") Counties that either lost offices or had no growth during this period were rural ones concentrated in the swath of territory running from eastern Montana to the western third of Minnesota—an area seeing mostly stagnant or negative population growth (see map).

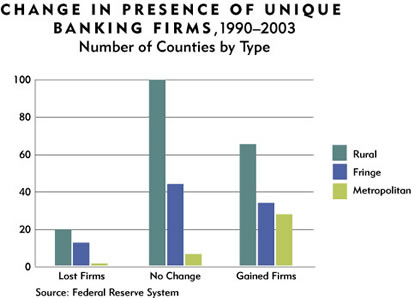

In terms of unique banking firms (which does not double-count firms affiliated with the same bank holding company), district counties show both similar and different characteristics. Metropolitan areas are getting noticeably more competitive-at least if competition is measured simply as the number of unique firms operating in them (and not adjusting for population or any other features).

But fewer than 40 percent of the rural and fringe counties had more firms operating in them in 2003 than they did in 1990, while 80 percent of the metropolitan counties witnessed such a trend (see chart). The majority of the counties that lost unique firms were not centered in the Dakotas or eastern Montana, but in Minnesota (18 of 32), where most were in the southern quarter near the Iowa border.

An analysis of bank saturation also uncovered 1,051 "places" in the district (cities and towns mostly, but also other jurisdictions recognized by the Bureau of the Census) with a single bank presence in 1990. Despite the widespread rise in bank offices in the district, 78 percent of these places saw no change in the local banking market by 2003, and roughly equal amounts saw a decline (9 percent) and growth (13 percent). Among the 97 places losing banking service, two-thirds (64) were in rural counties. For the 135 one-bank towns that gained service, the largest number (57) were also in rural areas, with the remainder split pretty evenly (40 and 38, respectively) among fringe and urban locations.

Related articles: |