On August 27, 2018, the Center for Indian Country Development at the Federal Reserve Bank of Minneapolis and the Federal Reserve Board of Governors held a first-of-its kind gathering that brought together over 100 Native American Financial Institutions (NAFIs). These are Native-owned or Native-serving banks, credit unions, and community development financial institutions.

We invite you to review the event agenda and materials below.

Event Details

August 27, 2018 at KwaTaqNuk Flathead Lake Resort. Polson, Montana

The goals of this convening:

- Foster networking, learning, and collaboration among Native community-serving financial institutions

- Create development opportunities to leverage capital

- Elevate best practices that create growth and sustainability

NAFIs in attendance—from Alaska to Maine—positively reported that the conference far surpassed their expectations. They are interested in learning more about new and emerging NAFIs, and especially look forward to future opportunities to work together.

![]()

Event Agenda and Materials

Networking Reception

In the evening of August 27, conference participants continued the day’s conversation on a boat tour of beautiful Flathead Lake on the KwaTaqNuk Lodge’s Shadow Cruiser. We are grateful to the reception sponsors: Confederated Salish and Kootenai Tribes, Bay Bank, Casey Family Programs, Citizen Pottawatomi Nation, and Pinnacle Bank.

Flathead Reservation Tour Agenda

On August 28, we toured the Flathead Reservation, including the tribally-owned Eagle Bank, which supports mortgage lending and homebuyer readiness across the reservation. We invite you to watch this video illustrating how the Tribes have established a successful infrastructure for homeownership on the Flathead Reservation.

Video of the Confederated Salish & Kootenai Housing Authority

Sovereign Lending: A Bright Chance of Survival

Resources for Native American Financial Institutions

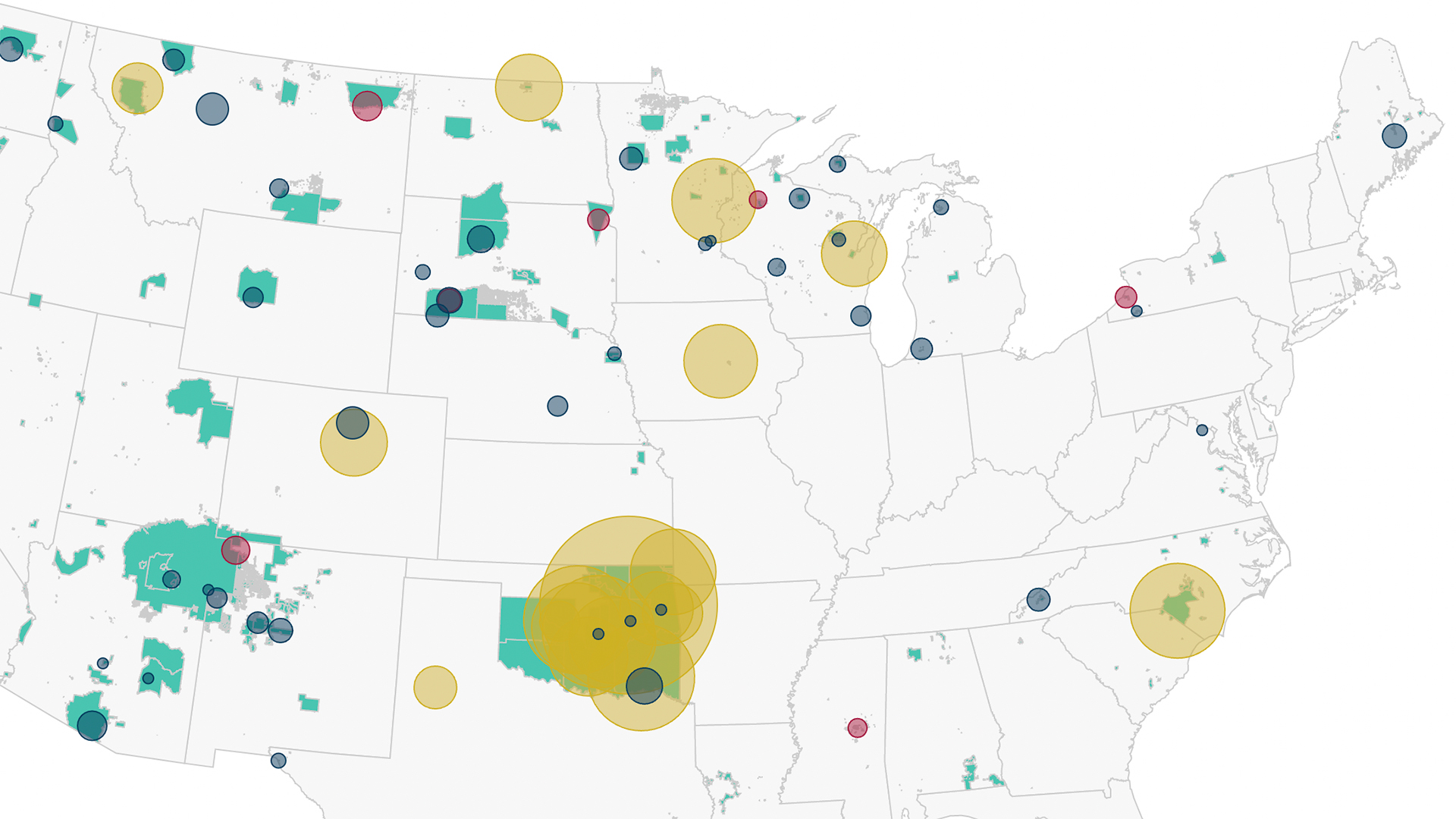

Mapping Native American Financial Institutions (NAFIs)

On August 27, the Center for Indian Country Development launched its dynamic map of the entire NAFI industry, with over 100 Native-serving financial institutions and $4 billion in assets.

The map features the potential for growth and expansion, with high-level information on assets and loans, as well as detailed profiles for individual banks and credit unions. For the big NAFI picture and to locate an institution, visit the mapping tool.

Reservation Profiles

Director Patrice Kunesh demonstrated on how financial institutions can access key community demographic and lending data at the Center’s Reservation Profiles. This data tool provides current information on economic indicators and lending activities for all reservations with residents of 2,500 or higher. These indicators include:

- Per capita income and employment stats

- Housing cost burden

- Homeownership rates

- Loan originations and denials

- List of active mortgage lenders

Access the Reservation Profiles here.

Tribal Leaders Handbook on Homeownership

While several NAFIs are engaged in mortgage lending in Indian Country, this remains a largely untapped and underserved market in most Native communities. There is growing interest in creating opportunities for homeownership through increasing demands for affordable housing and unique Indian Country-specific lending products.

To better support these efforts, the Center recently published the Tribal Leaders Handbook on Homeownership. The Handbook includes a loan products matrix, list of mortgage lenders active in Indian Country, as well as a landscape of the lending process. We’ve also highlighted four Native CDFIs in the Handbook with examples of their successful mortgage products and homeownership services. Check out these Native-serving lenders here.

An Industry Profile of Native American Banks, contributed by Betty Rudolph, FDIC (August 27, 2018)

There are 18 FDIC-insured Native American banks, of which 10 are supervised by the FDIC, 5 by the Federal Reserve, and 3 by the OCC. The 18 banks constitute over 10% of all minority depository institutions (MDIs) in the country. They have $2.9 billion in assets, which is about 1% of all MDI assets. Three of the 18 banks are also CDFI banks.

The geographic distribution of the 18 Native banks is as follows: 10 in Oklahoma, one each in North Carolina, Wisconsin, Colorado, Iowa, Minnesota, Missouri, North Dakota and Montana. The largest is over $452 million and the smallest is about $30 million. The average size is $158 million and the median size is $130 million.

The performance of Native banks is solid. From the latest financial data, all 18 Native American banks were profitable over 80% had earnings gains. Compared to other MDIs, Native banks have higher yields on earning assets. However, they also have lower returns on all assets and higher expenses. Native banks have an average efficiency ratio of 71 (vs. all MDIS at 54). This means that it costs 71 cents to bring in a dollar of revenue at Native banks, while it only cost 54 cents to bring in a dollar of revenue for all MDIs. Their Return on Assets ratio at 1.50 is lower than all MDIs, but still strong. Return on equity is also strong at 13.60. Native banks also experience low charge-offs on their loans at 0.06, indicating that Native banks are not inherently riskier institutions.