Author

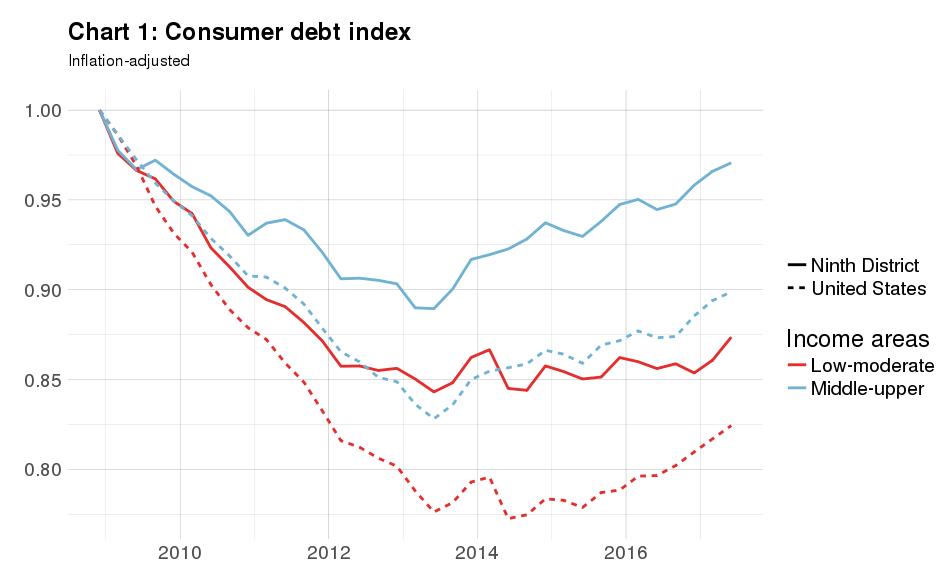

Since consumer debt levels peaked in 2008, debt levels in low- to moderate-income areas dropped steeper and then increased slower than debt levels in middle- to upper-income areas.* In addition, consumer debt levels in the Ninth District didn’t drop as steeply and, in recent years, grew faster than those for the U.S. as a whole (see Chart 1).

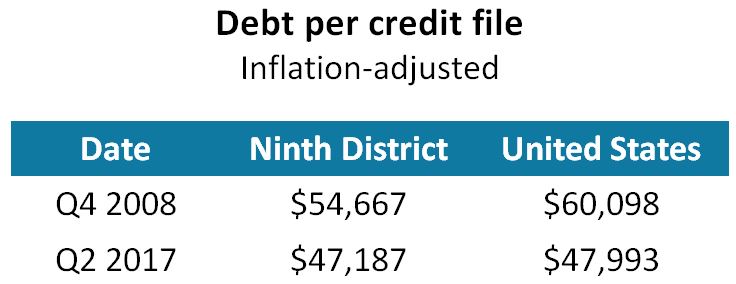

Adjusted for inflation, consumer debt levels in the Ninth District and U.S. remain below their 2008 peak, but are at record highs in nominal terms. Debt levels on a per capita basis decreased as the number of U.S. credit files increased by 25 million, or 11 percent, since 2008—an increase that was slightly faster than the increase in the adult population. In second quarter 2017, debt-per-credit-file levels in the Ninth District were slightly lower than in the U.S. (see table below).

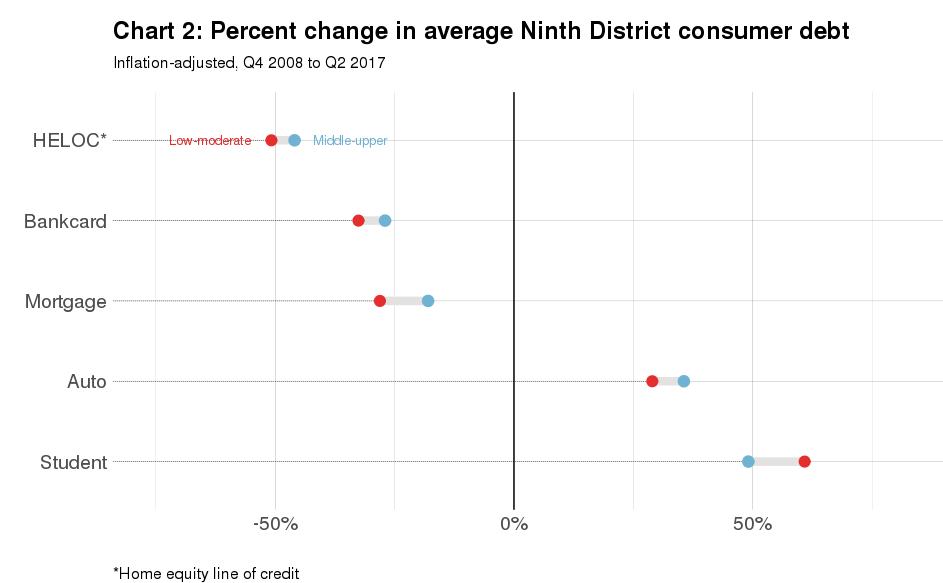

Home equity, credit card, and mortgage debt decreased since 2008 in low- to moderate-income and middle- to upper-income areas, with somewhat larger decreases in low- to moderate-income areas (see Chart 2). Since 2008, underwriting standards for subprime home mortgages tightened, which likely impacted low- to moderate-income borrowers more than middle-to upper-income borrowers. This likely explains a portion of the disparity in home mortgage debt growth between these two areas. Meanwhile, student and auto loan debt increased since 2008, with more student loan growth in low- to moderate-income areas. Trends for the U.S. are similar to those for the Ninth District.

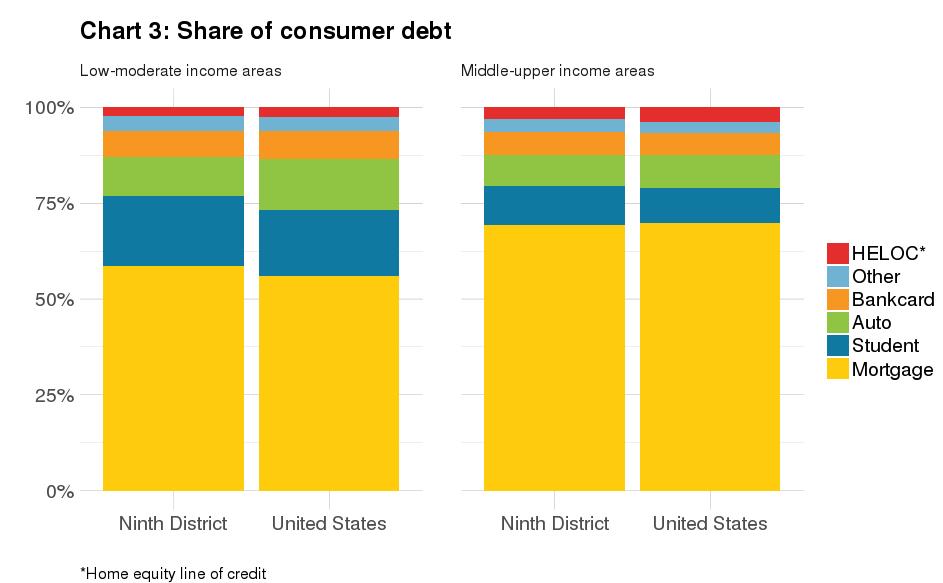

Student and auto loan debt make up a relatively larger share of total outstanding consumer debt in low- to moderate-income areas, while mortgage debt is a larger share of total consumer debt in middle- to upper-income areas (see Chart 3). The composition of consumer debt among Ninth District borrowers largely mirrors that of the nation, although a larger share of Ninth District low- to moderate-income consumers have mortgage and student loan debt compared with low- to moderate-income consumers in the U.S. Higher levels of homeownership and educational attainment in the Ninth District likely contribute to these differences.

* A low- to moderate-income area is defined in Home Mortgage Disclosure Act and Community Reinvestment Act regulations as a census tract where the median family income is less than 80 percent of a Metropolitan Statistical Area’s (MSA) median family income. For a non-MSA census tract, the median family income is compared with the median income of the non-MSA portion of the state in which it is located. A middle- to upper-income census tract is defined as having a median family income above 80 percent of an MSA’s median family income or the median income of the non-MSA portion of the state in which it is located.