Authors

Solomon Polansky

After the financial crisis of 2008, global appetite for safe currencies led to a continuous appreciation of the Swiss franc from 1.6 per euro in 2008 to almost 1.1 francs per euro in 2011—put otherwise, one franc equaled 0.63 euros in 2008 and 0.91 three years later. In September 2011, concerned about the negative effects that the franc’s growing strength was having on the Swiss economy, the Swiss National Bank (SNB) announced that it would set a floor at 1.2 francs per euro. It explicitly stated that it would “no longer tolerate” further appreciation and would enforce the floor “with the utmost determination.” It was “prepared to buy foreign currency [i.e., euros] in unlimited quantities.”

Indeed, the value of the Swiss franc against the euro remained steady around 1.2 for almost four years, but in January 2015, right around the time the European Central Bank announced its quantitative easing plan, the SNB abandoned the floor. The franc rocketed up 39 percent against the euro before settling down to a 20 percent appreciation. The move caused “panic,” according to The Economist. “The Swiss stock market collapsed.” Echoing a question asked by many, the Economist pondered, “Why did the SNB provoke such panic?”

Though rare, such moves are not unprecedented. The German Bundesbank, for example, unpegged the Deutsche mark against the U.S. dollar in 1971, leading to a major currency appreciation. In both cases, the central banks suffered as their large holdings of foreign assets (euros at SNB; dollars at Bundesbank) lost value. The SNB, for instance, had purchased nearly $500 billion worth of euros by 2014 to maintain the floor; after all, in 2011 it declared that it was committed to buying euros “in unlimited quantities.” Its decision to drop the peg—and stop buying euros—trimmed the value of the SNB’s euro holdings by a fifth: a painful self-inflicted loss.

So, why did the SNB abandon the floor?

A model to explore and explain

In “Reverse Speculative Attacks,” Minneapolis Fed economists Manuel Amador, Javier Bianchi and Fabrizio Perri, with Northwestern University’s Luigi Bocola, develop a “simple theory” to investigate decisions like the one by the SNB—their timing and external factors that might shape them.

The paper’s title derives from the notion of a conventional speculative attack. In the conventional story, a central bank commits to a peg with a foreign currency, backing the peg with its foreign reserves. Investors, however, believe that the peg is not sustainable and that the domestic currency will eventually depreciate. As a result, they sell massive quantities of domestic currency, exhausting the monetary authority’s foreign reserves. This forces the central bank to devalue its currency.

In a reverse speculative attack, investors believe that the domestic currency will appreciate and thus buy massive amounts of the domestic currency. The central bank, however, can always supply domestic currency and accumulate foreign reserves; hence, it cannot be forced to abandon its exchange rate policy. But though it didn’t have to abandon it, the SNB did.

Current pegs and future losses

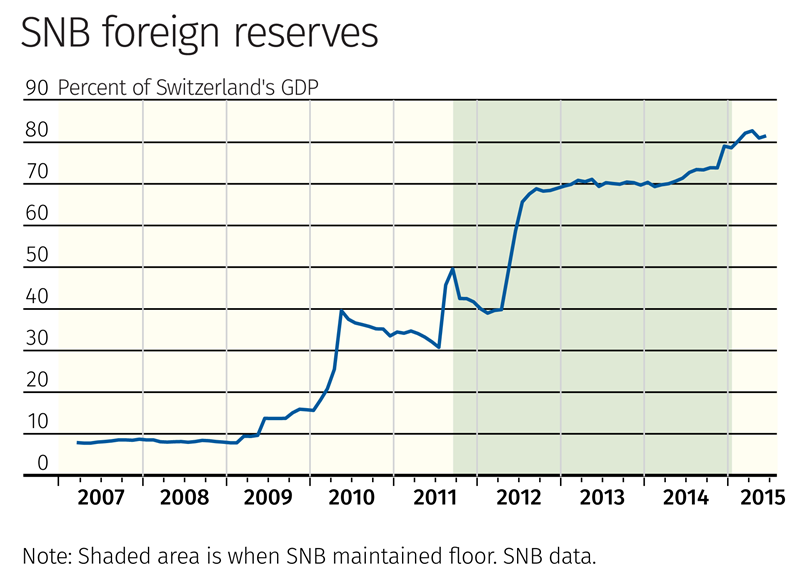

A bit of context may help explain the economists’ quest. A central bank has two options when it sets a peg but knows that markets consider its domestic currency undervalued. The first is to dutifully maintain the peg. The bank will suffer no immediate losses. It continues purchasing foreign assets at a blistering rate, thereby expanding its balance sheet. As Amador et al. observe, “In principle, it could have been feasible for SNB to increase its domestic liabilities (i.e., currency) while acquiring the foreign currency assets necessary to maintain the peg.” Indeed, the bank did acquire a huge euro stockpile—$500 billion worth, well over 70 percent of Switzerland’s GDP. (See the accompanying figure.)

Alternatively, the central bank can abandon the peg and let its currency appreciate as the market dictates, incurring immediate losses, but keeping its balance sheet to a more comfortable size. In January 2015, that’s exactly what the SNB did.

The economists theorize that while maintaining the peg and avoiding immediate losses is an attractive option, the large and growing balance sheet carries inherent risk. “When the balance sheet increases significantly,” they suggest, “the second choice becomes more attractive, and the Central Bank chooses to abandon the peg.”

Why? Risk of even more damage. “The current appreciation prevents a larger appreciation in the future, that would have led to much greater losses.”

The hypothesis would, if true, explain what markets evidently didn’t understand and anticipate: Central banks that initially perceive a peg as attractive—and therefore accumulate large reserves of a foreign currency—may later abandon the peg as concern about future losses comes to dominate.

Analytical approach

To analyze their theory, the economists build a model of an economy with a central bank using domestic currency and a large trading partner using a different currency. The central bank wants to maintain a fixed exchange rate between its domestic currency and the trading partner’s.

The central bank returns profits to—or recoups losses from—the nation’s treasury. But the economists suggest that the bank will, to ensure its viability, commit to avoiding losses above a pre-established point. That limit is set by political feasibility—losses could become so large that the treasury would refuse to recapitalize the bank, thereby undermining the central bank’s ability to conduct monetary policy. The central bank sets a loss threshold to avoid that existential threat.

To understand the role of external factors likely to affect bank decision-making, the model also incorporates demand for domestic currency (and shocks thereto) and variation in foreign interest rates, assumed to be random.

Notice that foreign demand for domestic currency and shocks to foreign rates are all factors that make life hard for the SNB. For example, suppose there’s an increase in foreign demand for Swiss francs. If the SNB does nothing in response, that would lead to an appreciation of the franc, which the SNB does not like. The SNB can avoid this appreciation by selling more Swiss francs and accumulating foreign reserves, but that expands its balance sheet and puts the bank at risk of future losses.

The model is then used to study what would persuade the central bank to abandon the peg—that is, when would a “reverse speculative attack” happen—and it shows that attacks happen if and only if the loss constraint is binding. That is to say, fear that maintaining the peg will lead to balance sheet losses that exceed the established threshold and thereby undermine the bank’s existence convince the bank to abandon the peg and suffer far smaller short-term costs.

The team then performs a numerical analysis, supplying parameter values consistent with real world data. Their results are qualitatively consistent with the real-world decision to break the peg (though with quantitative inconsistencies).

“Increases in money demand and/or a fall in the international interest rate can lead the Central Bank to first accumulate a large amount of reserves and then to abandon the peg,” they write. In response to either shock, “the Central Bank abandons the peg because maintaining the exchange rate … involves a large reserve accumulation, which coupled with the appreciation risk may lead to losses in the Central Bank’s balance sheet” that are unsustainable. By dropping the peg and allowing its currency to appreciate, the SNB “realizes some of these losses when reserves are still low, and [reduces] … future losses.”

But the model falls short quantitatively on two fronts. It projects an increase in reserves twice as large as seen in Swiss data, and domestic interest rates fall more sharply in the model than in reality. The economists suspect this is due to not “model[ing] a lower bound on interest rates and the patterns of money demand and capital flows around that bound.”

More work ahead

Amador et al.’s theory of central bank response to reverse speculative attacks correctly predicts firm but conditional resolve to maintain a peg, followed by abandonment when the situation warrants. At first the central bank accumulates large reserves, but when risk associated with these reserves grows too great, the bank breaks the peg: exactly what happened with the SNB.

The economists conclude by noting that model simplifications—particularly ignoring a lower bound on nominal interest rates—means that further research is required. “More work on reverse speculative attacks is useful and relevant” not only for better understanding of such events, they write, “but also because it sheds light on the limits of monetary policy … at very low interest rates”—a prominent feature of developed economies in current times.