Author

When governments roll the dice with debt, a shudder goes through financial markets—and the broader economy. In 2010-12, on the heels of the Great Recession, several eurozone countries with large fiscal deficits and/or debt suffered sovereign debt crises characterized by soaring interest rates on government debt, higher borrowing costs for households and firms, falling stock indexes and other asset prices, and faltering economic activity. (In Greece, a long-running debt crisis culminated last summer in a missed payment to the International Monetary Fund and nationwide bank closures.)

A standard explanation for these financial disruptions is that exposure to devalued government bonds increases the cost of raising funds for banks; they pass along these higher costs to firms, raising interest rates and discouraging capital investment. This view was a motive for massive lending to banks by the European Central Bank (ECB) during the sovereign debt crisis.

But what if constrained liquidity isn’t the only factor that leads banks to tighten credit when government debt gets out of hand? Recent research by Luigi Bocola, a former research economist at the Federal Reserve Bank of Minneapolis and an assistant professor at Northwestern University, suggests that heightened lending risk in the shadow of a potential sovereign default also plays a role.

In “The Pass-Through of Sovereign Risk” (Minneapolis Fed Working Paper 722), Bocola describes this additional source of credit tightening and quantifies its impact on lending behavior and economic output in Italy during the European debt crisis of 2010-11. Constructing a model economy in which bankers are mindful of the possibility of default, Bocola finds that a large share of the increase in borrowing costs during the debt crisis can be attributed to banks’ belief that lending to firms has become riskier.

The economist also uses his model to evaluate the effectiveness of the ECB’s efforts to maintain a cushion of liquidity for cash-strapped European banks. It turns out that the ECB’s loan lifeline did little to improve credit conditions or increase economic output in Italy during the debt crisis.

Sand in the works

The bankers in Bocola’s model conduct business as usual, collecting savings from households and using these funds, along with their own accumulated equity or capital, to invest in long-term government bonds and to lend to firms. But in the model, a microcosm of conditions in Italy during the sovereign debt crisis, there is a risk of the government defaulting on its debt. The mere prospect of this event throws sand into the works of financial intermediation.

Mathematical rules drawn from his model, and estimated from data on the exposure of Italian banks to sovereign debt risk during the crisis, govern the financial frictions in the model—the constraints imposed on banks when the risk of default increases.

In the model, a sharp rise in the likelihood of a government default (Bocola doesn’t dwell on the reasons for this increased default risk) sets off a series of events that restricts access to bank credit. One reason for this credit squeeze is heightened expectations of default, which slash the value of government bonds. Banks saddled with low-value government securities face a decline in net worth. This raises the cost of borrowing from investors and households; as a result, banks raise interest rates and lending to firms drops.

Another source of credit tightening in the model—one that has received scant attention from other researchers—is the perceived increased risk of commercial lending as the threat of sovereign default looms. Even when banks have sufficient liquidity, they anticipate funding constraints in the future and worry that firms hurt by recession triggered by default may not repay their loans. Thus these loans are seen as riskier “because bankers now attach a higher likelihood to a state of the world (a sovereign default) in which [loans] pay out little precisely when bankers are in most need of wealth,” Bocola writes.

As a precaution, banks charge firms higher interest as compensation for holding risky assets and sell some of their loans to reduce their exposure. Market demand for loan assets falls, and firms find credit harder to obtain.

By restricting access to credit, both mechanisms discourage capital spending by firms, with negative consequences for the Italian economy in the model.

The price of risk

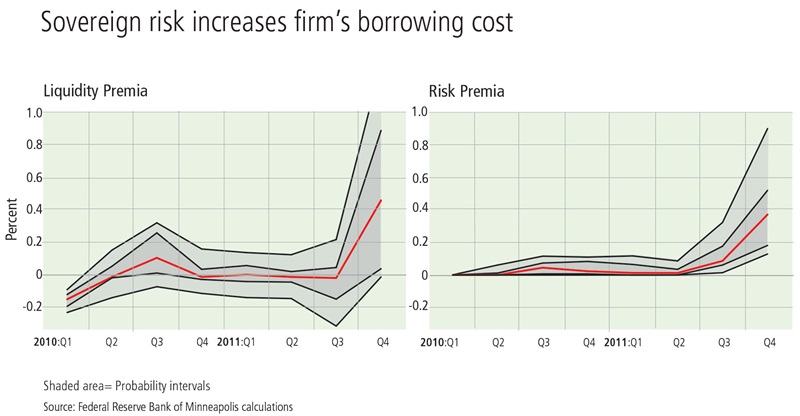

Model in hand, Bocola uses it to conduct an experiment, comparing a sovereign-risk scenario with one in which there is no risk of government default. The results quantify the impact of the sovereign debt crisis on the borrowing costs of firms in Italy and on economic activity in the country. They also allow Bocola to isolate the effect of banks’ precautionary motives on credit conditions, as distinct from current constraints on their liquidity.

In the model, the higher probability of an Italian default in the second half of 2011 leads to a marked increase in interest rates paid on loans by firms (see chart). The experiment also shows that bankers’ concerns about the riskiness of firms contributed significantly to credit tightening in Italy. In the last quarter of 2011, this “risk channel” accounted for 45 percent of the increase in borrowing costs due to the sovereign debt crisis.

By reducing firms’ ability to invest in production, higher interest rates sapped Italy’s economic growth; the model predicts that in the first quarter of 2012, output would have been 1.4 percent higher without the financial drag induced by the debt crisis. Thus “a mere increase in the probability of a sovereign default depresses real economic activity,” Bocola writes.

In response to the sovereign debt crisis, the ECB in early 2012 launched a lending program in Italy and in several other eurozone countries meant to prevent lending activity from seizing up. Bocola uses his model to assess the effects of these longer-term refinancing operations (LTROs), in which European banks borrowed hundreds of billions of euros from the ECB.

The LTROs were expected to lower interest rates and to spur increased economic output. Instead, in the model—reflecting the state of the Italian economy at the time—these measures improved very little. Because banks’ reluctance to lend was in large part based on aversion to risk, shoring up their liquidity was largely ineffective in easing credit conditions.

By highlighting the importance of firm risk in raising borrowing costs, Bocola’s research offers lessons for policymakers weighing the best course of action to restore credit flows during debt crises. “If this mechanism is quantitatively important, policies that address the heightened liquidity problems of banks but do not reduce the increased riskiness of firms may prove ineffective in encouraging bank lending,” he writes.

Ongoing research by Bocola, including a joint paper with Cristina Arellano, a senior research economist at the Minneapolis Fed, examines other aspects of sovereign debt crises, such as the role of self-fulfilling expectations and the impact of the European debt crisis on the private sector.