Authors

The district economy saw modest progress so far in 2015, with a number of industries posting employment gains alongside a slowdown in the natural resources sector. The outlook is also slightly positive as respondents to the professional business services survey are optimistic for the upcoming year, while the results of the Minneapolis Fed’s forecasting models point to slowing in employment growth through 2016. In the agriculture sector, crop prices are expected to remain low, providing a strain on farm income.

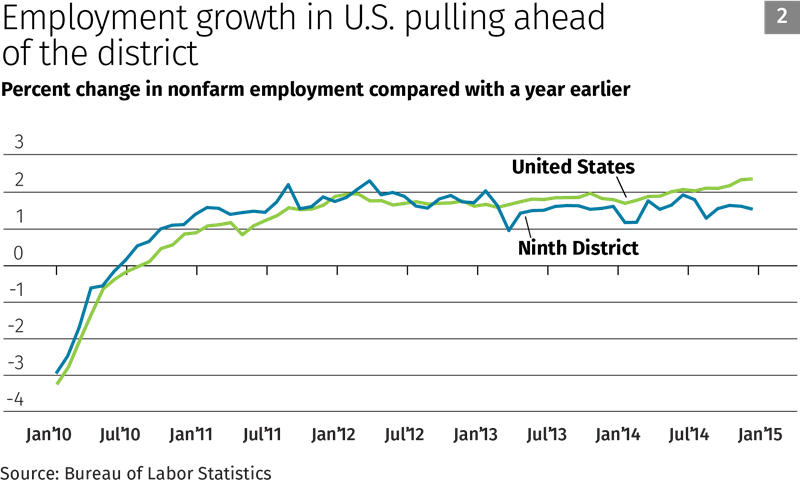

District employment growing slower than the nation’s

Employment levels increased in a number of district industries, but fell short of growth at the national level. Total district nonfarm employment increased 1.2 percent in May from a year earlier, while U.S. employment grew 2.2 percent (see Chart 1). The district’s strongest employment gains were posted by construction (2.7 percent), manufacturing (1.8 percent) and information and financial services (1.6 percent). Meanwhile, natural resources and mining decreased 2.1 percent compared with a year ago.

Over the past year, employment growth in the United States has exceeded that of the district (See Chart 2). A couple of factors come into play. First, employment growth was stronger in the district than nationally following the Great Recession, as economic activity continued to languish in other areas of the country from 2010 to 2013. Since then employment has been catching up in those other areas as they experience a later recovery.

Second, strong employment gains from the expansion in energy production in North Dakota contributed to district employment growth during 2010 to 2013. However, with the drop in oil prices and decreased drilling activity in the western part of North Dakota since the end of 2014, North Dakota has posted job losses over the first five months of 2015 due to layoffs of oilfield workers.

At the end of September 2014, when oil prices were above $90 per barrel, 197 drilling rigs were active in the region (189 in North Dakota, eight in Montana). Then, oil prices around the world collapsed. For example, the West Texas Intermediate crude oil price dropped, holding at around $50 per barrel from January to April and closer to $60 through June, and recently has dropped back to $50. By the beginning of July there were 76 drilling rigs active in North Dakota and one drilling rig working in Montana. Oil production also slowed in the region, dropping about 5 percent from its peak in December.

Despite the slowdown in oil drilling, unemployment rates in the region have risen only a little, and from very low levels as demand for construction workers remained strong to build public and energy sector infrastructure. When the pace of drilling was still rapid earlier in 2014, infrastructure was far behind needs.

While the slowdown in the oil patch has had an impact on the district’s employment tally, the overall impact is likely contained in and around that region. As reported earlier in “How Wide is the Ripple Effect? ” (see July 2013 fedgazette online) the impact of activity in the Bakken doesn’t seem to register in aggregate statistics much beyond 100 miles and at most 200 miles away. Furthermore, an analysis by the Minnesota Department of Employment and Economic Development released in April using a range of assumptions for future oil prices, shows that the energy-producing areas in North Dakota are expected to have a modest 0.1 percent to 0.3 percent overall net impact on Minnesota’s economic output by 2019 and 0.2 percent or less impact by 2030.

The outlook for district employment growth is slightly positive. According to the professional business services survey, the outlook for hiring is positive, with 21 percent of firms expecting to increase full-time staff while 7 percent expect decreases (see related story). However, the Minneapolis Fed’s forecasting models predict a slowing in employment, with slight decreases in Minnesota and Wisconsin during 2016, slight increases in Montana, South Dakota, and the Upper Peninsula, and a rebound in employment growth in North Dakota. Meanwhile, stronger growth is predicted for national labor markets relative to the district in 2016. Unemployment rates in the district are expected to increase slightly by 2016, but remain at relatively low levels, while the U.S. unemployment rate is predicted to drop below 5 percent.

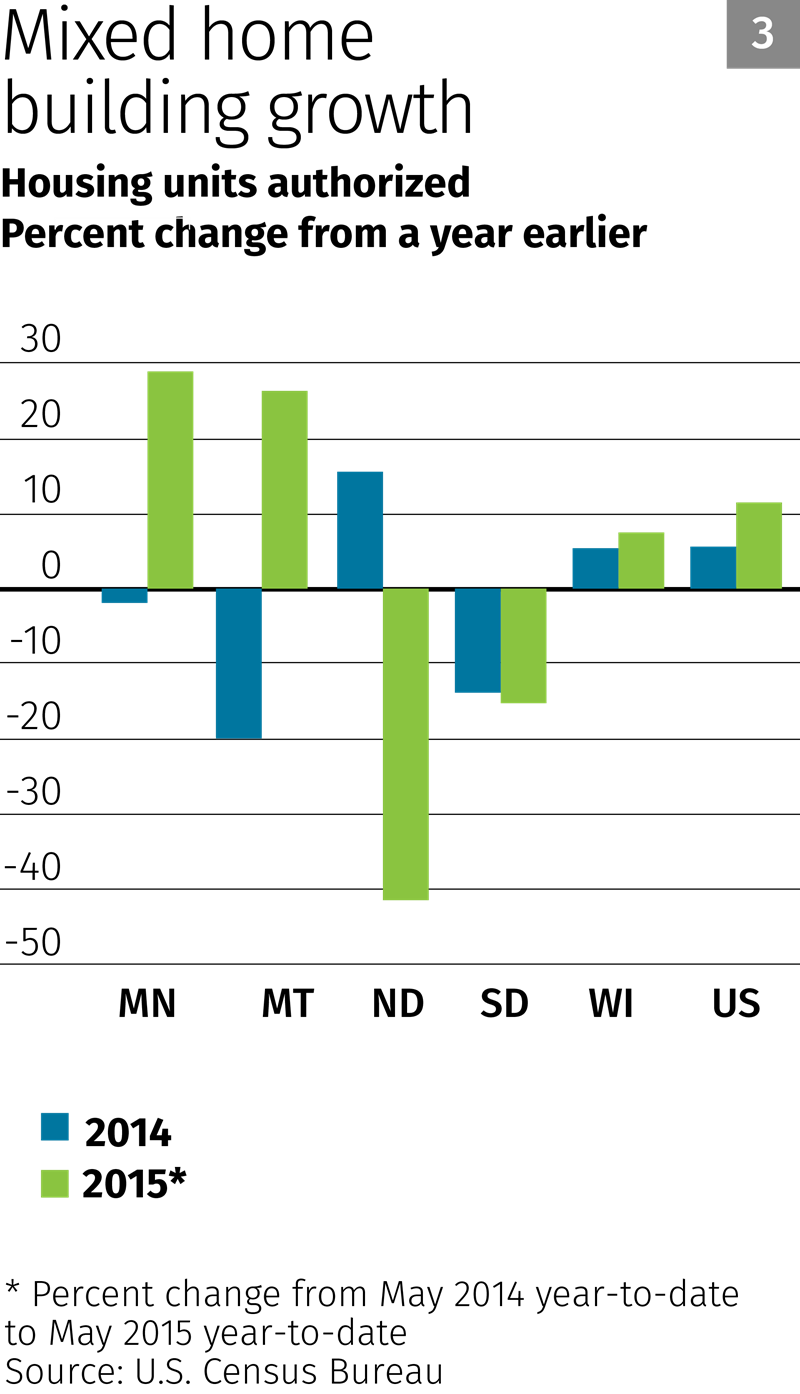

Homebuilding mixed, manufacturing slowing

Several large commercial building projects underway in the district have helped boost construction activity. However, housing units authorized, a signal of future residential building, has varied across the district (see Chart 3). During the first five months of 2015, housing units authorized posted strong gains in Minnesota and Montana, but dropped substantially in North and South Dakota, compared with the same period a year earlier. District homebuilding has picked up from the depths of the Great Recession, but is still far from the annual peak reached in 2004. One reason for this is that population growth and household formation are generally slower than a decade ago (with the exception of North Dakota); therefore, a return to annual home building levels in the district prior to the Great Recession is not to be expected.

Meanwhile, manufacturing activity has slowed somewhat in the district, despite year-over-year employment gains. According to a June survey of purchasing managers released by Creighton University, results indicated moderate expansion in manufacturing in Minnesota and South Dakota, and a contraction in North Dakota. The manufacturing sector has struggled from slower exports, in part due to the stronger dollar relative to currencies of trading partners (see related story).

Consumer spending and tourism are optimistic

Nationally, retail sales increased a solid 1.2 percent in May from the previous month and were 2.7 percent higher than a year ago (not adjusted for inflation). In the district, a number of retailers have reported gains in sales during the past few months, although retail activity has slowed in the energy producing areas of North Dakota and Montana.

Tourism officials and district business owners associated with tourism are optimistic for a strong season. Gasoline prices have increased since earlier in the year, but remain much lower than they were going into last year’s summer, which will help to keep travel costs down. According to a survey of Minnesota lodging businesses conducted by the state’s tourism office, 53 percent of businesses expect summer revenue to increase from a year ago, while 11 percent expect decreases.

Overall personal income gains during the first quarter compared with a year earlier were positive. But growth was depressed by decreases in farm income, which fell more than 25 percent in district states, except for Montana where farm income was higher than last year. The Minneapolis Fed’s forecasting model predicts slow income growth in 2015, likely influenced by the first quarter drop in farm income, but predicts growth rates will pick up in 2016.

In addition to relatively low gasoline prices, consumer prices overall have stayed in check. In May, the U.S. personal consumption expenditures price index was only 0.2 percent higher than a year earlier, while the core rate of inflation, which doesn’t include relatively volatile food and energy prices, increased 1.2 percent.

For farmers, better weather but falling prices

After two years marked by long winters, farmers finally got a reprieve in 2015 from late spring planting and were able to get crops in the ground on a more typical schedule. Planting progress and emergence rates for corn, soybeans and spring wheat as of late-June were slightly ahead of their five-year averages throughout most of the district. The majority of those crops were rated in good or excellent condition over the same period. Solid rainfall has also left much of the district free of drought, with the exception of parts of Montana. But the biggest news so far this year has been the massive avian influenza outbreak that has led to the deaths of an estimated 48 million chickens and turkeys in 15 states. The bird flu has been especially concentrated in Minnesota, which is the nation’s largest producer of turkeys, and in Iowa.

Unfortunately for farmers, crop prices remain at relatively low levels. The U.S. Department of Agriculture forecasts corn, wheat and soybeans prices to decrease this year and into 2016 (see Chart 4). For livestock producers, the outlook is a little better. Prices for cattle are historically high and expected to remain stable. Meanwhile, hog prices, which have also been strong, have retreated slightly. Dairy producers have seen milk prices drop dramatically to margin-squeezing levels, though they, and other animal product producers, benefit from lower crop prices that bring down feed costs.

Due to lower crop prices, district agricultural producers began the year in worse financial shape than in recent years. According to the Minneapolis Fed’s first-quarter (April 2015) agricultural credit conditions survey, 79 percent of respondents reported lower farm income compared to the previous three months, while only 8 percent noted increases. Agricultural lenders mostly expected farm profits to fall further in the second quarter of 2015, with 78 percent expecting decreased income and just 4 percent expecting increases. On balance, the outlook for farm household and capital spending was also for decreases.

Joe Mahon is a Minneapolis Fed regional outreach director. Joe’s primary responsibilities involve tracking several sectors of the Ninth District economy, including agriculture, manufacturing, energy, and mining.