Author

The number of consumers who experienced a default during the housing market’s recent boom and bust and the Great Recession that followed was unprecedentedly large. In the Ninth Federal Reserve District alone, an estimated 160,000 consumers experienced a default that resulted in the termination of their mortgage (either as a charge-off, which is when a lender deems a mortgage uncollectible, or as a foreclosure) between 2002 and 2009.1/ That prompts the question, How many of the consumers who went through a mortgage default have returned to the mortgage market?

In 2012, a nationwide study by economists at the Federal Reserve Bank of San Francisco found that only a small number (about 10 percent) of consumers reentered the mortgage market after defaulting on their original mortgage. The economists also found that consumers who experienced a mortgage default in the early 2000s (prior to the housing market’s boom and bust) or whose initial credit scores were fairly high (greater than 650) returned to the mortgage market at a higher rate when compared to those who defaulted after the early 2000s or had lower credit scores.2/

In other words, timing and credit scores matter. But what about geography? Specifically, does a consumer’s post-default return to the mortgage market differ based on whether they live in a lower-, middle-, or upper-income area? That question is likely to be pertinent to practitioners and policymakers, especially those concerned with homeownership in lower-income neighborhoods.

A recent analysis by the Federal Reserve Bank of Minneapolis suggests that yes, geography does matter, and that consumers in middle- or upper-income neighborhoods returned to the mortgage market twice as fast as those who lived in lower-income neighborhoods.

Measuring mortgage defaults and market returns

The Minneapolis Fed’s analysis used a proprietary dataset from Equifax containing a sample of credit files for roughly 5 percent of all consumers with an active credit file in the Ninth District. In order to determine which consumers experienced a mortgage default between 2002 and 2009, analysts used mortgage account information—also known as tradeline data—from each credit file to identify if a mortgage was past due and its balance was zero or missing for a specific quarter of a given year. (Here, past due refers to those mortgages identified as being more than 120 days in default. A zero or missing balance indicates that a mortgage has been terminated in a credit file.) Using an Equifax consumer identification code, those consumers who had a default followed by a zero or missing balance were matched to all future tradeline data (through the last quarter of 2012) to determine if they subsequently acquired a new mortgage.3/ If a new mortgage was acquired by the consumer, analysts calculated a duration difference, in months, between the end of the quarter of the original default and the date of the new mortgage origination. Overall, only a small number (about 13 percent) of consumers in the Ninth District reentered the mortgage market after defaulting on their original mortgage4/ —a finding consistent with the work of the San Francisco Fed economists mentioned previously.

Next, the analysts examined whether geographic differences existed. Previous research by the Minneapolis Fed and others has demonstrated that credit scores tend to correlate strongly with the average household income of a neighborhood.5/ Given that, and because income data are more readily available to the general public than credit data, the analysts decided to use neighborhood-level measures of household income as a substitute for credit scores. They coded each consumer credit file according to the census tract where the consumer resided at the time of the default. These census tracts were, in turn, identified as lower-, middle-, or upper-income based on the median income for each tract compared to that of its respective metropolitan median or non-metropolitan state median, as calculated in the U.S. Census Bureau’s 2009 American Community Survey. Finally, consumers were divided into two groups—those who experienced a default before the January 2006 peak in home prices and those who experienced a default after, during the decline—in order to gauge the effect these two periods may have had on the mortgage market outcomes of post-default consumers.

Neighborhood variations

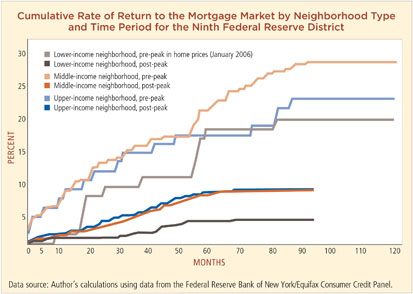

The graph below depicts the cumulative rate of return to the mortgage market for consumers who lived in either lower-, middle-, or upper-income neighborhoods by whether the date of their mortgage default occurred prior to or after the peak in home prices. It shows that consumers in middle- or upper-income neighborhoods returned to the mortgage market at rates higher than those of consumers in lower-income neighborhoods, both before and after the peak.

Prior to the peak in home prices, when fewer defaults occurred overall, consumers in middle-income neighborhoods had the highest return rate, with roughly one-quarter obtaining a mortgage over time (up to ten years after a default) compared to one-fifth of those living in upper-income and one-sixth of those living in lower-income neighborhoods. After the peak in home prices, consumers in all neighborhoods returned much more slowly to the mortgage market, if at all. The slowness was especially pronounced for consumers from lower-income neighborhoods, whose post-default rate of returning to the market was almost 15 percentage points less after the peak than before—a rate roughly half as fast as that of consumers in middle- and upper-income neighborhoods.

Future implications

Overall, recent evidence reveals that the vast majority of consumers who have experienced mortgage defaults did not return quickly to the mortgage market afterward, especially during and following the recent recession. As the analysis described here indicates, this is especially true of post-default consumers from lower-income neighborhoods. For policymakers and practitioners seeking to expand homeownership in those neighborhoods, the findings suggest that a wider array of affordable housing solutions for families, beyond homeownership, may be needed in the future.

1/ Author’s calculations using data from the Federal Reserve Bank of New York/Equifax Consumer Credit Panel.

2/ William Hedberg and John Krainer, “Credit Access Following a Mortgage Default,” Federal Reserve Bank of San Francisco Economic Letter, October 29, 2012.

3/ This analysis does not make distinctions for consumers who may have held multiple mortgages or for those consumers who are investors or homeowners or both. The analysis also does not account for the influence that Chapter 13 bankruptcy may have had in holding off a mortgage default for consumers.

4/ Author’s calculations using data from the Federal Reserve Bank of New York/Equifax Consumer Credit Panel.

5/ For example, see Report to the Congress on Credit Scoring and its Effects on the Availability and Affordability of Credit, Board of Governors of the Federal Reserve System, 2007, available at www.federalreserve.gov.

Michael works to advance the economic well-being of Indian Country and low- to moderate-income individuals, households, and communities. He has conducted research and published articles on affordable housing, community development corporations, homeownership disparities, and foreclosure patterns and mitigation efforts.

{kind=link}