Author

As the subprime mortgage crisis continues to unfold, observers have been hunting for both culprits and solutions. A prime suspect has been the mortgage broker industry, the growth of which paralleled the rise in subprime mortgages. And a proposed solution has been tighter regulation of mortgage brokers.

On the face of it, this makes perfect sense: If incompetent or dishonest brokers have encouraged borrowers to take out loans beyond their means, then targeting these abuses through stricter governmental requirements on brokers should help prevent future problems.

But a recent empirical examination by two Fed economists casts doubt on that solution. In the first comprehensive assessment of relationships between mortgage broker licensing and market outcomes, the economists find that most regulatory steps appear to have no clear connection to consumer outcomes, but one financial regulation (surety bond and minimum net worth requirements) is consistently related with conditions that seem worse for both brokers and borrowers.

The economists—Fed visiting scholar Morris Kleiner, of the University of Minnesota, and Richard Todd, vice president of Community Affairs at the Minneapolis Fed—are cautious in their conclusions: Their study finds statistical relationships that suggest unintended consequences from regulating brokers, but it doesn’t prove causality. Still, the possibility of negative outcomes from greater regulation is enough to counsel policymakers to tread carefully.

“[O]ur results,” write Kleiner and Todd in their December 2007 National Bureau of Economic Research (NBER) working paper, “underscore the need for both more research on this topic and a cautious approach to imposing additional restrictions on entry into the mortgage broker business and occupation” [emphasis added].

Morris Kleiner, University of Minnesota and

Richard Todd Federal Reserve Bank of Minneapolis

Current events

A day doesn’t go by without another wave of stories about mortgage foreclosures and the toll they’re taking on individuals, communities and the international economy. Dealing with the aftermath is a major preoccupation, but policymakers rightly turn attention to prevention of future problems. Subprime mortgages, most agree, are a good product that can help people with less than stellar credit obtain access to financing for homeownership. But the widespread extent of foreclosures across the country demonstrates that too many people were sold a product they couldn’t handle financially. How can this be prevented in the future?

Many policymakers have called for tighter regulations on the brokers that sell mortgages, the middlemen (and women) who, in return for a fee, play matchmaker between lenders and borrowers who want to finance a home purchase.

In September 2007, Sen. Christopher Dodd introduced a bill to reform the mortgage broker industry. After a similar bill was introduced in the House of Representatives in October, Fed Governor Randall Kroszner testified before a House committee that the bill’s effort to provide greater oversight and regulation of mortgage brokers was “an approach that has merit.” In February, Sens. Dianne Feinstein and Mel Martinez introduced another bill that called for a federal registry and national licensing standards for mortgage brokers. And in March, the President’s Working Group on Financial Markets recommended strong nationwide licensing standards for mortgage brokers.

These federal efforts have been paralleled by state-level proposals to address the industry, starting with a collaborative project by the Conference of State Bank Regulators and American Association of Residential Mortgage Regulators to develop a national mortgage licensing system, as recommended by the presidential working group.

The industry itself has asked for more regulation. The National Association of Mortgage Brokers (NAMB) has called for “an increase in professional standards, education requirements and criminal background checks.” And while it deflects blame for the subprime problem, saying that a recent Government Accountability Office study “vindicates brokers,” it has announced the creation of an online “integrity training” program for its members.

All this Sturm und Drang has yet to result in substantive federal reform measures, and state regulation remains uneven. Nevertheless, it seems likely that policymakers will enact some reforms in the coming months and years. But Kleiner and Todd’s research suggests that at least some forms of increased regulation may have consequences perversely at odds with policymakers’ goals.

“We do not provide a full causal interpretation of these results,” they admit in the abstract to their paper, “Mortgage Broker Regulations that Matter: Analyzing Earnings, Employment and Outcomes for Consumers,” but “we take seriously the possibility that restrictive bonding requirements for mortgage brokers have unintended negative consequences for many consumers.” Understanding that counterintuitive result calls for a brief review of the evolution of the mortgage broker industry as well as a look at economic theory on the effects of regulation—and licensing, in particular.

Theory of licensure

The negative effect of inhibiting free entry into occupations was noted early on by Adam Smith, who observed that various crafts used long apprenticeships and limits on the number of apprentices per master in order to raise professional earnings. Free competition, he suggested, would lower prices and consequently wages and profits—an outcome that crafts sought to avoid. And apprenticing didn’t guarantee better work, thought Smith. “The institution of long apprenticeships can give no security that insufficient workmanship shall not frequently be exposed to public sale,” he wrote in The Wealth of Nations.

The issue of licensing “then became dormant [in economics],” observes Kleiner during an interview at the Minneapolis Fed (see sidebar). Not until a 1945 NBER monograph by Milton Friedman and Simon Kuznets on “Income from Independent Professional Practice” did economists again look carefully at the impact of occupational restrictions through licensing and other forms of professional gatekeeping. “In all professions,” wrote Friedman and Kuznets, “there has developed in the last few years an aristocratic, or at least a restrictive movement which, in a sense, is reminiscent of the medieval guilds.”

Later, in Capitalism and Freedom, Friedman developed the idea more fully in a chapter devoted to occupational licensure. Once a profession obtains a legal requirement that only those with a license can practice that profession, it restricts supply of professional services and thereby increases price (and profit). “Once licensure is attained,” wrote Friedman, “[t]he result is invariably control over entry by members of the occupation itself and hence the establishment of a monopoly position.”

Nor did licensing achieve its ostensible goal of improved quality, argued Friedman, echoing Smith. Looking at the medical profession in particular, Friedman said, licensure “renders the average quality of practice low by reducing the number of physicians, by reducing the aggregate number of hours available from trained physicians … and by reducing the incentive for research and development.” It also makes it harder, he added, “to collect from physicians for malpractice” since physicians are unlikely to testify against one another when they might be punished for doing so by losing the right to practice in approved hospitals.

Friedman’s view has been powerful among economists, but later work by George Akerlof, Kenneth Arrow and especially Carl Shapiro suggested a more nuanced view. Akerlof, in his famous work on asymmetric information, pointed out that the outcomes of licensing models may change when neither regulators nor consumers can directly observe the quality of producers before they buy their services. A licensing system can encourage practitioners to seek more training because they’ll be able to reap higher returns from training if untrained practitioners are excluded from the profession. Arrow suggested that licensing could diminish consumer uncertainty about service quality and increase demand for it.

Shapiro expanded on these concepts, explains Kleiner, and provided an expanded theory of occupational regulation relative to Friedman. Some individuals might want lower-quality services at lower prices; others might want high quality at a high price. If licensing keeps low-quality providers out of the market, then individuals who want a higher-quality service benefit from licensing while those who want lower-quality services lose.

“So Friedman would say everyone loses [from licensing],” says Kleiner, “but Shapiro said there are winners and losers, and whether you gain or lose depends on whether you tend to buy high- or low-quality services.” It is “a separating equilibrium,” wrote Shapiro; licensing “tend[s] to benefit consumers who value quality highly at the expense of those who do not.”

Evolution of brokers

The economics of licensing, then, are somewhat ambiguous. Whether, on net, it benefits or harms consumers and providers isn’t theoretically obvious. So when Kleiner and Todd began to look at the regulation of mortgage brokers, it wasn’t at all clear what they’d find.

What was clear was the tremendous growth of the profession. In the 1970s, most mortgages were handled by banks or savings and loans; George Bailey and his nonfiction counterparts brokered mortgage deals as bank employees, not as independent contractors. But with the S&L crisis beginning in the 1980s, life was no longer wonderful for savings and loans, and home buyers needing mortgages sought other avenues. Loan officers laid off by foundering S&Ls found new demand for their skill set.

“As the industry contracted,” notes Todd, “you had a lot of people who knew how to make loans and didn’t have an S&L to work for anymore. And you had an obvious need to continue to make mortgages.”

At roughly the same time, technological advances enabled quicker information flow from lenders to brokers to borrowers, and back again. First, fax machines proliferated, allowing a lender to send brokers a daily rate sheet of loan terms they’d offer to borrowers. Then the Internet enabled even faster transmission of data and documents between those who had money and those who needed it.

By the mid-1990s, these pieces were joined by another: credit scoring, the quantitative evaluation of creditworthiness. New technologies fostered the mathematical estimation of borrowers’ credit risk and dissemination of those data. “Lenders started to think, ‘Not only can I originate loans on a different model,’” says Todd, “‘but I can also think about pricing according to risk. I can have a prime loan and a subprime loan and [gradations] within those categories.’”

That opened up new markets entirely, providing opportunities in low-income communities that previously had seen little history of mortgage lending, and it did so without the lender needing to establish a physical presence in those communities. Without bricks and mortar, and with brokers as independent contractors, lenders could expand and contract with the market.

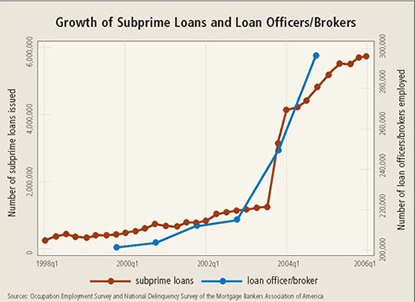

Conditions were perfect, then, for rapid expansion of both subprime lending and mortgage brokering. “Low overheads and the resulting ability to efficiently market within residential neighborhoods also helped brokers penetrate the emerging subprime market, which included many households who were somewhat unfamiliar with traditional mortgage lending institutions,” write Kleiner and Todd. “The number of mortgage brokers and the number of subprime mortgage originations grew in tandem” (see chart).

Market failures?

By 2004, mortgage broker firms were involved in the origination of over two-thirds of all mortgages, according to Kleiner and Todd, and “as the mortgage broker business grew, so did questions about the industry’s role and its effect on consumer welfare.” On the one hand, the growth of the industry demonstrated that consumers found it useful. The proliferation of mortgage products in the 1990s made the process of finding the “right” one difficult. Brokers smoothed the process for both lenders and borrowers by simplifying the search process and making matches between home buyers looking for a mortgage they could afford and money lenders looking for creditworthy customers. “Brokers can make the complicated task of shopping and applying for the increasingly wide array of mortgage products more manageable and efficient for borrowers and lenders alike,” write Kleiner and Todd.

On the other hand, some brokers took advantage of their customers, facilitating deals that had a high probability of going bad. “I think there’s enough solid anecdotal evidence to make clear that there were bad brokers who did things most of us find reprehensible,” says Todd. “But it would be very naïve to say there’s only one kind of broker and it’s the evil broker. Certainly, there’s plenty of reason to think that many brokers provide good service, and our correlations are very consistent with that notion.”

Nonetheless, observers have argued that market failures—specifically, information asymmetries—have allowed brokers to profit unduly at the expense of borrowers and lenders, especially in the subprime market. Their reasoning stems from the incentive issues inherent in the brokerage industry. Brokers are typically paid according to the size and number of deals they make and may receive further payments for arranging high interest rates. At least in the short run, whether the match is truly a solid one is (to them) a secondary consideration.

Thus the conflict is between broker interests and borrower/lender interests. Borrowers are often confused about mortgage products and processes, and they trust the broker to find them a good deal; lenders, in turn, trust that the broker is conveying accurate information regarding the borrowers’ creditworthiness. “This creates an opportunity,” write Kleiner and Todd, “for professionals, including mortgage brokers, to abuse that trust by, for example, recommending a mortgage that has a higher interest rate than the customer actually qualifies for, in order to obtain a higher fee.”

In theory, markets could address these problems. Lenders could monitor the quality of loans submitted by particular brokers. Better financial education and contracts could improve the broker-borrower relationship. But as of yet, note Kleiner and Todd, “market responses have not eliminated concerns about bad outcomes caused by asymmetric information and incentive conflicts in the mortgage broker market.” As a result, “public policymakers have entered the fray.”

Array of regulation

Indeed. During the past decade or so—well before the current crisis—government agencies at the state level enacted a wide range of regulations over mortgage brokers, specifically through licensing provisions applying to brokerage firms and individuals. Depending on the state, these provisions may include age, education, experience and residency requirements; minimum office space standards, such as maintaining a physical office in states of operation; evidence of ethical fitness and absence of criminal background; and minimum net worth or surety bonding.

Cynthia Pahl, a graduate student of Kleiner’s, was hired by the Minneapolis Fed in 2006 to compile a database of these state licensing regulations, and the Kleiner-Todd study relies heavily on it. Pahl’s database covers the 50 states plus the District of Columbia from 1996 to 2006 and includes 24 regulatory components. She assigned an integer value for the intensity of each component and developed two composite indexes to summarize regulatory strength.

The database reveals a significant range among states in regulatory oversight and a remarkable progression over time in licensing stringency. The average value of regulatory strength for all states rose from 3.2 in 1996 to almost 8 in 2005, according to one Pahl index. States such as Alaska and Wyoming had very little oversight in 2004; Florida, Montana and New Jersey regulated quite strictly.

This variation among states and change over time are what permit Kleiner and Todd to explore the relationships between licensing provisions, on the one hand, and labor and product market outcomes, on the other.

The study

Interviewed separately, both Todd and Kleiner use the phrase “Venn diagram” to describe the overlap in interests that brought them to this project. Kleiner has studied licensing theory and empirics throughout his career as an economist. Todd knows about the brokerage industry because of his community affairs responsibilities at the Fed; homeownership and mortgage lending are central aspects of his work. “It was an optimal combination of talents,” says Kleiner.

Over lunch at the Fed in the fall of 2005, the two began to discuss the commonalities of their fields, and the project slowly evolved. Kleiner’s students at the University of Minnesota began a project on the licensing of mortgage brokers; Todd became a resource for the class. Eventually, the Fed became a “client,” in a sense, for a class project examining regulation of brokers across the country. (A version of their work was published in the Minneapolis Fed’s Community Dividend. Pahl, a student in the class, was then hired to more fully develop the licensing database, the statistical foundation for the Kleiner-Todd study.

When the economists first crunched the numbers, the results were underwhelming. Kleiner looked at several years of panel data from all 50 states and Washington D.C., searching for associations between regulatory strength and numbers of brokers, foreclosures, subprime loans, wages and so on. Todd examined cross-section data on hundreds of thousands of loans in one year, 2005 (controlling, as Kleiner had, for other variables such as household income, unemployment rate, homeownership rates likely to impact labor and market outcomes). They found nothing.

“Our preliminary exploration of the influence of regulation on mortgage broker markets,” they wrote in a May 2007 version of the paper, presented at an NBER conference in Cambridge, Mass., “finds that it has a small and usually insignificant impact.” Regulation, it appeared, had very little effect on either the industry or the product. “Neither in Morris’ panel data nor in my cross section did we find any strong statistical relationships,” recalls Todd. “Nothing that was stable, nothing that stood up to a little robustness checking. It looked to be random noise. So we did report that negative outcome at a conference, and it was a little boring.”

But with encouragement from Minneapolis Fed consultant Tom Holmes and other scholars, the two dug deeper. While they’d found nothing significant between the general indexes of regulatory strength and the outcome variables, they noticed that one of the 24 index components—net worth and bond surety requirements—did seem to have a pretty reliable association. “So we cycled back to that,” says Todd.

Bonding

Look at a plumber’s van and you’ll likely see the words “licensed, bonded and insured.” The first and last terms are familiar, but unless they’re a flight risk, why should a plumber need to be bonded? Mortgage brokers might feel the same way.

Before issuing a license to operate, many states require some professionals to ensure that they’re able to compensate customers who make valid claims of professional nonperformance. Minimum levels of net worth meet this requirement in some states. Other states call for surety bonds; if a bonded professional doesn’t perform as required, a surety bond company pays out a valid customer claim. To remain solvent, the bonding company will seek full compensation from the professional, but it may also, before issuing a bond, screen applicants, just as credit card companies do.

“We speculate that this screening could make bonding one of the most significant barriers to entry in states requiring bonds of $50,000 and more,” write Kleiner and Todd. Their statistical results seem to bear this out. While none of the other licensing components or indexes had any consistent statistical relationship to labor or product outcomes, net worth and bonding requirements repeatedly showed strong connections.

Here’s a summary: Net worth-bonding requirements had

- a negative association with employment in mortgage brokering. “We find that doubling the bonding requirement is associated with a 10 percent decrease in the number of brokers and related lending professionals,” write Kleiner and Todd.

- a positive but imprecise relationship to broker earnings of about 5 percent.

- a negative association with volume of loans processed.

- a negative association with the number of subprime loans originated. “A doubling of the mean bonding requirement to approximately $54,000 would be associated with a cut in the number of subprime loans originated by 300,000 per year in 2005, or about 11 percent.”

- a positive relationship with foreclosure rates.

- a positive relationship to the probability that a refinancing loan or home-purchase loan is high priced. (A $100,000 increase in the bonding requirement is associated with a 5.4 and 5.0 percentage point increase in the likelihood that, respectively, a refinance or a purchase loan, is high priced.) This relationship is stronger for refinancing loans, though, than home-purchase mortgages.

The economists run a variety of checks to ensure that their results aren’t due to statistical quirks, measurement flaws or alternative interpretations. They consider, for example, whether the positive relationship between bonding requirements and foreclosure rates might be because regulators tightened requirements in response to higher foreclosure rates. But their statistical testing rejects this explanation: They time lag the data and show that if causality exists, it runs from regulation to foreclosure, not the reverse.

Some explaining to do

The statistical relationships are clear. Greater regulation in the form of tighter bonding and net worth requirements is statistically associated with a number of outcomes that, for consumers, are adverse: fewer brokers, higher-priced brokers, fewer loans and subprime loans, more high-priced loans and higher foreclosure rates.

But how to interpret these results is less clear. Why, in particular, is tighter regulation associated with more foreclosure? “We can’t explain that fully,” admits Kleiner. Referring to states where higher bonding or net worth requirements may have restricted the supply of brokers, he speculates that “it may be that these fewer brokers each processed a higher volume of loans as lending skyrocketed in the early 2000s, leading them to be less concerned with the quality of these loans.” This interpretation is consistent with Friedman’s idea that restrictions make it difficult for competition to weed out incompetent brokers, so the quality of the loan origination process suffers.

“I understand where that point of view comes from, and it’s possible,” says Todd. “But it is a little hard to know why it would operate so strongly.” He suggests another interpretation: Tighter regulation gave lenders more confidence that they could trust brokers and thus made them more willing to lend to risky people. “So there is a non-Friedman possibility that regulation was working, was creating trust in the broker, and so people were willing to extend risky credit,” says Todd. “That could be the explanation, and that’s why we can’t jump to the conclusion that it’s the old story of entry barriers.” He adds, however, that neither story may be right and that this puzzling result illustrates the need for more theoretical and empirical work on both brokering and occupational licensing.

Alternatives to stricter licensing

This may be where the Venn diagram separates, where Kleiner’s deep knowledge of occupational licensing and Todd’s long experience in housing markets broadens both perspective and possibility for interpretation. But the two fully agree that forms of intervention short of tighter broker licensing regulations might better serve consumer interests. Certification, they both point out, is a means of providing consumers with information about an individual’s credentials that wouldn’t necessarily preclude entry into a field. In most states, anyone can legally offer their services as an accountant, for example, but a consumer might be better off hiring a certified public accountant.

Todd raises another option, initially proposed by Jack Guttentag, professor emeritus at the Wharton School of Business. “In the Guttentag proposal,” explains Todd, “the broker agrees to join a voluntary group that commits him or her to agreeing with the borrower ahead of time on how much the broker will be paid, either as a fixed fee or as a percentage of the loan amount. Then the broker’s job is, for the agreed-upon fee, to find the borrower the best loan they can. The broker gets no benefit from jacking up the [interest] rate.”

The Fed has proposed a set of changes to Truth in Lending regulations, to be adopted under the Home Ownership and Equity Protection Act, which would restrict certain mortgage lending practices and also require that certain mortgage disclosures be provided earlier in the transaction. “So the alternative to licensing,” says Todd, “may be a combination of redesigning the relationship between borrowers and brokers by contract, which is what the Guttentag proposal does, and/or doing that by regulation, which is what the HOEPA proposal, in part, tries to do.”

In the meantime, though, both economists strongly recommend that policymakers slow down and consider the repercussions before they adopt tighter occupational requirements for mortgage brokers. They note that their data set ends in 2006, before the meltdown in housing. The brokerage field has changed—and no doubt shrunk—since then, and issuing new edicts for a rapidly changing industry is likely to result in even more unforeseen consequences, especially if that regulation relates to broker licenses.

“Licensing is the most heavy-handed way of regulating,” observes Kleiner. “It allows members of the occupation to capture both current and future work. It keeps out others from being able to provide these services to consumers and it drives up prices. And as our results show, it has, if anything, a negative effect on quality of services rendered.”

“I think it’s reasonable right now for policymakers to be taking a good hard look at the industry,” concludes Todd. “But our results do add a strong note of caution, especially about raising the financial barriers to entry into the business.”