Author

Emily Sachs

Community Affairs Intern

Since the Earned Income Tax Credit (EITC) was added to the U.S. tax code 32 years ago, it has become the leading federal program for boosting the incomes of the working poor. Traditional cash aid, like that of the former welfare system, did little to encourage recipients to join the workforce and change their socioeconomic status. But by virtue of being directly tied to earnings, the EITC essentially subsidizes work.

The program, which is administered by the Internal Revenue Service (IRS), provides refundable tax credits to low-income workers. Refundable means that if the credit a worker qualifies for is greater than his or her income tax liability, the worker receives the excess as a refund.

The amount of the credit depends on a worker's wages and family size. For the 2007 tax year, the income ceiling for married couples with two children is $39,783. Such families are eligible to receive up to $4,716 in a lump-sum credit. A single working person with no children who makes up to $12,590 will also qualify for the EITC and can receive up to $428. In addition, 20 states and several local governments have enacted their own forms of earned income credits (EIC) that refund a portion of state or local taxes. In the Ninth District, Michigan, Minnesota, and Wisconsin all have state EICs.

Boosting family incomes

Nationally, more than 20 million families received more than $40 billion in 2006 through the EITC. Each year, the program provides enough money to lift nearly 5 million people, as many as half of whom are children, above the poverty line. In fact, data indicate that children may be the biggest beneficiaries of the EITC. One estimate by the Council of Economic Advisers suggests that more than half of the decline in child poverty between 1993 and 1997 was due to tax changes—most notably, changes to the EITC, which was expanded to help all single parents who work full time at the minimum wage and receive food stamps rise above the poverty level.

A qualified success

From an administrative perspective, the EITC is a streamlined, successful program. The credits it provides are essentially cash, which can be distributed more efficiently than other forms of support. Also, the program has low administrative costs; the Government Accountability Office estimates they may equal less than 1 percent of program payments.

The EITC is less successful in some other respects. For example, the program fails to reach all of the families it could help. Estimates suggest anywhere from 11 to 25 percent of eligible workers fail to claim their credits. Why is the program failing to reach up to one-quarter of its intended beneficiaries? The answer lies in the quirks of the tax-filing process. In order to claim the EITC, a worker must file a tax return. But many of the workers who are eligible for the EITC do not ordinarily file tax returns because their incomes are too low to trigger any federal tax liability. These workers may have had little or no exposure to the federal tax forms that explain what the EITC is and how to claim it.

Workers who attempt to claim the EITC may find the filing process unexpectedly complicated. EITC filers must use Form 1040 or another itemized tax form, even if they have no need to itemize deductions. The 1040-EZ, the most user-friendly form, does not allow for EITC credits. The complexity of the 1040 form may discourage workers from claiming the EITC altogether or drive them to seek help from private tax preparation firms, where they could end up losing a hefty portion of their credits to fees and other service charges. Low-income filers are more likely than other filers to be charged at least $100, or even as much as $600, for tax preparation services.1/ High fees have the net effect of significantly reducing the benefits workers receive from the EITC program.

The program has other flaws. For example, fraud, intentional or not, is difficult to monitor and therefore more common with the EITC than other poverty-reduction programs.2/ This has hurt the program’s political support and public image.

Nonprofits step in to help

The EITC program's weaknesses have kept it from receiving the universal political support and generous funding needed to conduct a widespread promotional campaign. Since the IRS is not positioned to make a large investment in the EITC—either in marketing it, reaching out to eligible recipients, or investigating every refund for fraud—much of the responsibility for promoting the program has fallen on other parties.

The private sector is one example. Private employers are now required to notify employees about their possible eligibility for the EITC, either by issuing them a W-2 form with an EITC notice printed on the back or providing copies of IRS Notice 797, which explains who is eligible for the credit. Some employers have gone above and beyond the notification requirement by launching in-house EITC awareness campaigns. (For more on this development, see the sidebar below.) Nonetheless, many employers still fail to inform their employees about the EITC, and many employees likewise fail to utilize the program.

Consequently, nonprofit groups and coalitions have stepped forward to increase access to tax support services and extend the benefits of the credit to more low-income working families. For example, the United Way of America has chosen financial stability of low- and moderate-income earners as a national initiative. The organization sees the EITC as a critical piece of the effort. The U.S. Conference of Mayors has spearheaded a movement to introduce EITC campaigns in individual cities. The effort has spread from cities such as New York and Chicago to Orlando, Fla., and Lewiston, Maine.

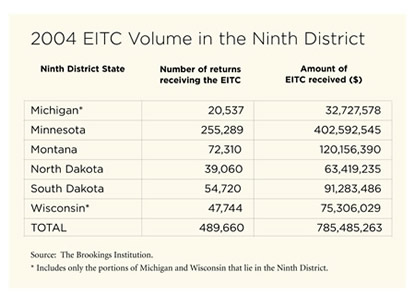

In the Ninth Federal Reserve District, EITC promotion is primarily led by nonprofit organizations. Efforts extend from urban and rural areas to Native American reservations. Among them:

- The Claim It! campaign, a partnership of local governments, nonprofit organizations, and private corporations in the Minneapolis-St. Paul area, helped 30,270 people with free tax preparation in 2007. The campaign increased state and federal refunds and credits by more than $3 million, for a total of $21.6 million. A focus of the effort is to increase the volume of EITC returns by expanding the capacity of tax sites and extending their service hours.

- In the largely rural region of Clay County, Minn., and Cass County, N.D., where EITC outreach had never taken place, the Red River Community EITC Coalition brought together 15 agencies to initiate a first-ever EITC awareness campaign. As a result of the 2006 effort, which included postcard mailings and public events throughout the region, plus informing every county in North Dakota about the campaign, the amount and scale of refunds doubled or tripled in some areas.3/

- In 2006, Community Action Duluth in Duluth, Minn., embellished an already successful free tax preparation program by making the most of the time clients spent in the waiting room. Through an expansion of its Covering All Families program, The Children's Defense Fund Minnesota trained volunteers to screen people for eligibility for other income-based public programs, such as utility assistance and health insurance.4/

- With the support of a nationwide EITC network organized by the Native Financial Education Coalition (NFEC), a number of American Indian tribes in the Ninth District conduct EITC outreach to reservation communities. In addition, the results of an NFEC-sponsored survey indicate that American Indian reservations in the District will host a total of nearly 30 free tax preparation sites in 2008. (For more information on the NFEC EITC Network, see the sidebar titled, "A primer on free tax preparation assistance," also in this issue.)

A trend toward asset development

Proponents of the EITC recognize that the story doesn't end when a low-income worker receives a credit. The next chapter involves encouraging EITC recipients to put at least some of the money toward long-term financial goals.

The biggest trend within the EITC movement seems to be in the area of asset development, which has the larger goal of encouraging recipients to be more self-sufficient and able to cover unplanned expenses.

In order to build savings, low-income families must first build relationships with financial institutions. A recent study of 700 low-income workers who received free tax preparation services through Accountability Minnesota (AAM), a nonprofit organization, found that low-income earners with existing bank accounts were up to eight times more likely to save than those without accounts.5/

Outreach programs are embracing asset development in various forms. Nonprofit organizations are forming partnerships with banks to enable EITC filers to open checking and savings accounts at the same time that they receive tax preparation help. For example, in the Community Action Duluth program mentioned above, banks were on hand to help clients open accounts on the spot.6/

The U.S. Treasury is encouraging the use of direct deposit, which may promote saving by removing the temptation for tax filers to spend a "live" check they receive in the mail. In 2007, the IRS introduced a split refund option for tax filers, allowing refunds and refundable credits to be divided among up to three savings or checking accounts via direct deposit.

AAM, with the help of the McKnight and Annie E. Casey foundations, took direct deposit and asset development a step further in 2005 through the Refund Loan and Savings Program. The program, which was created as a response to the costly refund anticipation loans marketed by private tax preparers, requires clients who receive free tax assistance at U.S. Federal Credit Union to open a savings account at the same time that they receive the assistance. Any refunds are then directly deposited into the new account. As soon as one day after the tax return is completed, clients can borrow up to the full amount of their expected federal refund. During the 2007 tax season, filers opened 361 accounts through the program; 243 recipients took out loans. As of May, 88 percent of the accounts were still open,7/ an encouraging sign that many low-income working families can embrace banking.

Taken together, asset development efforts, free tax preparation services, community outreach, and employer-sponsored promotional campaigns form a patchwork of initiatives that are raising awareness of the EITC. As these initiatives multiply and strengthen, the hope is that the program's benefits will one day reach all eligible families.

Emily Sachs served as a Community Affairs intern at the Minneapolis Fed in 2007. She is pursuing a master's degree in public policy at the University of Minnesota's Hubert H. Humphrey Institute of Public Affairs.

Private employers help promote the EITC Some private companies are expanding their role from employing people to empowering them. One tool of choice is the Earned Income Tax Credit (EITC), which provides refundable tax credits to low- and moderate-income workers. Employers can help their employees take better advantage of the EITC by providing free, on-site tax preparation services and accompanying financial education programs. The benefit to employees is obvious: workers who claim EITCs will receive hundreds or thousands of dollars. Employers benefit, too, but in less direct ways. On an aggregate level, the EITC is credited with helping workers be more productive by lessening the stress of financial pressures. Also, the EITC may reduce turnover by encouraging low- and moderate-income workers to stay employed in order to earn the credit. The nonprofit Center on Business and Poverty in Madison, Wis., specializes in encouraging companies to promote the EITC in the workplace. The center's director, John Hoffmire, has convinced Staples Corporation, U.S. Airways, and several hospitals and banks to provide employees with free tax preparation and financial literacy programs. The Staples initiative, which began in 2004, has now expanded to nine states and 19 of the company's business locations. Employees who are eligible for the EITC get free tax preparation services through a partnership with H&R Block, whose associates use Savings Point and Benefits Enrollment, a pair of special software programs from the company Nets to Ladders that, respectively, create bank accounts and screen individuals for eligibility for income-based public services. Eligible employees also participate in financial education workshops. Some 500 Staples employees have taken part in the tax preparation and financial literacy courses. According to Hoffmire, surveys conducted after the program was implemented indicate "universal support" from employees. Resources for employers The following organizations can provide additional information to employers who have an interest in promoting the EITC.

|

1/ Don Wedd, "AccountAbility Minnesota: Good RALs," National Community Tax Coalition, www.tax-coalition.org/affiliatesProgramProfilesMinnesota.cfm, August 2007.

2/ Steve Holt, The Earned Income Tax Credit at Age 30: What We Know, The Brookings Institution, 2006.

3/ Don Wedd, "Imaginative EITC Rural Outreach: Fargo Moorhead," National Community Tax Coalition, www.tax-coalition.org/affiliatesProgramProfilesFargo.cfm, May 2006.

4/ Don Wedd, "Community Action Duluth," National Community Tax Coalition, www.tax-coalition.org/affiliatesProgramProfilesDuluth.cfm, January 2007.

5/ Leo T. Gabriel, Indicators of Saving: A Case Study of Earned Income Tax Credit Recipients in the Twin Cities of Minnesota, doctoral dissertation submitted to Anderson University, 2007.

6/ Wedd, January 2007.

7/ Wedd, August 2007.