Author

Microfinance is the provision of small-scale financing to the working poor. While it includes lending and savings products aimed at a range of needs, such as education and home improvement financing, the best-known form of microfinance involves lending to very small businesses, or microenterprises.

The concept of microfinance caught the world’s attention in 2006, when Grameen Bank in Bangladesh and its founder, Muhammad Yunus, received the Nobel Peace Prize for their efforts to “create economic and social development from below.” For more than 30 years, Grameen Bank has helped people in Third World countries escape poverty by providing collateral-free loans and other financial services to support microenterprises.

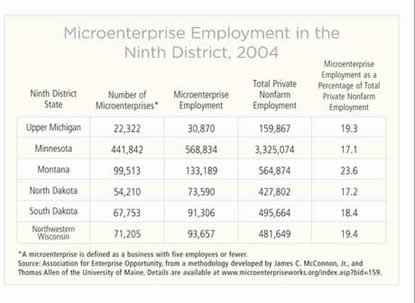

The prize announcement piqued media interest in microenterprise development organizations (MDO) all over the globe, including those in the U.S. MDOs emerged here in the mid-1980s in response to a need for better economic options, particularly for entrepreneurs who lack access to mainstream financial institutions. They provide small business loans, technical assistance or both to businesses with five or fewer employees. The Association for Enterprise Opportunity (AEO), the trade association of microenterprise programs in the U.S., estimates there were 20.7 million microenterprises nationwide in 2001. According to one set of estimates, they make up nearly 86 percent of all enterprises in the U.S. and contribute 16.6 percent of total nonfarm employment. *

Nearly 20 years after its inception, the U.S. microenterprise development field is at a critical point. By 2005, the number of microenterprise development programs in the U.S. had grown to more than 500. Still, achieving sufficient scale and sustainability remains elusive for many MDOs. Many field practitioners and researchers agree that the industry faces a multitude of hurdles. Some of the key challenges they identify are:

- Fragmentation. There are many MDOs that have limited capacity and provide similar products and services, resulting in duplicated efforts across the field and an inability to take advantage of economies of scale.

- Increased competition due to market changes. The growing microenterprise field is attracting the attention of other financial players, which means MDOs are no longer the only entities providing assistance to very small businesses. While increased competition is generally a good thing, some people have expressed concern that products offered by the new players, like credit cards and payday loans, may have high costs and negative effects.

- Lack of standardization and accreditation. Since there are no standardized performance data or certification programs for MDOs in the U.S., funders may lack confidence that programs are worthy of support.

Some MDOs and their networks are attempting to address these challenges. For example, AEO developed national standards for its member organizations. The goal of the standards, which are based on best practices for microenterprise development, is to provide funders at the local, regional and national levels with a mechanism to identify effective microenterprise development programs.

To learn more about the history of MDOs in the U.S. and the challenges these organizations face, Community Dividend spoke with Elaine Edgcomb, who has served as director of the Aspen Institute Microenterprise Fund for Innovation, Effectiveness, Learning and Dissemination (FIELD) since its creation in 1998. FIELD’s mission is to identify, develop and disseminate best practices for microenterprises and educate funders, policymakers and others about microenterprise as an antipoverty strategy. In her role as director, Edgcomb writes and edits works on evaluation practice, institutional development, financial analysis and microenterprise strategies.

Community Dividend: First, a basic question. Why is it relevant to distinguish microenterprises from small businesses in general?

Elaine Edgcomb: According to the U.S. Small Business Administration, the definition of small businesses includes businesses that are relatively large—up to 500 employees. So the term “micro” is used to distinguish or put some focus on the very smallest of these businesses, those with five or fewer employees. The other thing to keep in mind, although it’s not in the definition per se, is that microenterprise development programs focus preferentially on businesses that are started by people who are disadvantaged or marginalized by gender, race, ethnicity or poverty. They help individuals who haven’t had easy access to mainstream business services or have experienced barriers to getting credit. It’s true that the term “microenterprise” could be explained better. There’s some talk in the field about finding additional words to refine the definition.

CD: What led to the development of microenterprise programs in the U.S.?

EE: It’s an interesting question, because people often think the U.S. microenterprise development field is a direct outgrowth of the field overseas. In fact, that was just one of the influences or forces. People in the U.S. did look overseas to understand the microenterprise development methodology being used in Third World countries and how it might be applicable to disadvantaged entrepreneurs and low-income individuals here at home. But prior to the emergence of the international field, there were a number of other things happening in the U.S.

In the early 1980s, a number of women’s organizations started trying to create more opportunities for women to engage in small businesses in the U.S. Their interest emerged as a response to the limited options that existed for women in both wage employment and business ownership. Various programs were developed to provide business training and counseling for women at all economic levels.

Another impetus was that some organizations began to look at self-employment as an option for the unemployed. The Corporation for Enterprise Development, a policy organization that’s now called CFED, was inspired by some initiatives in Europe that allowed people to use their unemployment insurance payments to start their own businesses. CFED representatives went to Europe and looked at some examples of these initiatives. They returned to the U.S. and, with the U.S. Department of Labor, launched a demonstration using unemployment insurance to help people move to self-employment rather than into another job.

At the same time, community development corporations and other groups at the community level were looking at ways to revitalize neighborhoods where businesses had left. These groups began to see new business development as an option. Community action agencies, which work mainly on behalf of low-income people, began to see that maybe self-employment was a viable option for their clientele. So all these trends began to lead to the growth—almost the explosion—of microenterprise development in the U.S. from the mid-1980s onward.

CD: What causes people to start microenterprises?

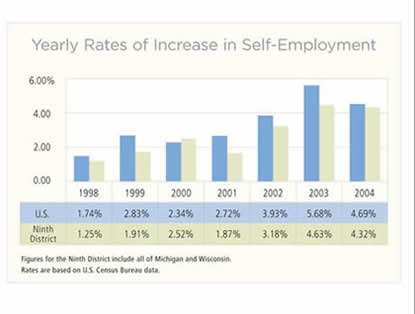

EE: There’s a set of “push-pull” factors to consider. First, the loss of opportunities to get “middle-class” jobs is a contributing factor. In many places, the available jobs don’t provide a secure, middle-class income anymore. As people are pushed into the low-wage sectors, they look for other opportunities to generate income. Corporate downsizing, the outsourcing of jobs, the reliance by some corporations more heavily on a temporary workforce rather than a workforce that has permanent employment backed by benefits—all of those trends encourage people to look to self-employment as an alternative source of income or a supplement to the wage employment they have. [For more on the rise in self-employment, see the graph below. Editor]

Other “push” factors include growth in immigration, the aging of the population (workers over 50 have a higher rate of self-employment than others), changes to welfare programs and the decline in many rural economies as farming has changed or consolidated.

The “pull” factors that draw people to self-employment include flexibility in terms of work hours, especially for women trying to balance their working and care-giving roles, and the growth of niche markets where microenterprises can prosper.

CD: Is promoting microenterprises a good strategy to alleviate poverty?

EE: The short answer is yes, for some people. It’s not for everybody. We’ve done some studies and looked closely at others. They show that people who pursue business ownership experience income growth over time. In many families, the increasing income is sufficient to move them above the poverty line. One study looked at what happens to entrepreneurs over a five-year period. Over that period of time, 53 percent of the entrepreneurs studied were able to move out of poverty. We also saw that when they move above the poverty line, many entrepreneurs do it not just through a business, but through a combination of wage employment and business. We call that concept “income patching.” Within a family, a number of members may be contributing to the household income by pursuing wage employment and business ownership, and together all those pieces help move the household out of poverty. The portion that can be attributed to business ownership depends on the amount of time the person spends working in the business and the length of time the person has been in business. Over time, we usually see the business grow and the return to the producer increase. The business can then provide an income supplement to help the family move above the poverty line.

Finally, we found that entrepreneurship does not end the struggle. Healthcare is generally a major concern for low-income people. Even if a microenterprise provides supplemental income to help the family inch above the poverty line and improve certain conditions, these families often are not able to cover healthcare expenses. That’s why many household members hold wage jobs that provide healthcare benefits.

CD: Based on data collected in 2005, you’ve estimated the market for the services provided by MDOs in the U.S. to be about 10 million individuals. Can the MDO field grow enough to help all those potential entrepreneurs?

EE: It’s a huge challenge to try to grow with limited resources. The MDO field needs to start thinking about how services are delivered. Looking at ways to use technology is one possible solution. For example, we helped develop an online tool called Micromentor that connects experienced business people—acting as mentors—with entrepreneurs.

Also, it’s important to look at ways to restructure the field. Instead of having hundreds of very small programs, practitioners could look at ways to achieve economies of scale through mergers, strategic alliances or acquisitions.

Finally, there is a need for better market research. This is really critical and can help microenterprise programs better plan their outreach activities and understand the changing marketplace. Ten years ago, there were fewer financial alternatives for entrepreneurs to use in developing and implementing their business ideas. Today there are so many alternatives, positive and not-so-positive. There are credit cards, banks, check-cashing outlets and payday lenders, just to mention a few. Practitioners need to understand the market situation, both on the supply and the demand side, so as to better position themselves.

CD: What does the future hold for the microenterprise development industry?

EE: Microenterprise development is getting more complex and sophisticated. We’re going to see more programs that will help entrepreneurs to not start businesses, but to really grow them and become savvy about the current marketplace. Also, there’ll be a much larger role for programs that help individuals become financially literate and programs that sustain families through asset development.

There’s a growing emphasis on rural microenterprise development, and I think we’ll see more of that in the future. In some rural communities, there are programs that focus on microenterprises as part of a broader entrepreneurship development system. The aim is to build a pipeline of rural entrepreneurs and help them grow and become successful. We see some microenterprise development programs beginning to specialize in certain sectors, like specialty foods or child care. In other rural areas, there are efforts to develop “regional flavor initiatives,” where microenterprise development programs work not only with business developers, but also with tourist promotion programs, heritage institutions and cultural institutions to build an economy around the unique characters or features of the local region.

Regardless of the setting, I think the future paths of individual MDOs will vary depending on their leadership and circumstances. On the ground, I see organizations that will continue to be small and serve a small part of their local communities. I also see a set of organizations that are on the cutting edge and are probably going to take off and do extraordinarily well.

Microenterprise development spotlight Four Bands Community Fund As Elaine Edgcomb mentions in our interview, it’s common for microenterprise development organizations to focus their efforts on specific racial or ethnic groups. Four Bands Community Fund (Four Bands) in Eagle Butte, S.D., is one example. Four Bands was founded in April 2000 to encourage economic development and enhance the quality of life on the Cheyenne River Indian Reservation. The organization’s services include a comprehensive business training class called Cheyenne River Entrepreneurial Assistance Training and Education, or CREATE; a variety of business loan products, which require borrowers to receive training in personal finance or business planning; Made on the Rez, a collection of marketing and development services that includes a retail store, e-commerce Web site and online business directory; individual development accounts; youth entrepreneurship programs; and consumer education. As of year-end 2006, Four Bands has served more than 800 clients and closed 90 loans totaling $470,000. All of the fund’s borrowers are Native American and most are women. Many of the businesses served are based in tourism or cultural artisanship. There is strong, persistent demand for Four Bands’ services. As a result, the organization’s major challenge is to keep up with the demand for capital. Additional challenges include the lack of business experience on the reservation and the extremely remote locations of some clients, which can impede the delivery of products and services. Partnering with other organizations is a priority for Four Bands. Through an effort funded by the W. K. Kellogg Foundation, the organization has worked collaboratively with other Native organizations to create and implement an entrepreneurship development system via the Oweesta Collaborative. (For more information on this effort, contact Staci LaCroix at slacroix@oweesta.org.) Other partners include the South Dakota Small Business Development Center, University of Sioux Falls Center for Women’s Business Development, Cheyenne-Eagle Butte High School and Tribal Ventures. |

Ninth District Microenterprise Development Organizations Upper Peninsula of Michigan Minnesota Montana North Dakota South Dakota Northwestern Wisconsin The list above is not all-inclusive. It reflects Ninth District microenterprise development organizations listed with the Association for Enterprise Opportunity and the Aspen Institute Microenterprise Fund for Innovation, Effectiveness, Learning and Dissemination as of January 2007. |

* The primary methodology for arriving at these estimates was developed by James C. McConnon, Jr., and Thomas Allen of the University of Maine. Details are available at www.microenterpriseworks.org/index.asp?bid=159.

Michou Kokodoko is a senior policy analyst in the Minneapolis Fed’s Community Development and Engagement department. He leads the Bank’s efforts to promote effective community-bank partnerships by increasing awareness of community development trends and investment opportunities, especially those related to the Community Reinvestment Act.