Authors

Toby Madden

Regional Economist

Troubles that started in the financial sector have led the U.S. and district economies into a recession. According to the Minneapolis Fed's forecast model and business outlook poll, the economic downturn is expected to continue well into 2009 and will likely dig deeper in the eastern part of the district compared with the west.

Consumer spending is expected to remain weak, employment is predicted to contract and unemployment rates are anticipated to increase in 2009. Home building and residential real estate markets have been in the doldrums, and recovery may be more than a year away. However, inflation worries have dissipated as a number of energy and commodity prices have recently decreased. Agricultural producers had a good year in 2008, but are concerned about profitability in 2009.

District follows U.S. economy into downturn

According to the National Bureau of Economic Research, the arbiter of when recessions begin and end, the U.S. economy slipped into a recession starting in December 2007. Since the beginning of 2008, the U.S. economy has lost 1.9 million jobs through November. Furthermore, initial claims for unemployment insurance benefits were up more than 50 percent in November compared with a year earlier.

The broadest measure of economic growth, gross domestic product, didn't decrease during the first half of 2008, but contracted 0.5 percent in the third quarter and is anticipated to drop further in the fourth quarter. The third and fourth quarters were dealt sharp decreases in consumer spending, which comprises more than two-thirds of the economy.

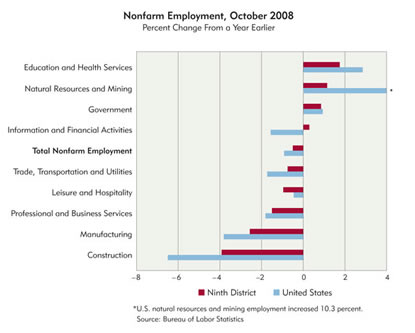

Employment and consumer spending conditions in district states largely echo those of the nation, as a number of companies announced layoffs since September. Districtwide, nonfarm employment was down 0.4 percent in October compared with a year earlier.

Sectors with the largest employment decreases include construction (-3.9 percent), manufacturing (-2.6 percent) and professional and business services (-1.5 percent). While employment as a whole was soft, not all sectors shed jobs during the first 10 months of 2008. Sectors with increases in employment include education and health services (+1.8 percent), natural resources and mining (+1.6 percent) and government (+1.4 percent). (See chart.)

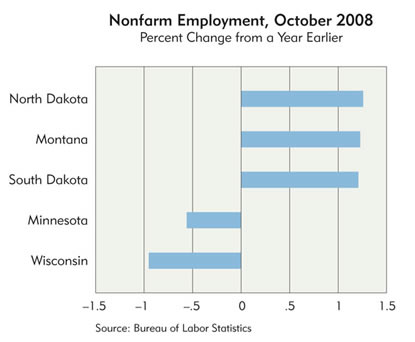

Just as not all sectors have lost jobs, not all states have lost jobs either. Montana and the Dakotas recorded job gains in October compared with a year earlier (see chart below). While economic conditions have slowed in Montana and the Dakotas, these areas are weathering the national recession better than the eastern parts of the district due, in large part, to a relatively strong agriculture sector, as well as strength in mining and oil drilling activity. However, recent drops in commodity prices have softened activity in these sectors.

As employment has contracted, claims for unemployment insurance benefits have climbed, as has the unemployment rate. In Minnesota, initial claims for unemployment insurance were up 31 percent in October compared with a year earlier. Unemployment rates increased in all areas of the district during 2008. The district unemployment rate for October reached 5.3 percent compared with 4.4 percent a year ago.

According to the Minneapolis Fed's forecasting model, employment is expected to contract in Minnesota, Wisconsin and the Upper Peninsula of Michigan in 2009, with modest growth in Montana and the Dakotas (see economic forecast). Meanwhile, unemployment rates are predicted to increase in all areas in 2009, except in Montana.

As jobs have been lost, consumer spending has been constrained. Not only has the downturn in employment stifled spending, but the ability of consumers to harness home equity and consumer loans has diminished as home values have decreased and credit standards have tightened. Reports from major retailers based in the district point to slow sales in October and November.

The outlook for retail suggests that consumers will continue to pull back spending through the holiday season and into 2009. A preholiday spending survey conducted by the University of St. Thomas of households in the Minneapolis-St. Paul area indicated that respondents expected to spend over 10 percent less on holiday gifts compared with last year's season. Furthermore, 85 percent of respondents to the business outlook poll expect consumer spending to decrease in their communities during 2009.

Home building and sales continue their torpor

The financial crisis has its roots in the residential real estate market, as a relatively large percentage of subprime home loans packaged into complex securities became delinquent and went into foreclosure. Since the outset of the crisis, home prices, sales and building have plummeted in many areas.

Home prices in Minneapolis-St. Paul, Fargo, N.D., and Sioux Falls, S.D., decreased 10.7 percent, 4.7 percent and 1.8 percent, respectively, during third quarter 2008 compared with a year earlier. Meanwhile, existing home sales decreased in all areas of the district during the same period.

Home building continued to tumble during 2008. Following annual decreases since 2005, housing units authorized decreased 29 percent during the first 10 months of 2008 compared with a year earlier. During the past year, nonresidential building also slowed, but it remains relatively strong compared to residential building.

The outlook for home building continues to look grim for 2009. Almost 80 percent of respondents to the business outlook poll expect housing starts to decrease in their communities during the upcoming year, and the Minneapolis Fed's forecasting model also points toward decreases in housing units authorized.

Manufacturing has also suffered during the economic downturn. In addition to job losses in the sector, Creighton University's survey of manufacturing showed that manufacturing activity in Minnesota contracted from August through November. However, manufacturing growth in South Dakota only turned negative in November, and growth continued in North Dakota. According to the Minneapolis Fed's business outlook poll and survey of manufacturers, district manufacturers are pessimistic regarding manufacturing activity in 2009.

Inflation fears dissipate

Energy and commodity prices soared during the first part of 2008. But as the economy began to slow during the latter part of the year, these and other prices began to fall as well. The consumer price index decreased 1 percent in October from September levels, the steepest one-month decline since the Bureau of Labor Statistics began releasing seasonally adjusted changes in 1947.

The energy component of the index fell almost 9 percent in October. Average Minnesota gasoline prices dropped to $1.72 per gallon by the end of November, almost $1.25 lower than a year earlier. Meanwhile, the core component of the CPI, which excludes volatile energy and food prices, decreased 0.1 percent in October from September levels and was a modest 2.2 percent higher than a year earlier.

Prices also moved lower for a number of wholesale goods measured in the producers price index; the finished goods index dropped a striking 2.8 percent in October from September. The decrease in prices from their upward trends spells good news for consumers and a number of businesses. Lower retail prices can give a shot in the arm to consumer spending, and lower input costs can help widen profit margins.

Ag profits up in 2008; concern for 2009

Price volatility increased, planting and harvests were delayed and bioenergy firms ran aground, but Mother Nature blessed producers with a large harvest in 2008. Moisture conditions improved across most of the Ninth District, except in the far eastern portion.

Average 2008 prices increased for wheat, corn, soybeans and steers; however, average input costs also increased. The outlook for 2009 is mixed, with many producers facing costs that may exceed expected revenues. Wheat and cattle prices are expected to increase, and replenished soil moisture conditions may help produce another bumper crop.

Many changes occurred in 2008 for Ninth District agricultural producers. Demand for grains initially increased as ethanol plants consumed more corn, but ethanol producers cut back usage as costs exceeded revenues. Late spring rains delayed planting, and autumn rains pushed back the harvest. After huge increases in prices through the first half of the year, prices for many commodities fell fast. For example, diesel prices increased 55 percent from January through July, but then dropped 35 percent from July to October. Propane prices increased 21 percent from January through July, but then dropped 36 percent from July to October. Poultry and pig feed prices also posted notable increases from January through July and then declined from July to October.

However, a number of other input costs increased throughout 2008. October prices for fertilizer and agricultural chemicals (including pesticides) increased 87 percent and 9 percent, respectively, from January. October cattle feed prices increased 15 percent from January.

Even with all these changes, agricultural production increased in 2008. Estimated corn production in Minnesota and the Dakotas is over 2 billion bushels, an increase of about 5 percent from 2007, and soybean production (at half a billion bushels) is expected to be on par with 2007. However, 2008 district sugar beet production dipped 7 percent from 2007. Cattle on feed in South Dakota during November 2008 were about level with November 2007.

The outlook for 2009 is mixed. Soil moisture conditions have improved, which bodes well for crop production. According to U.S. Department of Agriculture forecasts, 2009 prices for wheat will increase, remain level for corn and decrease for soybeans. However, cash rents, fertilizer and other costs are expected to eat into 2009 profit margins. Cattle and hog prices are expected to increase, while dairy prices are expected to decrease from 2008 levels (see table).

| AVERAGE FARM PRICES | ||||

|---|---|---|---|---|

| 2005/ 2006 |

2006/ 2007 |

Estimated 2007/2008 | Projected 2008/2009 | |

| (Current $ per bushel) | ||||

| Corn | 2.00 |

3.04 |

4.20 |

3.65—4.35 |

| Soybean | 5.66 |

6.43 |

10.10 |

8.25—9.75 |

| Wheat | 3.42 |

4.26 |

6.48 |

6.40—7.00 |

2006 |

2007 |

Estimated 2008 |

Projected 2009 |

|

| (Current $ per cwt) | ||||

| All Milk | 12.90 |

19.13 |

18.30—18.40 |

14.95—15.75 |

| Choice Steers | 85.91 |

91.82 |

92.59 |

92.00—99.00 |

| Barrows & Gilts | 47.26 |

47.09 |

47.73 |

48.00—52.00 |

Source: |

||||

{kind=link}

{kind=link}