Authors

Toby Madden

Regional Economist

Indications of economic growth in the district during the first part of 2006 are expected to continue through the end of the year and into 2007. Strength in natural resources, manufacturing and commercial construction have boosted economic growth in several parts of the district. According to the Minneapolis Fed's forecasting models, employment growth is expected to continue into 2007 while unemployment rates are expected to decline modestly overall. The outlook for agriculture is mixed, with higher operating expenses likely squeezing profit margins for some producers.

Strong employment gains recorded in natural resources

District nonfarm employment in April was 1.3 percent higher than a year earlier. Employment gains were noted in almost all sectors, except for "other services," where employment was flat. The strongest gain was posted in natural resources and mining at 3.7 percent. Most of the gain was recorded in Montana and North Dakota, where high oil prices have continued to spur oil drilling and high mineral prices have led to strong mining production levels.

Recent oil prices have exceeded $70 per barrel. While higher oil prices have resulted in increased gasoline prices and fuel surcharges for consumers and several businesses, oil producers have benefited from wider profit margins. Oil drilling operations in Montana and North Dakota continued at a vigorous pace. In May, the number of oil rigs in the two states increased to 51, up from 42 a year ago and up from 25 in May 2003. While the district "oil boom" has led to more economic activity and jobs in the region, labor demand for oil drilling operations has led to worker shortages in other sectors.

Similar to oil, higher mineral prices have boosted mine production. Copper prices that were just above $1 per pound in early 2004 reached the $3.50 mark by the end of May 2006. About $1 of the increase occurred during April and May. Nickel and zinc also posted strong gains during the past six months. Mining officials in Montana recently noted that production was generally at strong levels. Other sectors with strong employment gains in April compared with a year ago include construction (3.5 percent), leisure and hospitality (3.1 percent), education and health services (2.6 percent), and professional and business services (2.1 percent). Sectors that showed positive growth rates, but below 1 percent, include information and financial activities, government, manufacturing, and trade, transportation and utilities.

The Minneapolis Fed's forecasting models point to growth in nonfarm employment into 2007, but at lower levels relative to historical averages. Meanwhile, unemployment rates are expected to decrease.

Manufacturing sector continues to improve

The economic downturn in 2001 was preceded by a drop-off in manufacturing activity and employment that began in 2000. At the national level, the percentage of manufacturing capacity utilized for production began to decrease after April 2000, while manufacturing employment peaked in June 2000. Capacity utilization began to increase in November 2001 and has continued to do so through April 2006. In contrast, manufacturing employment continued to drop until January 2006.

Capacity utilization increased as unprofitable firms closed production facilities while others held on and eventually expanded as the pace of economic growth picked up. Manufacturers that weathered the storm were able to keep productivity levels high—producing relatively more output with fewer workers. It's not surprising, therefore, that capacity utilization grew for about five years while employment decreased. Many firms effectively competed in the global marketplace, often by producing customized products with short timelines, in contrast to bulk manufacturing products that are cheaper to produce abroad.

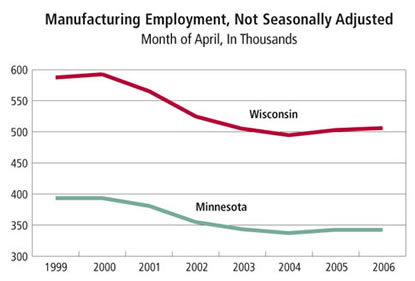

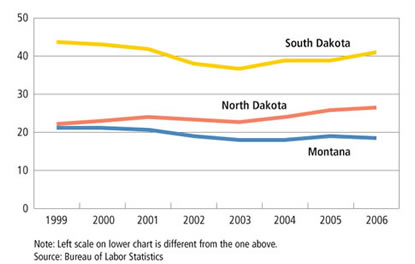

While capacity utilization data are not available at the state level, similar manufacturing employment trends seemed to occur in Minnesota and Wisconsin, but less so in Montana, South Dakota and particularly North Dakota (see chart). Manufacturing employment in North Dakota in April 2006 was higher than in April 2000, the year manufacturing employment peaked in most other district states.

Prospects for continued growth in manufacturing were supported by results from a monthly survey of supply managers and business leaders by Creighton University (Omaha, Neb.) in which solid manufacturing activity was reported during May in North Dakota and South Dakota, and even stronger growth was reported in Minnesota. The survey indicates that manufacturing activity has expanded in all areas consistently since 2003.

Despite gains in manufacturing activity, growth in wage rates for manufacturing jobs has been relatively subdued; manufacturing wages in district states increased 2.9 percent for the three-month period ended in April compared with a year ago.

Home building slows; commercial construction grows

The pace of district home building slowed during the first few months of 2006. District housing units authorized for new construction of single- and multi-family homes decreased 12 percent during the three-month period ended in April compared with a year ago. However, existing home sales in district states were 4.3 percent higher during the first quarter of 2006 compared with a year earlier. Despite the increase in existing home sales, the number of listings in several markets has increased and gains in home prices have slowed.

Nonresidential construction has been active in several parts of the district. In Minneapolis-St. Paul, the vacancy rate for office buildings decreased to 15.2 percent during first quarter 2006, down from 17 percent a year earlier. Vacancy rates for industrial space have also declined during the past year. As vacancy rates decline, the likelihood for new construction projects increases.

Agricultural producers hopeful for 2006

Most farmers and ranchers enjoyed fat profits in 2005 due to large harvests, strong milk prices and the washing away of drought. However, the first half of 2006 saw significant declines in milk prices, softening of other commodity prices and higher input costs. Offsetting these negatives were bountiful spring rains and increased demand to convert grain into energy. Given these strengths and weaknesses, the outlook for 2006 depends on the type of producer. Row crop producers should fare well, cattle producers may struggle to make a profit and hog and dairy producers may see declines.

Mild temperatures and spring rains across most of the district aided farmers and ranchers alike in the first half of 2006. Spring plantings occurred on pace with the five-year average for most district crops. The calving and lambing season went without a hitch for most of the ranches that evaded spring storms. However, as a South Dakota banker noted in the Minneapolis Fed's first quarter (April) agricultural conditions survey, increased "fuel and fertilizer costs along with low crop prices continue to be a big concern," for many producers.

The respondents to the survey expect decreased farm income in 2006, especially for hard-hit dairy producers. Milk prices dropped from $16.05 per hundred pounds in 2004 to $15.14 in 2005 and are expected to fall significantly to the $12.40 to $12.80 range in 2006. In addition, hog prices hovered in the profitable $50 range in 2005 but are expected to drop to the $43 to $44 range in 2006. Meanwhile, cattle producers saw increased prices in 2005 and expect mild drops in 2006. The number of cattle on feed at South Dakota feedlots was level in May 2006 compared with May 2005.

The outlook for 2006 and into 2007 is mixed. Prices for milk and cattle are expected to increase slightly in 2007 from 2006, while hog prices are projected to sink further. Higher operating expenses and lower revenue will put a squeeze on producers' earnings. Meanwhile, wheat producers expect increased prices and a good growing season to aid the bottom line. Corn and soybean producers expect higher prices this season, partially due to increased demand by energy companies. However, the higher energy prices also increase the cost of producing the crop, and profits may be slim.

| AVERAGE FARM PRICES | ||||

|---|---|---|---|---|

| 2003/ 2004 |

2004/ 2005 |

Estimated 2005/2006 | Projected 2006/2007 | |

| (Current $ per bushel) | ||||

| Corn | 2.42 |

2.06 |

1.95-2.05 |

2.25-2.65 |

| Soybean | 7.34 |

5.74 |

5.65 |

5.10-6.10 |

| Wheat | 3.40 |

3.40 |

3.42 |

3.60-4.20 |

| 2004 | 2005 | Estimated 2006 | Projected 2007 |

|

|---|---|---|---|---|

| (Current $ per cwt) | ||||

| All Milk | 16.05 |

15.14 |

12.40-12.80 |

12.85-13.85 |

| Choice Steers | 84.75 |

87.28 |

81.00-84.00 |

81.00-87.00 |

| Barrows & Gilts | 52.51 |

50.05 |

43.00-44.00 |

39.00-42.00 |

Source: |

||||